Since I started investing in 2014, I noticed that majority of investors’ money continues to flow towards certainty, at any price, and flees from the most cyclical and/or “unfashionable” stocks, despite the attractiveness of the companies’ valuation.

Over the years, this has given me opportunities to invest in such overlooked companies for huge appreciation in the long-term: waste management company 800 Super(SGX:5TG) to wireless device maker Powermatic Data (SGX:BCY) & recently, shipping companies.

I guess why Value Investing seemed especially appealing to me is also partly due to my character; I’ve always wanted to be different from the mainstream.

Currently, the commodities sector is one of the most unloved sectors. Supply and demand factors have caused prices to fall.

Among the different assets, this one piqued my interest:

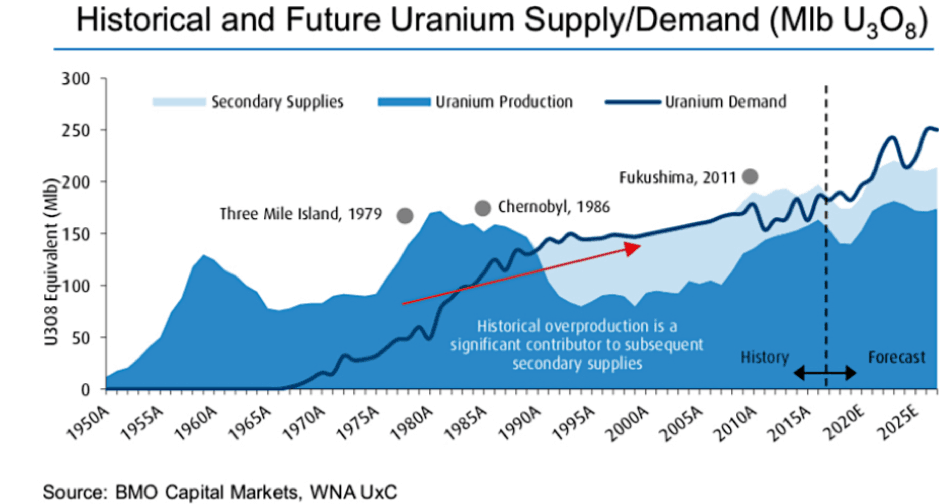

A little bit of background, Uranium prices peaked in 2007 after a series of events:

- Reduction of available weapons-grade uranium from Russia

- Growing nuclear programmes in India and China

- Flood of Cigar Lake Mine, Saskatchewan, home of the world’s largest undeveloped high-grade uranium ore deposits.

The bubble finally burst in 2007 and prices hovered around the cost of production for the uranium miners before recovering sharply when the Chinese appetite for uranium increased.

The rise in price was short lived, however, when the Fukushima Accident occurred which led to countries like Japan and Germany denuclearizing and closed dozens of nuclear reactors.

As such, demand for nuclear fuel decreased and uranium prices plunged even further, forcing miners to close or mothball their mines.

Plainly speaking, the problem with uranium is one of oversupply, which was triggered by the Fukushima Accident nearly a decade ago. Miners couldn’t react in time when several plants went offline and they were caught sitting on unprofitable stockpiles.

However, although still too early to be 100% sure, the supply-demand imbalance seems to be correcting itself and is ready to begin its long-awaited recovery.

1. Background

When you talk about uranium, nuclear energy always comes into the picture. An article by Nuclear and Energy Studies (NEA, 2012) revealed Nuclear Energy is the most efficient alternative energy source, & that using nuclear or renewable generation to produce electricity results in far lesser greenhouse gas emissions as compared to fossil fuels.)

Also, the table below shows that nuclear energy is the cheapest alternative electricity generation source in 4 countries: France, Korea, United Kingdom and United States:

– System Costs taken from Nuclear Energy and Renewables (NEA, 2012).

As countries pledge efforts to fight climate change, we see more and more of them committing to net-zero carbon dioxide emissions.

