Hartalega Holdings Berhad is the world’s largest nitrile glove manufacturer. As at 1 September 2019, the company is valued at RM17.2 billion in market capitalisation.

In this article, I’ll bring an update on Hartalega’s latest annual results, the development on its Next Generation Integrated Glove Manufacturing Complex (NGC), and offer a few ratios to assess the company’s stock valuation.

Here are 10 things to know about Hartalega before you invest:

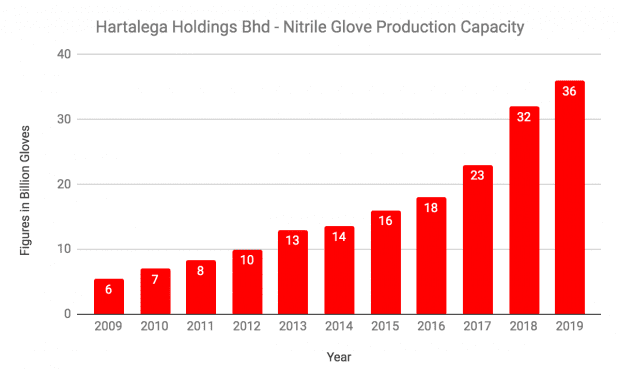

1. As of 31 March 2019, Hartalega has successfully commissioned 10 out of 12 production lines at Plant 5 at the NGC. The company now has an annual production capacity of 36 billion gloves, a six-fold increase since 2009.

2. Hartalega sold a total of 27.2 billion gloves in 2019. This represents a nine-fold increase since 2009 when it sold 3.1 billion gloves.

Over the last 10 years, Hartalega has seen steady growth in sales from its key export markets in the U.S., Europe, Asia, Australia and South America:

| Key Markets | 2010 Revenue (RM millions) | 2019 Revenue (RM millions) | CAGR (2010-2019) | Proportion of 2019 Revenues |

|---|---|---|---|---|

| United States | 427.1 | 1,528.3 | 15.2% | 54.1% |

| Europe | 68.0 | 716.3 | 29.9% | 25.3% |

| Asia | 43.3 | 383.6 | 27.4% | 13.6% |

| Australia | 18.9 | 93.4 | 19.5% | 3.3% |

| South America | 14.7 | 70.0 | 19.0% | 2.5% |

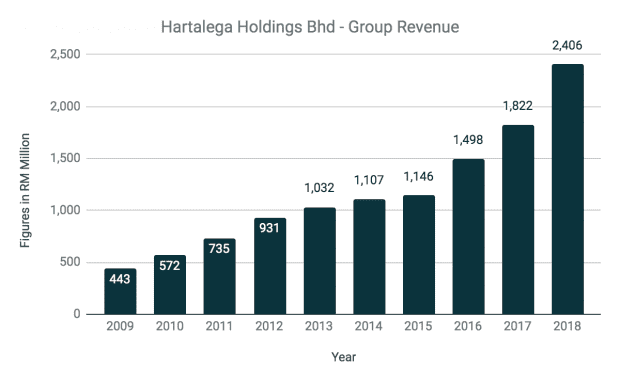

3. Total revenue has grown from RM571.9 million in 2010 to RM2.83 billion in 2019 – a compound annual growth rate (CAGR) of 19.43%.

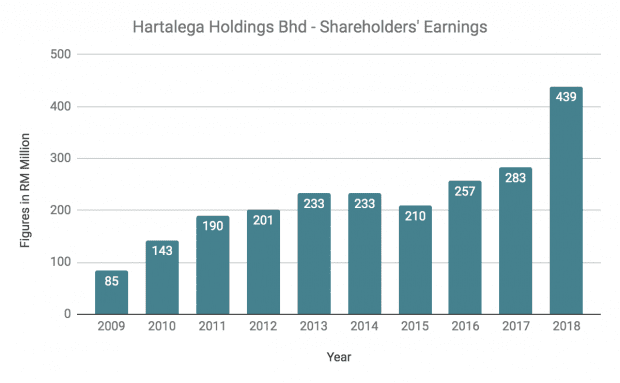

Likewise, shareholders’ earnings have grown from RM142.9 million to RM455.2 million over the same period – a CAGR of 13.74%. Earnings have grown at a slower rate as the company saw margin compression due to higher administrative and distribution expenses.

4. From 2010 to 2019, Hartalega generated RM2.89 billion in cash flow from operations and raised RM795.0 million in net equity and long-term debt. Out of which, it has spent RM389.7 million in capital expenditure, RM1.98 billion in capital work-in-progress, and RM1.24 billion in dividend payments. As of 31 March 2019, Hartalega has a gearing ratio of 9% and a current ratio of 2.18.

5. Hartalega is currently into the sixth year of its eight-year NGC master plan. Plant 6 is under construction and, upon completion, will add another 4.7 billion gloves in annual production capacity. Plant 7 is slated for construction next and will focus on smaller, specialty orders. Its annual production capacity is 2.6 billion gloves. The full completion of Plants 6 and 7 will increase Hartalega’s total annual glove production capacity to 42 billion gloves.

