I’ve been a UOB One user since about 8 years ago. So, when the bonus interest rates were raised, it was…just a Bonus.

But, the latest rate revision still feels like they are taking away candy that was given to us.

UOB One Bonus Interest Revised Downwards 😕

tl;dr: UOB will be revising the Bonus Interest rates on all One Accounts as of 1 May 2024. After the revision, account holders will only get an effective interest rate (EIR) of ~4%, if you deposit $150,000 and meet the criteria of salary crediting and $500 eligible spend on your credit card.

For context, UOB One Account holders were enjoying an EIR of 5% on a deposit $100,000, if they met the other criteria.

How much lesser will we be getting?

If you’re currently keeping your account at $100,000, interest rate will be down 1.6% from 1 May 2024.

But if for some reason you didn’t shift your salary out and have accumulated $150,000, you’ll be seeing an increase of 0.6% EIR as of 1 May 2024.

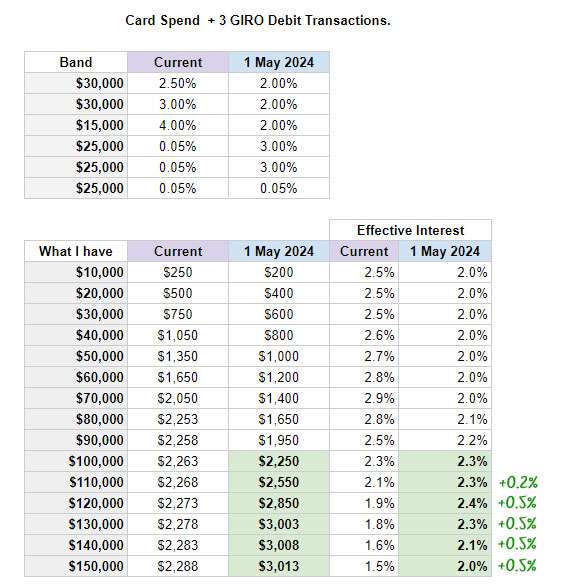

Here’re the differences in interest rate based on the amount of deposit you have:

| Annual Bonus | Effective Interest Rate | Difference | |||

| Deposit | Now | from 1 May 2024 | Now | from 1 May 2024 | |

| $10,000 | $385 | $300 | 3.9% | 3.0% | -0.9% |

| $20,000 | $770 | $600 | 3.9% | 3.0% | -0.9% |

| $30,000 | $1,155 | $900 | 3.9% | 3.0% | -0.9% |

| $40,000 | $1,545 | $1,200 | 3.9% | 3.0% | -0.9% |

| $50,000 | $1,935 | $1,500 | 3.9% | 3.0% | -0.9% |

| $60,000 | $2,325 | $1,800 | 3.9% | 3.0% | -0.9% |

| $70,000 | $2,810 | $2,100 | 4.0% | 3.0% | -1% |

| $80,000 | $3,443 | $2,475 | 4.3% | 3.1% | -1.2% |

| $90,000 | $4,223 | $2,925 | 4.7% | 3.3% | -1.4% |

| $100,000 | $5,003 | $3,375 | 5.0% | 3.4% | -1.6% |

| $110,000 | $5,008 | $3,825 | 4.6% | 3.5% | -1.1% |

| $120,000 | $5,013 | $4,275 | 4.2% | 3.6% | -0.6% |

| $130,000 | $5,018 | $4,800 | 3.9% | 3.7% | -0.2% |

| $140,000 | $5,023 | $5,400 | 3.6% | 3.9% | 0.3% |

| $150,000 | $5,028 | $6,000 | 3.4% | 4.0% | 0.6% |

No matter which camp you are in, the max EIR will be down from 5% (at $100,000) to 4% (at $150,000).

In case you’re wondering…

Does it still makes sense to hit the $500 min spend?

This isn’t for everyone. But if like me, you have no life and you struggle on certain months to hit the min eligible spend, here’s the quick answer: it only makes sense to hit the $500 if you have deposit the max of $150,000.

Of course, you’ll naturally already have spending, so you’ll be weighing your pros and cons based on your spending nature. But, keep in mind that the monthly interest is less than the $500 you’ll be spending for deposits below $150,000.

“But what if I don’t credit salary to UOB One and only max out on card spend and 3 GIRO?”

Good news, if your deposit is at $100,000, you will not be affected. In fact, if you have more than $100,000 in your account, your effective interest goes up.

If you’re in this camp, Investment Moats did the calculations, you can find the numbers here.

Stay with UOB One or move…?

While the revision is disappointing, it is within expectation, given that the US Fed Interest Rates have been stagnant and is anticipated to come down in the near future. (wondering how US rates affect us? read this) So, it is likely that the other banks would follow suit and reduce their rates in the near future.

So…Should you stay with UOB or is there a better high yield savings account out there?

Here are some scenarios to help you decide:

1. You want to Keep It Simple

Confession time: I went with UOB One because the rest had too many criteria and I was lazy.