A recent study by MIT revealed that to achieve a “deeply decarbonized energy future”, there is a need to realise nuclear energy’s potential.

An article by Forbes brought up HUGE challenges to realise a net-zero carbon dioxide goal by Year 2050.

In its World Energy Outlook Report by IEA published in 2019, nuclear energy only met about 10% of global energy demand.

Also, despite how ‘clean’ electricity looks, more than 30% comes from burning coal today.

In summary, in order to ultimately deliver a low carbon future, nuclear is an important part of the energy mix as it brings a cost-competitive low carbon generation option to the table.

2. Supply

Low uranium prices made exploration projects and new mine development uneconomical.

Current costs of production for most companies is nearly twice the uranium spot price. Many uranium producers are reducing production over the years in response to the low price.

Uranium Producers Reducing Output

Kazakhstan’s JSC National Atomic Company Kazatomprom, the world’s largest uranium producing nation, says it will continue to cut production by 20% through 2021, rather than to the end of 2020 as originally planned.

The company also indicated production will not resume until market conditions signal a need for more uranium: 20% alone represented 8% of global annual output.

Cameco, the largest uranium mining company in the world, announced that it will indefinitely shutter its McArthur mine until prices recover. This mine alone produced 11% of the world’s annual uranium output.

In total, an estimated 25-35% of global uranium supply is already removed from the market.

*Why This Is Significant:

Most commodities producers would try to increase production so that they can make up for the lower prices. E.g. if a pound of “yellowcake” (Uranium) dips from US$60 to US$30, then producers will have to double their output, just to make up for loss revenue.

However, when everyone does this, it floods the market with excess uranium. Eventually, this would push prices even lower which will trigger a vicious cycle where producers continue to further increase output in an attempt to make up for larger losses in revenue.

The recent meaningful reductions in global uranium output meant producers were forced to accept reality that they need to cut production.

This resulted in a growing supply gap as we can see in the chart below – for the 1st time in almost a decade, we see a supply deficit in uranium production.

3. Demand

(i) Energy

Economic growth and a rising global population meant that worldwide energy demand is slated to increase. In 2018, China and United States accounted for nearly 70% of the rise in global energy demand (Source: IEA).

Nuclear also grew by 3.3% in 2018, with global generation reaching pre-Fukushima levels, mainly as a result of new additions in China and restart of four reactors in Japan.

Worldwide, nuclear plants met 9% of the increase in electricity demand.

EIA projected an approximate 50% increase in world energy usage by 2050, with most of the growth led in Asia.

(i) Electricity

According to IEA, electricity is touted as the “fuel” of choice for society. Hence, energy policy making is ensuring the reliable and secure provision of affordable electricity, while meeting environmental goals.

Electricity demand is mainly due to the increase in end-user consumption in residential sectors as rising population and living standards increase the demand for appliances and personal equipment.

There is also the rising popularity of using electricity to power transportations, from rail to cars to even bicycles.

(ii) Nuclear Energy Contribution

As global demand for energy and electrical energy grows, nuclear energy is expected to be a key aspect of contributing to the energy mix. As stated above, 10% of the global energy output comes from nuclear energy.

Even if the percentage remains the same, the gradual increase in total energy demand would lead to a rise in demand for nuclear energy.

(i) Nuclear Power Capacity

There are about 450 nuclear power reactors in the world, with about 50 more reactors under construction, which would add 15% more output to the existing capacity.

According to World Nuclear Association, current global operable reactor energy capacity is 394,000 MWe while there is another 53,300 MWe soon to be added due to new reactors.

Here is a geographic breakdown of current and expected capacity:

China and India are committed to grow their nuclear power capacity as part of their major infrastructure development programme. China also has an added incentive to improve their urban air quality reduce greenhouse gas emissions.