6. Hartalega first launched its antimicrobial glove in Europe in May 2018, and has since exported the product to over 20 countries worldwide. The company is presently working to secure approval from the U.S. Federal Drug Administration in order to market the gloves in the U.S.

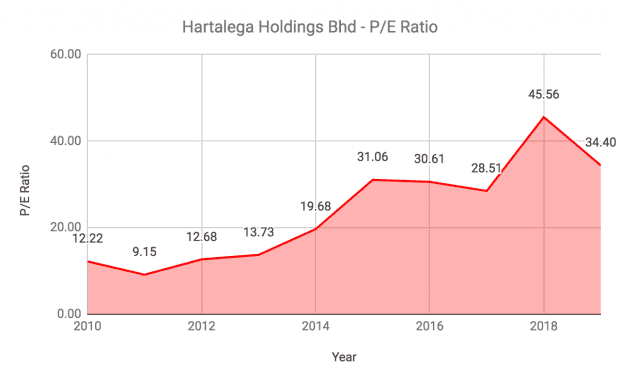

7. P/E ratio: Hartalega posted earnings per share of 13.69 sen in FY2019. Based on its share price of RM5.13 (as at 2 September 2019), its current P/E ratio is 37.47. Although the ratio has come down significantly from one year ago, it remains above its five-year average of 34.03.

8. PEG ratio: As highlighted in Point 4, Hartalega’s shareholders’ earnings has grown at a CAGR of 13.74% over the last 10 years. Therefore, its PEG ratio is 2.73. A PEG ratio above 1.0 is considered overvalued.

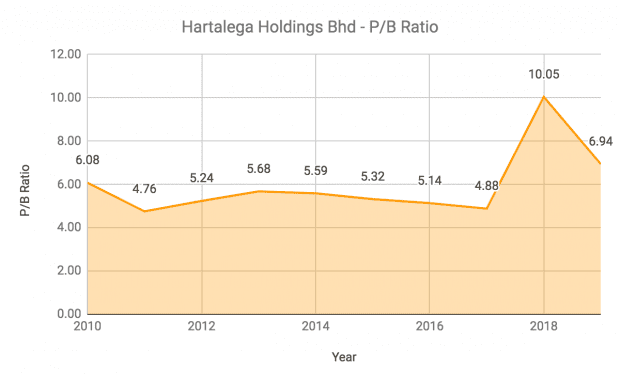

9. P/B ratio: As of 31 March 2019, Hartalega has net assets per share of RM0.67. Therefore, its current P/B ratio is 7.66, which is above its five-year average of 6.47.

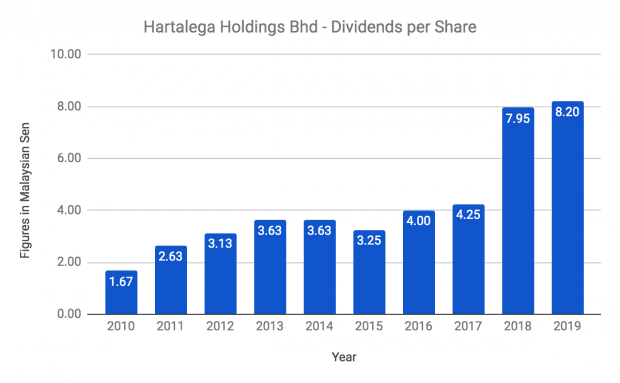

10. Dividend yield: Hartalega paid 8.20 sen in dividends per share (DPS) in FY2019. DPS was substantially higher in the last two years as the company revised its dividend policy to distribute a minimum of 60% of net profits, up from 45% previously.

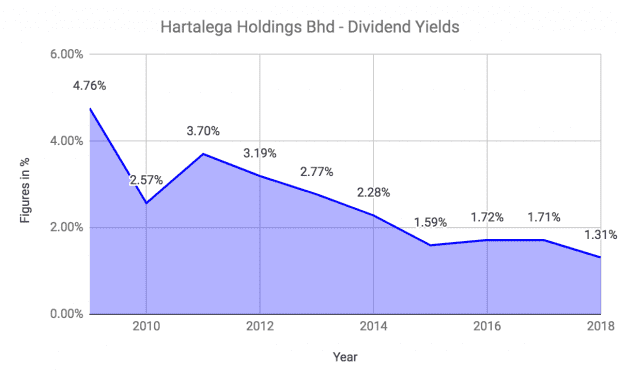

Hartalega’s current dividend yield is 1.60%, which is below its 10-year average of 2.56% per year.

The fifth perspective

Hartalega has built a track record of steady growth in revenue and profit over the last 10 years. Global demand for nitrile gloves looks set to continue and the pending completion of Plants 6 and 7 will increase Hartalega’s annual production capacity to 42 billion gloves to meet the growing demand. At the same time, Hartalega’s current stock price means it’s trading above its long-term valuation averages and offers a lower than average dividend yield.