As we continue our month-long hibernation, one can only pause and reflect at how our world and society have been immeasurably impacted. COVID-19 has accelerated the global mega trends taking place prior to this crisis. E-commerce platforms, last mile logistics, and digital modes of work and communication, once seen to be gradually growing in importance, are now firmly thrust to the forefront of our existence.

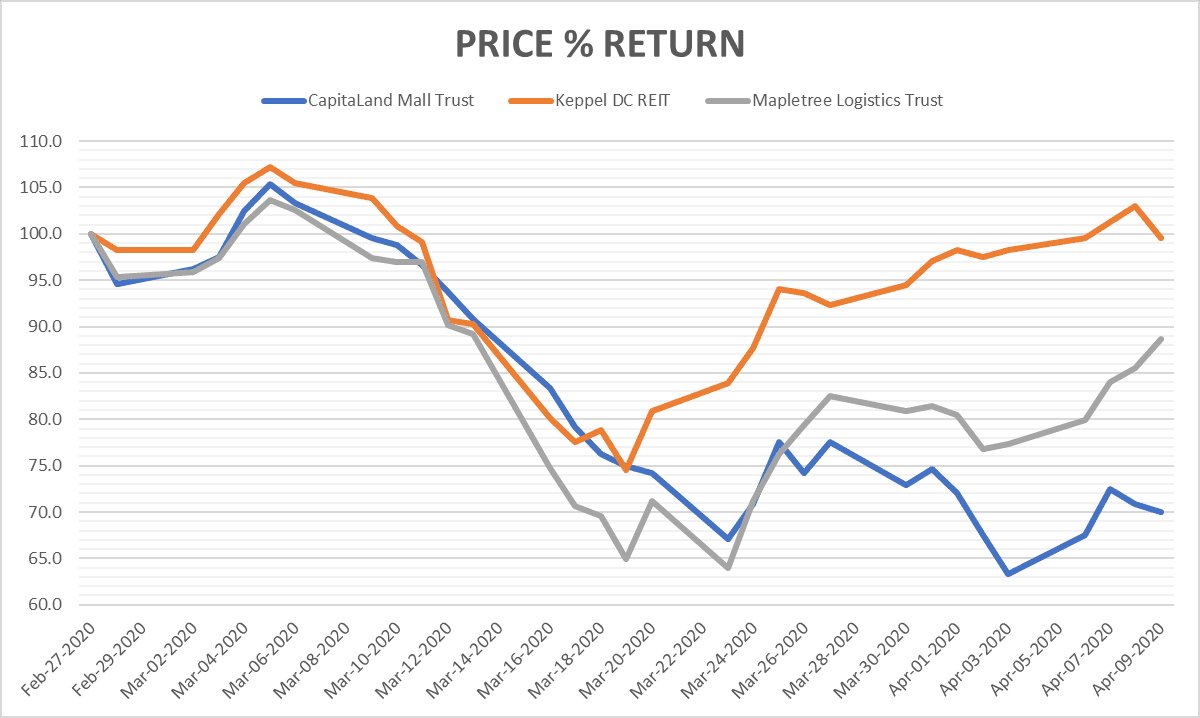

Companies at the centre of these trends have been relatively insulated from the recent market rout. Consequently, the share price performance of Keppel DC Reit and Mapletree Logistics Trust, two companies that are part of digitalization and e-commerce trends respectively, have experienced a smaller negative impact compared to CapitaLand Mall Trust (CMT).

Price percentage return of REITS in different sectors (retail, data centre, and logistics) from 27 February to 9 April 2020. Source: Capital IQ

More broadly, will CMT become a permanent victim to the acceleration of the megatrend towards greater online shopping and e-commerce? Or is this just a temporary blip due to current circuit breaker measures?

What is the original investment case for CMT and does it still hold?

In this article, we shall explore these issues and more.

Original investment case for CMT

CMT is the largest shopping mall owner in Singapore, owning 14.6% of malls that have more than 100,000 square feet of net lettable area (NLA).