From the chart below, after the 80s, we saw growth in nuclear plants starting to plateau, with only an average increase of 1.2 reactors in operation every year. But now we are starting to see a sharp increase in reactors till 2030.

However, not all nations are receptive to nuclear energy after the Fukushima accident e.g. Germany decided to phase out nuclear generation as part of their Energiewende policy. This excludes additional 120,000 MWe in reactors which have not commenced construction and additional 300 more reactors which have been proposed.

This could mean that demand for uranium will more than double by 2030 (See source here).

4. Catalyst for Price Recovery

Supply Demand Imbalance

This is where it gets interesting: From production figures provided by the World Nuclear Association, total world production of uranium in 2018 was 53,498 tonnes.

The 450 reactors worldwide require some 63,000 tonnes of uranium each year. Each GWe of new capacity coming online would require 150 tonnes/year of uranium and 300-450 tonnes for the initial fuel load.

So what we are seeing here is a case where demand will increase over the next decade while supply will stay consistently below global demand unless prices recover, creating an increasing supply gap.

Assuming more mines will halted operations & await price recovery, restarting mines will not happen in a day.

The shortest timeframe we are looking at is 12 months for open pits and even longer for underground mines.

This could further enlarge the supply-demand gap.

Sellers’ Market

In nuclear reactors, uranium only accounts for 3% of the total cost for electricity production.

Hence cost of electricity is highly inelastic to any price changes in the Uranium spot price. It also does not make economic sense for the nuclear reactors to halt production just because uranium prices increase. Therefore, utilities are ‘Forced Buyers of Uranium’ in order to keep their reactors running. This also means makes the demand for uranium easy to forecast.

Long-Term & Short-Term Woes

Everything in Uranium is long-term based: You do not come to the market right before you need to load uranium into your reactors which are meant to run for the next 60 years.

Customers usually would try to secure long-term contracts to ensure of supply. However, this changed when uranium prices were so much lower and there is an excess supply that utilities do not see the need to secure production and purchase uranium off the market directly.

Even the producers themselves are purchasing physical uranium off the market:

- May 2019: Cameco announced to ramp up purchase of uranium to 7000-8000tones to meet their sales commitment while they mothball their mine at McArthur River.

- Production cuts and the reduction in producer inventories will increase demand of uranium in the spot market.

When the supply gap widens, these utilities would start to worry about the availability of future supply to fill demand. Therefore, this could be a catalyst when we see utilities re-entering long-term contracts to ensure they can have the reliable supply of uranium.

If uranium prices increases exponentially due to supply crunch, the reactors might be forced to sign contracts with a price premium.

In my opinion, this could happen soon because utilities are beginning to run out their contracts and, referring to the graph below, by 2022-2023, there would be only 50% of global uranium demand in long-term contracts.

5. Investing in Uranium

There are many ways you could ‘play’ the uranium sector. However, I will categorize it into 2 groups, namely mining and physical uranium.

(i) Mining

The mining industry is one of the hardest sector to invest in. Honestly, I would discourage it unless you are specialised in this sector; that can analyse on a mine-by-mine basis and understand geology reports which will inform you miners with the best resources.

But if you really want to put your money in the mining industry, there are 2 companies that I would recommend you to start your due diligence in.

1. Cameco (TSE:CCJ)

Cameco is the 2nd largest uranium producer in the world, contributing to 15% of the world’s supply. This company has solid cash flows even in an extremely challenging market environment. Their adjusted Free Cash Flow (‘FCF’) in 2018 amounted to C$647mil on the back of C$2.1bil revenue. Its YTD Q3-2019 FCF is C$317 on the back of C$988mil rev.

NOTE: Total FY revenue is back-end heavy with about 50% coming in Q4. This would mean that their FCF is consistent with FY2018 levels.

I’m of the view that Cameco is one of the better-managed mining companies.

Having long-term supply contracts at around US$36/lb and faced with the cost of production at US$31/lb, the management decided to close down their McArthur River mine and purchase uranium to meet supply requirements in the spot market, priced at around US$20/lb.