If you’re as lazy as me and can afford to park $150,000 in your savings account, then UOB One might still be a good option. There’s no need to consider adding insurance or investment products unlike many other high yield savings accounts. You don’t even need to deal with the admin work of changing your salary crediting account.

But if you don’t have $150,000, or you are not happy with the drop of 1.6% interest from 1 May 2025…

2. You want Maximum Yield

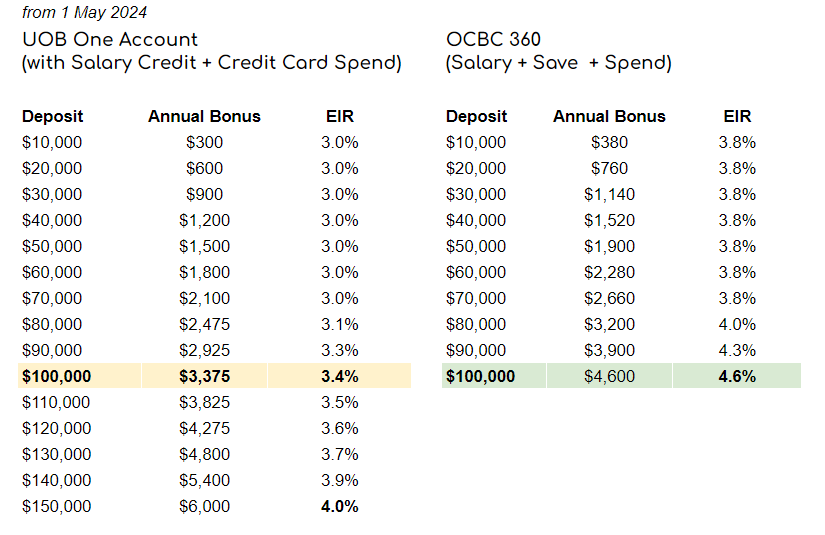

Then OCBC 360 might be the better option, at the point of writing.

Here’s a comparison of the EIR you’ll be getting in May 2024. I’m only comparing against the Salary + Save + Spend option in OCBC 360 to keep the comparison as close as possible:

Of course, if you’re drowning in cash, you could also use OCBC 360 as your salary crediting account and put the rest of your cash into UOB One to earn the bonus interest if you can hit the card spend and GIRO requirements.

Keep in mind, OCBC might revise their rates later this year, who knows. 🤷

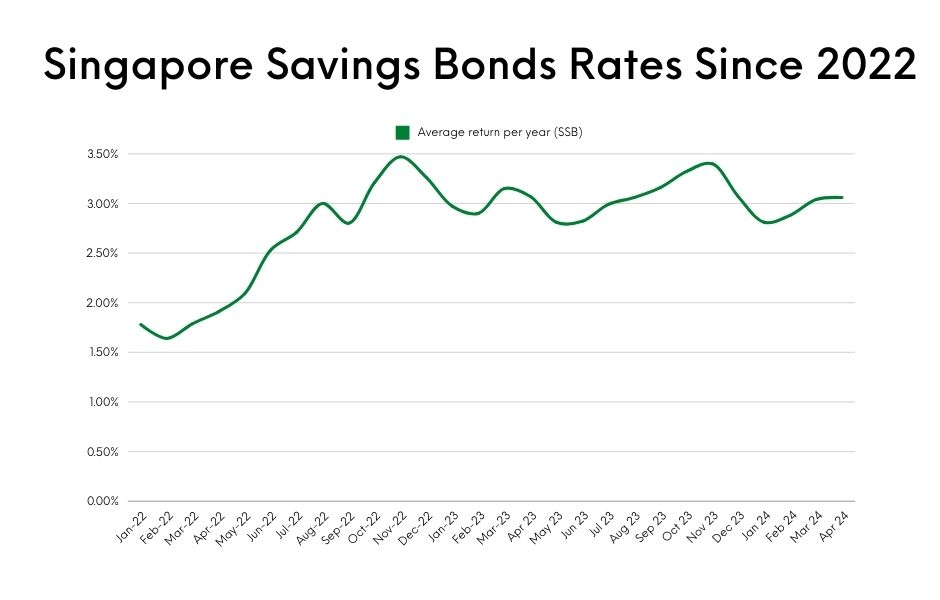

3. You want Consistent Yield over a longer period, and don’t mind a slightly lower yield

SSB is your best bet…at the point of writing.

Here’s the average returns of SSB since the spike in interest rates in 2022:

A few things to note about SSB:

- Rates will not remain at 3%, SSBs rates are based on the average SGS yields from the month before. The lowest rates offered was 0.8% back in Jul 2020.

- You may not get the full allocation if they are oversubscribed.

- Each investor can only hold a maximum of $200,000 worth of SSB at any one time.

While SSB offers some liquidity, take note that it is not as liquid as a cash savings account.

To redeem your SSB early, you’ll need to submit a request, pay $2 and wait till the 2nd business day of the following month to get your cash.

Where else can you park your money now?

Let’s face it, high risk free rates are drying up. UOB One users need to find the best way to reallocate our savings in the coming weeks.