For me, the key investment case for CMT lies in its ownership of shopping malls at key travel nodes in Singapore. Accessibility to its malls is everything, and in the course of bus or MRT travel, it is almost inevitable to step foot in one of CMT’s malls at a major interchange. For potential tenants, this is extremely attractive as it leads to higher footfall traffic in their stores.

In addition, the diversity of product offerings at CMT’s malls adds to its importance in the daily lives of Singaporeans. Being a one-stop location where groceries, dining, health and wellness, and fast fashion may be procured, CMT’s malls are a convenient place for one’s needs to be met holistically.

With both the increasing population and higher population density in Singapore, especially in suburban locations, shopping malls are fast becoming, if not already one of the key tenets of our society. A trip down (before COVID-19) to any one of Bedok Mall, Junction 8, Tampines Mall, or Westgate will easily prove this.

The attractiveness of the malls’ locations, wide offering of household essentials, and being a point of socialisation in turn enables CMT to attract: 1) quality tenants, and 2) charge good rents. Together they ensure the sustainability and growth of rental income which is to investors’ benefit.

As a result, CMT experienced good tailwinds in its business in the past few years. This is reflected in its financial performance.

Revenue grew by 18% in the past four years, while net property income (rental income minus operating expenses) expanded by 20% in the same period. CMT was able to maintain its operating margins and also increase distribution per unit to 11.97 cents per unit in 2019, from 11.25 cents per unit in 2015. This implied a dividend yield of about 4.5% (at a share price of S$2.50), providing a good source of passive income especially for retiree investors.

CMT was able to achieve operational growth without having to increase balance sheet risk. Leverage improved to 32.9% as of end 2019 from 35.4% as of end 2015. Interest coverage remained healthy at 4.7 times as of end 2019.