Hence this makes more financial sense for them to expend excess inventories and help get uranium prices back to a more sustainable level.

Another reason why I prefer this company to Kazatomprom, the world’s largest producer, is because their mines are in the Athabasca Basin in Canada, the world’s highest-grade uranium district, with 10 out of 15 highest grading uranium deposits located in this region.

Cameco’s McArthur River mine, which is located in this area, is the world’s largest high-grade uranium mine.

2. Paladin Energy (ASX:PDN)

Production costs is the primary litmus test for measuring competitive advantage in the highly cyclical mining industry. All producers can generate fat returns on capital when commodity prices are high, but only ‘lowest-cost’ producers can generate excess returns on capital.

Paladin Energy owns 75% stake in the Langer Heinrich, a large open pit mine in Namibia with one of world’s largest uranium reserves. The mine is currently placed in care and maintenance.

Depending on which sources you look at, the sustainable price for uranium production ranges from US$40-US$70 per pound. The Langer Heinrich mine’s all-in production cost is about US$28/lb.

If Paladin decides to restart, being an open pit mine, this mine could be up and running in about 12 months and could be one of the first mines resuming production.

With a low production cost, if the Langer Heinrich mine restarts when Uranium prices recover to >US$40, Paladin Energy would enjoy about US$40mil of cash flow and will significantly increase as prices recover above US$40.

Paladin’s assets are excellent but with rising debt levels, this company is currently with its back against the wall if the downturn persists longer than expected.

(i) Physical Uranium

Another option is to buy the physical metal itself. Unlike its other yellow metal counterpart, you can’t just buy a few barrels of yellowcake back and store it in your safe.

Luckily for us, there are two specialty companies that buy and store physical uranium without all the mining risk. Uranium Participation Corp (TSE:U) and Yellow Cake PLC (LON:YCA)

1. Yellow Cake PLC (LON:YCA)

Yellow Cake PLC offers investors exposure to the uranium market without the operating risks associated with exploration, development, mining or processing. Their main business is to purchase and store uranium.

Trading of uranium is managed by a company called 308 Services Limited. They are paid in a flat fee plus US$275,000 and variable fee of 0.275% AUM over US$100mil. They are also paid a 0.5% commission charge whenever there is a sale or purchase.

Yellow Cake gets most of their uranium from Kazatomprom. Both have an agreement indicates Yellow Cake has the right to purchase US$100mil of uranium annually for 9 years.

In return, Kazatomprom has the option to repurchase up to 25% of the Initial Uranium Purchase (about US$170mil) after 3 years at a discount but only if price of uranium is above US$37.50/lb. Yellow Cake PLC currently holds 4363 tonnes of uranium.

Purchased uranium is stored Cameco’s Port Hope/Blind River facility in Ontario, Canada.

In addition to just buying and storing uranium, Yellow Cake PLC and Uranium Royalty Corp (which owns 9.9% of Yellow Cake PLC) have an agreement to share royalty opportunities.

*A royalty contract is one which gives the owner the right to a percentage of uranium production or revenue in exchange for upfront payment.

This is used to finance mining exploration companies and Yellow Cake stands to benefit from the exploration upside that may find new uranium source or extend the life of a mine.

Of course, this is a double-edged sword because changes in spot prices and mine production will impact the profitability of their investments.

Looking at their Finances: Recurring operating cost is about US$1.7mil while their NAV (Net Asset Value) is US$252mil. Cost to NAV is very low at 0.7% so we should not worry too much about Yellow Cake not being able to pay the management fees for the time being.

(In my opinion, the best way to valuate this company would be to use P/NAV.)

The current price of Yellow Cake PLC is £1.80 and their most recent NAV released in Oct 2019 was £2.08 – representing a 13% discount to the above estimated NAV.

