Whenever you’re bored and your mind is on idle, you can’t help but to reach out to that f-letter word on your phone. It’s an escape, a place where you get your daily dose of news, entertainment, and interactions with your friends and family. This is not only the place that your loved ones get to know more about you, it’s also the perfect place for advertisers to target you based on your demographics, interests, and behaviors.

I’m sure you know what the ‘f’ I’m talking about by now — Facebook.

So far, it hasn’t been a smooth sailing year for the social media giant. Earlier in March, the company got hit by the Cambridge Analytica scandal. The political consulting firm hijacked data of up to 87 million Facebook users and allegedly used the information to influence voters’ opinions during the 2016 U.S. presidential elections.

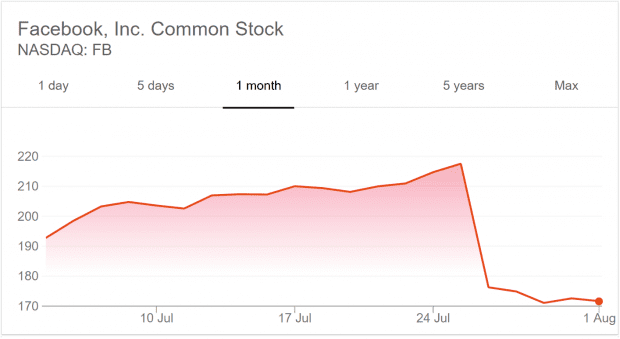

But that’s not all. Last Wednesday, Facebook got smacked once again after posting its Q2 2018 earnings. Facebook’s share price plunged 18.96%, from US$217.50 to US$176.26, in one single day and wiped off US$120 billion in market value at a stroke – the biggest single-day loss in U.S. corporate history.

What could have possibly gone wrong to have caused such a huge knee-jerk reaction from the market? Here’s what happened…

Why Facebook lost US$120 billion in value in one day

Here are the main reasons why investors dumped Facebook when it announced its Q2 2018 earnings:

- Facebook disappointed the Street by missing revenue expectations. Revenue for the second quarter came in at US$13.23 billion, below the consensus estimate of US$13.36 billion.

- Quarter-on-quarter revenue growth decelerated from 47% in Q2 2017 to 42% in Q2 2018. (Yes, Facebook grew 42% in its most recent quarter, which is phenomenal for almost any other company. But for Facebook, it was disappointing.)

- Operating margins decreased 300 basis points from 47% in Q2 2017 to 44% in Q2 2018. The higher costs were driven by Facebook’s commitment to invest in security after the Cambridge Analytica scandal. A new regulation in Europe known as the General Data Protection Regulation is pressuring large corporations to better protect users’ data. Failure to comply will result in a hefty fine, either a fine of €20 million or 4% of global revenue, whichever is higher. (Based on Facebook’s 2017 revenue, that is a US$1.63 billion fine!)

- Facebook’s user growth is slowing down. Growth of monthly active users fell from 3.15% in Q1 2018 to 1.73% in Q2 2018. The social media giant also saw a reduction of one million users from Europe, and the number of users remained flat in U.S. & Canada.

- CFO David Wehner said during the earnings call to expect revenue growth rate to decelerate further by high-single digits for the next two quarters. Of all the points, this is the one that probably sent investors running to the hills. To add salt to the wound, the management also guided investors that investment in areas like safety and security, AR/VR, marketing, and content acquisition will increase, and total expense growth will exceed revenue growth in 2019. Operating margins will also trend downwards to the mid-30s on a percentage basis over the next several years.

To put it simply, the market wiped US$120 billion in value off Facebook because it thinks its hyper-growth story is over.

So is this really the ‘end’ of Facebook?