| CapitaLand Mall Trust | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|

| Revenue (SGD million) | 669 | 689.7 | 682.4 | 697.5 | 786.7 |

| Net Property Income (SGD million) | 466.2 | 479.7 | 478.2 | 493.5 | 558.2 |

| NPI Margin | 70% | 70% | 70% | 71% | 71% |

| Earnings Per Unit (cents) | 16.65 | 13.25 | 18.55 | 18.96 | 18.9 |

| Distribution Per Unit (cents) | 11.25 | 11.13 | 11.16 | 11.5 | 11.97 |

| Aggregate Leverage | 35.40% | 34.80% | 34.20% | 34.20% | 32.90% |

| Interest Coverage | 4.8 | 4.8 | 4.9 | 5.2 | 4.7 |

| NAV Per Unit | 1.86 | 1.86 | 1.92 | 2 | 2.07 |

Source: CapitaLand Mall Trust

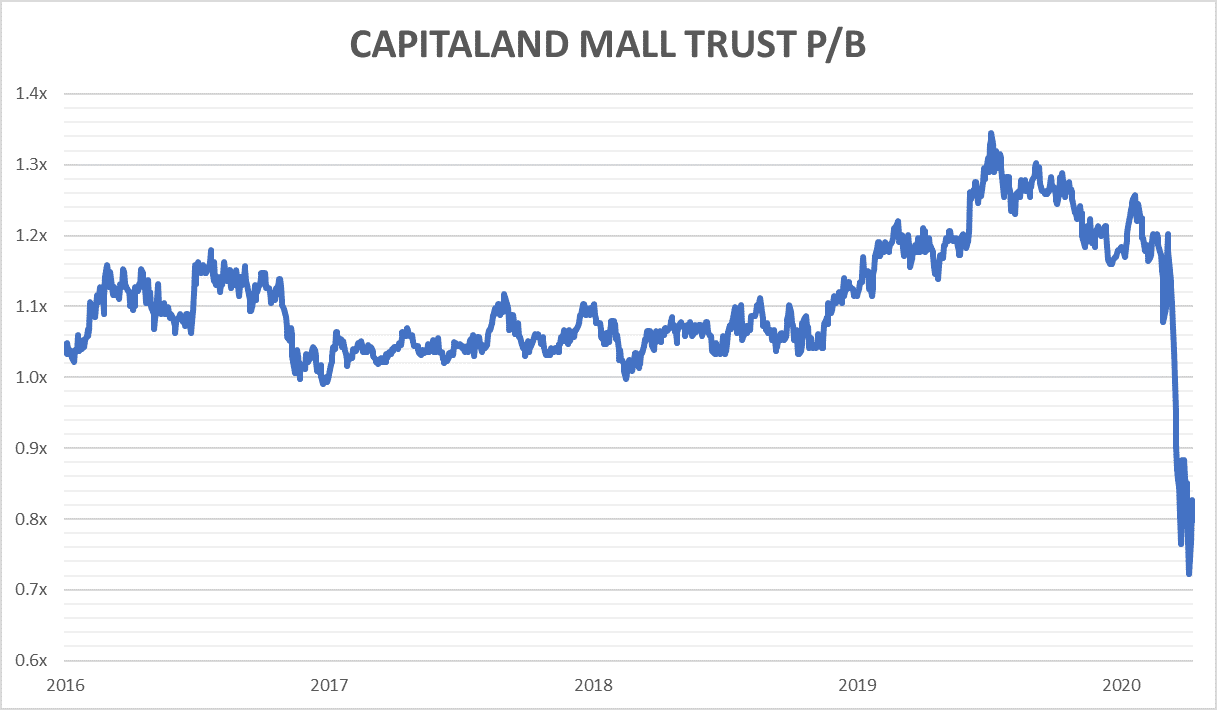

All these factored in the high valuations that CMT’s stock was trading at pre-crisis. However, things came to a grinding halt with the onset of COVID-19.

Exhibit 3: Price to book ratio of CMT collapsed in the aftermath of COVID-19

Source: Capital IQ

So what changed? What triggered the steep fall in prices? Is the decline justified?

First, there was a wide market sell-off at the end of February. These market movements would have been part of the reason why CMT’s stock price came under pressure.

More importantly, I believe two firm specific uncertainties hang over CMT at this point:

- Will significantly lower human traffic at shopping malls impact CMT’s liquidity?

- Will there be a deep property recession that impacts asset valuations?

Underlying these uncertainties, as with most other affected companies, is the question of how long circuit breaker measures will last.

If the timeline in China is to be followed, a return to normalcy between one and two quarters is likely to be manageable for CMT. However, anything longer than a year of disruption will likely result in a significant hit.

Does CMT have enough cash to last the crisis?