P.S. To read more about Uranium Royalty Corp, here is an article by Katusa Research, a firm which specialises in mining & commodities. URC has also recently filed its preliminary prospectus of IPO.

2. Uranium Participation Corp (TSE:U)

For those who are not interested in the gimmicky business strategies and is looking for a “Pure Play” uranium play, Uranium Participation Corp (UPC) is the company you want.

Their business strategy is simple. Invest in holdings of physical uranium without actively trading. No royalties and no mining investments. (Basically, no nonsense).

Under a Management Services Agreement, Denison Mines Inc is appointed the Manager whose responsibility is to purchase, sell and store uranium on behalf of UPC.

UPC has more assets than Yellow Cake PLC at 7600 tonnes. Their Operating Expense relative to NAV is at 0.8%, which is roughly the same as Yellow Cake PLC.

At current share prices of CAD$4.21, its NAV (as of 30 Sep 19) of CAD$4.43 represents a 5% discount.

Its discount to NAV is much lower compared to Yellow Cake PLC but it could be due to Yellow Cake’s shareholders selling down.

NOTE: Yellow Cake also has agreements with Uranium Royalty Corp which would mean taking additional risks in their business.

Therefore, as an investor it really depends on you whether the deeper discount in NAV is worth the additional risks.

6. Risks

Uranium has been ‘bearish’ for almost a decade. ‘Low’ can go ‘Lower’. My thesis could fail due to unforeseen circumstances – risks, which may lead to sustained low prices for uranium.

(a) Nuclear Reactor Shutdowns

“In the 1980s there was a new nuclear reactor commissioned every 2½ weeks, on average. Today there are just 53 under construction world-wide, nearly all in Asia, according to the WNA, and many of the world’s 448 existing plants face decommissioning.”

– Wall Street Journal

In the nuclear sector, many power plants are considered very old. Reactors are on average 35 years old in EU & 39 in the US.

Most nuclear power plants originally had a nominal design operating lifetime of 25 to 40 years. If the cost to upgrade and to prolong their life is to high compared to the current price of electricity, the more economical way is to shut down the plant.

Currently, new units coming online have more or less been balanced by the retirement of old units in recent years. The World Nuclear Association’s 2019 edition of The Nuclear Fuel Report has 154 reactors closing by 2040 in its reference scenario, using conservative assumptions about licence renewal, and 289 coming online.

However, a reduction in both license renewal & planned nuclear plants could lead to a decrease in demand for uranium in the future.

(b) Renewable Energy

The renewable energy market is expected to increase by 50% in the next 5 years with solar and hydropower leading the charge. Their popularity could mean nuclear energy may no longer be the best alternative to clean energy.

Even if electricity demand rises over the years, the contribution by nuclear energy might stagnate or even decrease.

This is also due to the risks involved in building a nuclear reactor. Everyone has seen what Fukushima Accident did to Japan and the waters surrounding it. To avoid a repeat, countries could start to phase out nuclear reactors and use renewable energy to replace the gap.

(c) Thorium

Problem: Nuclear Reactors produce a lot of radioactive waste when extracting energy from uranium fuel rods. Scientists are experimenting with thorium as a critical alternative to uranium, in developing a cleaner, greener safer version of nuclear power.

To learn about the fascinating history of thorium and its potential for nuclear power generation, read Uranium’s ugly stepsister.

Any advancement in this technology could mean it’s time to ditch uranium & go with thorium.

7. Conclusion

“We are not restarting mines until we see a better market and we may close more capacity, although no decision has been taken yet.”

– Tim Gitzel,

Cameco CEO

“Kazatomprom does not expect to return to full production until a sustained market recovery is evident, and demand and supply conditions signal a need for more uranium.”

– Kazatomprom

CEO Galymzhan Pirmatov

When you have producers supplying over 50% of global uranium supply singing the same song, there is very high possibility they will succeed in forcing the price of uranium higher.

