I would like to share with you an embarrassing moment in my recent stock investing experience.

It was regarding a newspaper company in Hong Kong, Sing Tao. But I need to give you the background before I can tell you about the embarrassing moment.

Similar to SPH, Sing Tao and the rest of the newspaper companies, have seen declining sales and profits as advertisers move more of their advertising budget online.

But SPH wasn’t selling at undervalued prices despite the bad news. Sing Tao on the other hand presented a super undervalued case, and became a better choice for value investors like myself.

Although they sell newspapers in different countries, they are linked to the same owner in history. Aw Boon Haw had stakes in both Sing Tao’s and SPH’s predecessors. SPH’s Lianhe Zaobao is a union of Aw’s Sin Chew Jit Poh and Tan Kah Kee’s Nanyang Siang Pau. Aw is also known for Tiger balm as well as the scary Haw Par Villa.

I digressed. I picked up the Sing Tao in 2016 and presented it as a case study to our graduates. The book value was HK$2.38 while the share price was just HK$1. Comparing this to SPH where its book value was S$2.18 and share price was around S$3.20. Even though they were in the same business, Sing Tao was a better undervalued buy than SPH.

Below is a screen shot of the data I showed to the graduates and some of you who knows the CNAV strategy would be able to understand this.

We focused on the assets more than the businesses when we buy undervalued stocks. Many times, the valuable assets are sold at a steep discount that it doesn’t make sense and the business comes to us for free. Hence the business becomes a red herring that most people get distracted upon and miss out the assets the company is sitting on.

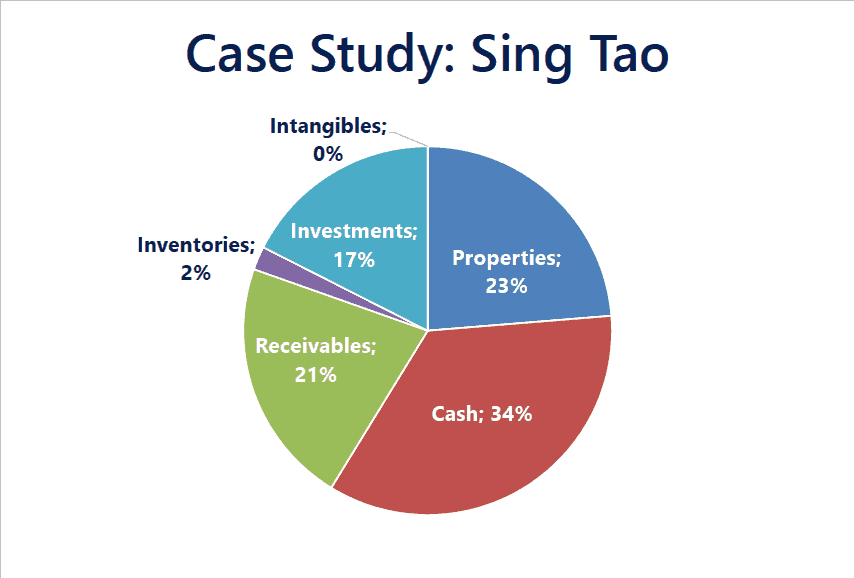

Sing Tao had 34% of its total assets in cash and another 23% in properties. These are good assets that hold value well over time. The properties were either office properties for their operations or rented out for income and located in Hong Kong, Beijing, New York, Los Angeles, San Francisco and Toronto.

If we just take the properties and cash, and net off the total liabilities, we still get HK$1.16 per share. This means that the stock market is willing to sell you (HK$1) less than the cash and properties they have.

Sing Tao owns several major papers such as Sing Tao Daily and The Standard. The former received the second largest amount of advertising volume in 2015.

It also owns the most distributed free Chinese paper in Hong Kong. This shows that Sing Tao’s market share of the newspaper business is quite large and not shabby at all!

The market probably discounted the stock severely based on the steep decline in sales (-13%) and profits (-88%) from a year ago. But it still doesn’t make sense to price the stock below its cash and properties.

I also like to see a the director having significant ownership in the company and Sing Tao makes the cut whereby the Chairman, Charles Ho, owns 49% of Sing Tao. He’s the largest shareholder and the skin in the game give some degree of confidence that his interest is aligned with shareholders.

So I took a position in Sing Tao on 24 Oct 2016 since the stock ticked all the boxes.

The newspaper business didn’t improve after I bought the stock but the stock prices held on well. The unexpected thing was that the management decided to distribute the large cash pile in the company and continue to give out increasing dividends each year as I held the stock. My dividend yield ranged from 9% to 13%, far exceed the dividend yield of 4-5% you would get from SPH.

That’s the good thing about buying deeply undervalued stocks backed by valuable assets – the dividend yield can be very high because of the low price you got in. Moreover, the bad news can’t get much worse but slight good news can give you a significant gain.

I sold it on 31 Oct 2019 as we have a holding period of 3 years. It was a total gain of 31%. Not very fantastic but a decent result nonetheless.

Here comes the embarrassing part – the share price jumped 16% as soon as 5 minutes after I have sold! Ouch!

I had to remove the stock from my monitoring list so that I can forget about it.

But I kept checking. I couldn’t help it. I’m only human.

It went up another 9.8% the next day and another 10+% the day after.

I could have as high as a 102% gain instead of a 31% if I had sold later. But no one can sell at the top and we all will have regrets like this. Well, we just have to move on.

Below is a chart and the labels of the milestones holding the stock.

The reason for the sudden rise in the stock was because there was an external party who was in talks with the management to buy over the company. Value investing works because most undervalued stocks cannot stay undervalued for too long as the price attracts competitors and investors to buy them up. Sing Tao is one of the many examples.

Conclusion

Not everyone can accept deep value investing. Many people say they are value investors but in my view, they aren’t. The real classic investors buy cheap on assets. The modern definition has been shaped by Warren Buffett to buying good businesses at fair prices. I prefer to call it growth investing instead.

Value investing is about buying unloved stocks. Most people like to buy popular stocks.

Value investing often venture into lower liquidity stocks. Most people feel the share price isn’t going anywhere and shun them for popular stocks.

Value investing may guide you to buy a declining business in a sunset industry. Most people are too uncomfortable and prefer to buy popular stocks because they feel ‘safer’.

Many people think they are contrarian and practise second-order thinking. True value investing is uncomfortable and uneasy. At the end of the day, it is either you get it or you don’t.

Are you a value investor?

We run courses on deep value investing. If you wish to learn, you can register for a seat here.