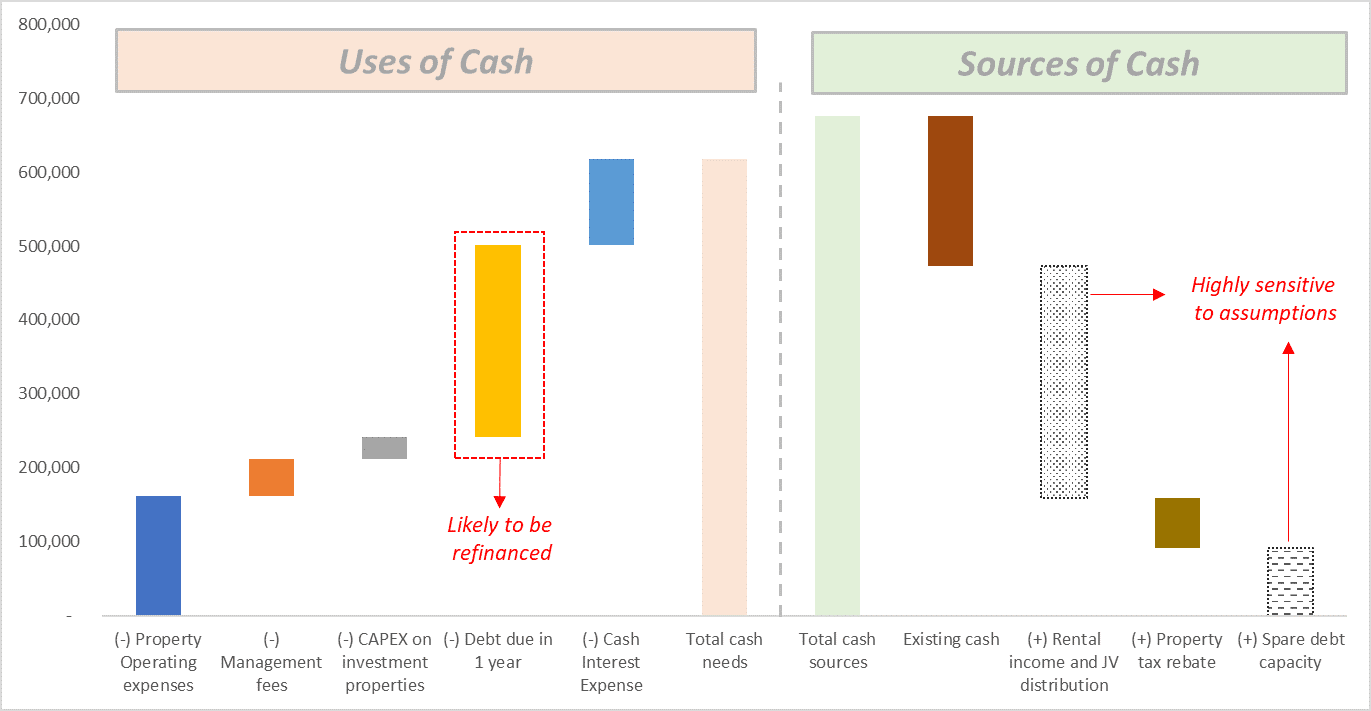

The key to understanding CMT’s liquidity lies in identifying its major sources and uses of cash.

The main uses of cash for CMT are:

- Property operating expenses

- Management fees

- Capital expenditure (CAPEX) on its properties

- Debt and interest payments

The main sources of cash for CMT are:

- Rental income

- Distribution from joint ventures

- Additional debt capacity

- Given the property tax rebate announced by the government, this provides an additional source of cash for CMT (which they will pass on to tenants)

CMT also announced that they will utilise existing security deposits to offset rent payments. It is important to note that this does not represent a new source of cash for CMT as these deposits are already sitting in their cash balance.

Our analysis shows that cash sources can comfortably cover cash needs for one year even in an extreme stress scenario. Uses of cash are estimated based on 2019 amounts. Debt due in one year is based on CMT financial disclosure at the end of 2019, and assumes the unlikely scenario where CMT does not refinance this. Sources of cash are highly driven by assumptions on rental income and joint venture distributions, and the spare debt capacity that CMT has.

Credit to CMT, the company provides a very detailed breakdown of rental income by trade sector in their annual report. The level of granularity extends even to a breakdown by each mall. One key takeaway is how food & beverage and supermarket rental income combined contributes to 34.7% of total gross rental income in 2019. These businesses remain open during this lockdown period.

We have assumed a very conservative haircut to rental income and joint venture distributions in our analysis: 50% decline in 2020 compared to the year before. Given that all stores were still semi-running in the first two months of the year, that F&B and supermarkets continue operating in this stay-home period, given that rents are generally fixed and independent on store turnover, and if businesses can resume normal operations in the last quarter of 2020, a 50% haircut is a conservative estimate.

CMT also has spare debt capacity to bridge its cash needs. As CMT is a REIT, it is not allowed to exceed leverage of 45%. Leverage is measured by total borrowings divided by the value of its properties.

The amount of additional debt CMT can raise depends on 1) the existing debt it has, and 2) the value of its properties.

In our analysis, we have assumed an extremely conservative fall of 25% in its property values when modelling how much additional debt it can raise.

As a sense check, we looked at the market valuation of Tampines Mall and Junction 8 between the 2002/03 SARS, and the 2008/09 Great Recession periods respectively. For Tampines Mall, market valuation increased by 2% during SARS and was flat during the Great Recession. For Junction 8, market valuation increased by 4% during SARS and declined by 3% during the Great Recession.

Finally, if all else fails and while not ideal, CMT can issue equity to meet its cash needs. This is therefore not incorporated in our analysis as we view this to be an unlikely action given that it will send a very negative signal to the market. Such new equity will have to be issued at a steep discount to market price and will be extremely dilutive for existing unitholders (E.g. Singapore Airlines raising SS$5.3 billion in new equity).