Here’s why I think Facebook’s stock crash is a knee-jerk reaction from investors, even though I recognize their fear of Facebook’s growth slowing down:

- Facebook has a monopoly on social media. Besides Facebook itself, the company also owns Instagram, Messenger, and WhatsApp. Combined, over 2.5 billion people use at least one of these social apps. Besides China’s social networks, Facebook’s closest competitors in the industry are Snapchat (191 million users) and Twitter (335 million users). In other words, no one comes close to Facebook in the West. Because of this, Facebook enjoys a network effect – since everyone is already on Facebook (or one of its other apps), more people will continue to join Facebook, and so on. This is a nearly insurmountable advantage that Facebook has over its peers.

- Facebook has a duopoly in digital advertising. Along with Google, Facebook dominates the digital advertising industry – 61% of global online advertising spending goes to Facebook and Google. As a share of total media advertising worldwide, the two tech giants occupy a 25% market share. Not only that, the global online advertising market grew 21% (US$88 billion) in 2017, and Facebook and Google accounted for 90% of that growth! If that isn’t a duopoly, I don’t know what else to call it.

- Facebook’s advertising revenue still has room to grow. CFO David Wehner has previously said that Facebook’s newsfeed ad load is nearly maxed out – there are only so many ads you can cram around user content before people get turned off. However, video ads are growing strongly with digital video ad spend among large brands growing by 53% over the past two years. Besides the growth in video ads, ad costs are also rising across the board as more businesses compete to display their ads to consumers on Facebook.

- Instagram, Messenger, and WhatsApp are just starting out. Around 99% of Facebook’s revenue comes from advertising, most of which is generated from Facebook (the social network). However, ad revenue from Instagram, Messenger, and WhatsApp is still relatively untapped. If you’re an Instagram user, you’ll notice the comparative lack of ads on the platform. In 2017, Instagram generated US$3.6 billion in revenue – only 8.9% of Facebook’s total revenue. But Instagram is also Facebook’s fastest growing social network – it has doubled in size from 500 million users to over 1 billion in just two years. As for Messenger and WhatsApp, Facebook is still thinking how best to monetise them (the latter has no ads whatsoever).

- The world and internet population will continue to grow. The world has around 7.6 billion people right now and over 4.1 billion internet users. This is projected to reach 8.1 billion people and 5.0 billion internet users by 2025. In a nutshell, the more people there are online, the bigger Facebook’s potential market is.

The fifth perspective

At the end of the day, you have to keep in mind that businesses don’t rise to the top in a single straight line. There are bound to be obstacles, hiccups, and slowdowns along the way. Our job as investors is to determine whether these problems are permanent or temporary. For example, in the short term, Facebook’s investment in security and compliance may reflect badly on its bottom line, but in the long run being able to provide a secure platform for people to connect is key if Facebook wants to continue growing their user base.

Another thing you have to remember is that ‘trees do not grow to the sky’ — there’s a limit to how large and how fast a business can grow. At some point, a company will mature and its industry will reach a saturation point — Facebook is no exception. Even though it has been growing like gangbusters, there is no company in history that has been able to grow at a rate of 40% annually for, say, 30 years.

Right now, Facebook has 2.5 billion people who use one of their apps (i.e., Facebook, Instagram, Whatsapp, Messenger) – that’s already over 60% of the total number of internet users in the world right now. As Facebook grows larger and larger, a slowdown is bound to happen – and we may be starting to see that now.

So should you #DeleteFacebook from your watchlist/holdings, or is this a chance of something more? Despite its current travails, Facebook’s business model remains intact and is one half of a formidable duopoly in the digital advertising industry. The company has potential growth opportunities from Instagram, generates a huge amount of free cash flow, and has zero debt on its balance sheet.

At the same time, however, its explosive growth looks to be slowing down. The important thing is to factor Facebook’s slower growth rates in your valuation, and never overpay for a stock no matter how good the business is.

If you’re a long-term investor, Facebook will most likely be bigger and more successful five years from now. But in the short term, does that mean Facebook won’t be hit by a scandal, bad news, or another disappointing quarter again? No. That’s just part of the game.