Here’re the few other options you could consider:

| Options | Estimated Rates | Liquidity | Pros | Cons |

|---|---|---|---|---|

| Singapore Treasury Bills (T-Bills) | 3.8% (latest 6-month T bill rate) | 💧 | Relatively easy to apply. You can sell your T-bill in the secondary market if you need cash. | You will have to find another option after 6 months. |

| Singapore Savings Bonds | 3.06% (May 2024 Tranche) | 💧 | Lock in yield for 10 years | Not as liquid. |

| Money Market Funds | ~3.6% | 💧💧 | Relatively Liquid | Rates are not locked in but fluctuates on a regular basis instead. |

| Fixed Deposits | ~3% | 💧💧 | Still comparatively higher yield for almost zero effort. | Higher yields are on shorter term FDs. You will have to find another option when your FD matures. |

| Digital Banks | up to 3% | 💧💧💧 | Criteria is easy to hit. | Rates may change over time |

1) T-bills

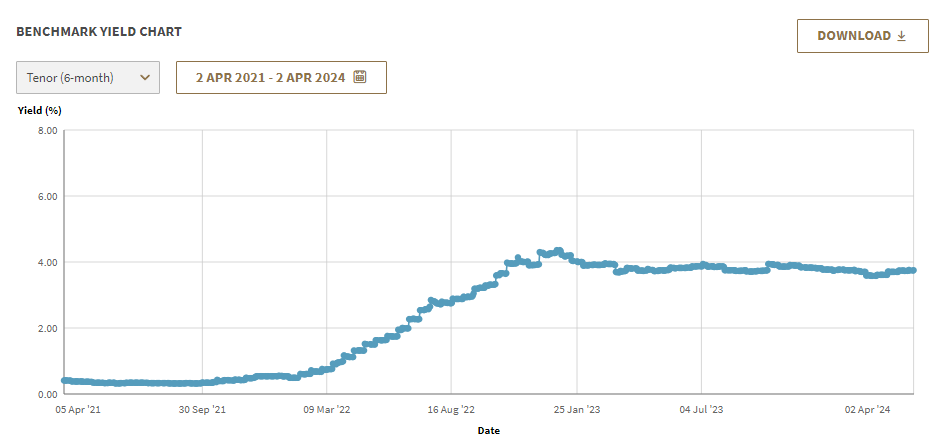

Singapore Treasury Bills aka T-Bills have become one of Singapore’s favorite high yield option since interest rates shot through the roof. They are backed by ah gong the Singapore Government and have a credit rating of AAA.

The latest 6-month T-bill rate on 27 Mar was 3.8%. Here’s how the 6-month yield trend looked like over the past 3 years:

You can learn more about how T-bills work here or on MAS.

2) Fixed Deposits

Fixed deposits don’t need much introduction. Since interest rates had gone up, banks had increased the rates on their fixed deposits to much cheers.

However, as with the revision of UOB One’s bonus interest rate, I expect fixed deposit rates to be revised downwards in the near future.

Currently, the highest fixed deposit rates are offering about 3%. We compile a monthly update of the current SGD Fixed deposit rates here.

3) Money Market Funds

Money Market Funds are income funds that invest in short term debt securities like treasury bills, bonds and the like. This allows them to generate a yield which is given back to the investors.

The advantage of money market funds is that they are liquid, meaning you can sell your position and withdraw your capital anytime. That said, do note that ‘redemptions’ are not instant, it make take a couple of days before the cash reaches you.

The disadvantage of money market funds is that the yields change on a regular basis. As high yield opportunities dwindle, the performance of MMFs may decline over time too. You should also note that MMFs also come with a fee (or expense ratio) which will eat into your potential yields.

Popular ones include:

- Fullerton SGD Cash Fund: ~3.9% (1 year annual)

- Phillip Money Market Fund: ~3.4% (1 year annual)

- moomoo’s Cash Plus: ~6.8% p.a. (but only up to 31 days)

4) Digital Banks

While they offer the lowest interest rates currently, Digital Banks are a good option if you’re looking for an avenue that offers higher rates and higher liquidity. Better for the extra cash you have after you have maxed out your high yield savings bonds.

Trust Bank

- Base interest of 1.5% p.a. on first $500,000.

- Deposit at least $100,000 to earn 2% p.a.

- Make 5 monthly card spend to unlock 2.5% p.a.

- NTUC Union Members get up to 3% p.a.

Earn 2.88% p.a. with no minimum deposits nor spending requirements.

Bad news; Interest Rates will likely continue dropping. Here’s what you can do now

As if inflation isn’t bad enough, we are now facing a double whammy of increased cost of living AND lower rates to grow our money.

I’ve shared several options where we could park our money above. But what else can we do to beat inflation and still grow our money?

Well, Dr Wealth is a investing focused, so our answer might be slightly biased. But, we still think investing is a better and more consistent way of growing our money.

Christopher Ng retired at 39, after building his dividends portfolio. He shares how you can take advantage of the ‘cheap’ dividend stocks in the Singapore markets today and build a portfolio that could replace your salary, and more. Join him at the next live webinar.