It is anybody’s guess on what is uranium’s ceiling but I think that it should be at least somewhere in the region of US$40-US$60 where it is sustainable to operate the mines.

The global demand for energy and worldwide electrification will lead to increased demand for uranium as more nuclear reactors are being built to contribute to the power grid.

As nuclear reactors in Japan started to come online, together with the newbuilds in China and India, these will drive up demand for uranium over the next decade.

As for the supply side, shutdowns of major uranium mines like McArthur River, Langer Heinrich and decreased production in Kazatomprom will ease the demand supply imbalance.

You also have funds like Yellow Cake PLC and producers Cameco buying off the spot market to reduce excess inventory.

In the next 5 years, half of the long-term contracts will expire. To ensure long-term sustainable uranium supply, utilities would be forced re-sign long-term contracts at a premium before the supply crunch comes in.

With so much buying going to come into the spot market, I’m confident uranium prices will see a brighter future as demand continues to improve and cumulative supply cuts draw down existing supply as buyers re-enter the market. If all the ducks are lined up properly, we could have ourselves a repeat of 2007.

Cheers!

Disclaimer: The Moss Piglet is not vested in any of the companies mentioned but is planning to initiate a position in Uranium Participation Corp (TSE:U) and Yellow Cake PLC (LON:YCA) in the next 3 months.

Interested To Learn More On How We Analyse Whether To Invest In A Company?

Seats are Filling Fast: Join us at our LAST FREE Stocks Investing 101 Workshop (2019).

You’ll discover whether you can invest in a particular stock within just 10 to 15 Minutes.

At Dr. Wealth, we approach the Stock market in a rather different way from others who teach Investing, But it works, & you can see this from over 180 reviews about us in Singapore’s Largest Personal Finance Community, Seedly.

URNM is a good way to play too. I was way too early, speculated on section 232 and bought UEC. Still holding the bag at a 30% loss

Hi,

Thanks for analyzing the potential of commodity of Uranium. Your sharing is coming on time which I intended to seek help if there is an overview or related data that DW able to extract data for companies involving in the sector of renewable energy. As I am overwhelmed with online data and not sure where should I start.

Refer to your article above on the Risks session: “Their popularity could mean nuclear energy may no longer be the best alternative to clean energy.” Agree with you and not foreseeing nuclear will be the alternative clean energy for next decade.

Some findings and own opinion from insurance perspective point of view:-

– Conventional Power includes the combustion of fossil fuels (coal, natural gas, and oil) and the nuclear fission of uranium.

Challenges of conventional power project include Financial Funding/Lending (extensive cost, safety, humanity & Financial Risk transfer to (Re)Insurers on conventional power project especially for nuclear and coal probably not insurable in future.

References:-

https://www.oecd-nea.org/ndd/reports/2009/financing-plants.pdf

http://ieefa.org/wp-content/uploads/2019/02/IEEFA-Report_100-and-counting_Coal-Exit_Feb-2019.pdf

– Renewable energy which rely on sources include sun, wind, moving water, organic plant and waste material (eligible biomass), and the earth’s heat (geothermal). Most of countries will be focusing on Green Power.

– with Paris Agreement signed in 2016 – to mitigate global climate change; and those OECD countries will be focusing to change/shift to clean energy.

Investment perspective, wish if there is an overview or analysis on companies who are involving supplying for solar panel, wind turbine etc at the same time fulfills the fundamental analysis for investors’ reference. Not sure if this is feasible. Let me know how I can help to contribute as well.

List of publicly traded renewable energy companies:-

https://en.wikipedia.org/wiki/List_of_renewable_energy_companies_by_stock_exchange

List of wind turbine manufacturers:-

https://en.wikipedia.org/wiki/List_of_wind_turbine_manufacturers#Current_manufacturers

Let me know if you need further info on current position of Global (Re)Insurers towards nuclear power energy. I can speak to them and gather the most latest info.

Thanks.