What we would like investors to take away is not the exact science of the magnitude of how cash uses and sources fluctuate. Instead, the focus should be on understanding what are the main sources and uses of cash, and whether the company has appropriate levers to pull if additional cash is required to survive this crisis. Our conclusion is that in such an extreme scenario, the company continues to be able to meet its obligations.

Liquidity analysis for the next year shows CMT’s ability to generate more cash than what is required:

Note: Conservative assumptions for rental income and joint venture distribution, and spare debt capacity. Debt due in one year is also likely to be refinanced which will therefore not require cash. Source: CapitaLand Mall Trust 2019 annual report and author’s estimates.

What will happen to distributions?

The profitability of CMT will definitely come under pressure in the near term. Since REITS are generally distribute upwards of 90% of its taxable income, profitability pressure will likely see investors lose out on distributions in 2020.

Nevertheless, there are two potential mitigating factors:

- Capital gains. As earlier shown, CMT is currently trading at a roughly 30% discount to its pre-crisis share price. If one is confident of the long-term economics of CMT’s business, then this represents significant upside.

- Higher dividend yields. Investing at price of S$1.80 (as at 14 April 2020) will enable investors to lock in a dividend yield of 6.7% (based on FY2019 distributions). Although you will not enjoy this yield in 2020, when business recovers and distributions are in line with what was paid in 2019, this is yours to keep.

What does the current valuation represent in terms of a margin of safety?

The market capitalization of CMT as of 14 April 2020 stands at S$6.3 billion. This is the market value to all unitholders of CMT. If we assume no change to the value of CMT’s properties based on 31 Dec 2020’s valuation of S$10.4 billion and total debt of S$3.6 billion, and include CMT’s S$867 million share of joint ventures, the implied value to all unitholders will be S$7.7 billion. At current valuation, this represents a discount of S$1.4 billion to CMT’s net asset value (NAV) as of 31 Dec 2019.

What risks can we attribute this discount to? Has the market overreacted? Therefore, does this provide investors with a margin of safety?

Even if CMT does not have any revenue in 2020, which is unrealistic, total P&L losses is estimated to be in the region of S$400-$500 million a year. This means three years of losses before arriving at the S$1.4 billion valuation gap.

On its own, the discount of $1.4 billion represents a 15% fall in the valuation of its properties. As earlier described, the SARS and Great Recession periods did not see such an extent of decline in mall valuations. Even if both revenue and property valuations fall, our liquidity analysis shows CMT’s ability to bridge cash needs. Only in the very severe case where both revenues and property valuation decline sharply, will we begin to see stress on its balance sheet.

Another reason for the discount is that of lower distributions, at least in the near term. Most investors would have been attracted by the healthy dividend yields provided by CMT pre-crisis. Given the current state of affairs, however, distributions will not be available to the same extent as before. For investors depending on cashflow provided by CMT, the attractiveness of ownership has obviously declined.

The fifth perspective

Human beings are naturally social beings. In Singapore, especially in the searing tropical climate heat we live in, shopping malls will, for better or worse, remain at the heart of our social activities.

I believe the disruption is therefore only temporary, and once a pathway to the resumption of normal activities is clear to see, the original investment case for CapitaLand Mall Trust will emerge from the current sea of murky uncertainty.

Enjoyed the article and analysis – keep up the good work !

How about the envisaged merger with CCT? Has this been factored in your analysis?

No as what will happen with the merger with CCT deserves an independent article on it own.

I highly suspect the merger timetable will be pushed back, as management’s attention now should be on managing the crisis and ensuring the health and safety of its employees/stakeholders.

Broadly on the merger, there are several questions I will raise. They mostly involve the transaction economics. Given the sharp fall in both companies’ market valuation, does the share exchange ratio still hold?

Part of the merger involves CMT raising additional debt. Is it sensible to raise more debt to fund the merger given the uncertain business environment and tight liquidity conditions?

The merger still requires approval from both CMT and CCT shareholders (with Capitaland abstaining). Given the uncertainty, will shareholders approve the resolution?