Disclaimer: Neither the author nor Dr Wealth are responsible for losses you incur. Naturally, neither will we profit from your wins. Caveat Emptor, people.

Many precision engineering firms listed in Singapore have been privatised in recent years, such as Armstrong, Fischer Tech, Innovalues, Interplex, etc. Spindex is nearly one of them, as it was the subject of a competitive bid between a holding company privately held by Spindex’s chairman and a private equity fund in 2017.

It was not much of a bidding war, as the chairman soon emerged victorious by increasing his shareholding from 24.4% to 72.4% of the company.

What makes this company so interesting to be the subject of a competitive bid? Let us look at the strengths and risks of this company below.

Strengths

1. Low-Cost Manufacturing Base

Spindex is in the business of precision manufacturing. It manufactures precision parts that are used in printers, cars, washing machines, etc. It has 4 factories located in China (Suzhou and Shanghai), Vietnam and Malaysia. A 5th factory is planned to be built in Nantong, China in 2021. It used to have a factory in Singapore, but has since closed it and moved operations overseas.

Compared to Singapore, land, factory and labour costs in China, Vietnam and Malaysia are all cheaper. As an example, the cumulative cost paid by Spindex for all the freehold/ leasehold land in these countries is only SGD7.1M. In comparison, the market value of the leasehold land in Singapore was SGD4.1M when Spindex surrendered it back to JTC in 2017 after closing the factory.

Revenue is generated in USD, but part of the costs are in the local currencies (Renminbi – RMB, Vietnamese Dong – VND, Ringgit Malaysia – RM). The advantages are similar to a worker earning a salary in Singapore but staying in Malaysia. That is probably the biggest strength the company has.

2. Relative Immunity from US-China Trade War?

When US initiated the trade war with China in 2018, some manufacturers started to look at relocating their factories outside China, such as Vietnam. However, long before the trade war begun, Spindex had already established a factory in Hanoi, Vietnam in 2004. All the factories that Spindex has are certified to produce automotive parts. So, Spindex has first-mover advantage if supply chains start to move to Vietnam.

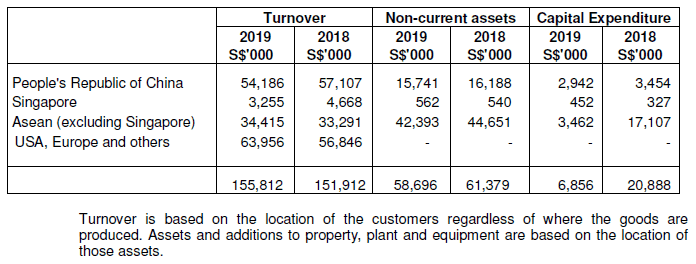

Having said that, with 2 factories in China, will Spindex find itself losing business in China when supply chains move? Let us take a look at the geographical distribution of revenue based on location of Spindex’s customers in Fig. 1 below.

Revenue for customers in US are at the most risk of the trade war. For the Financial Year ending in Jun 2019, customers in US, Europe & Others generated a total revenue of SGD64.0M, or 41% of the total revenue. We do not know how much of these US-based revenue is generated from factories in China, however, a glance at the distribution of non-current assets in the various countries in Fig. 1 above tells us where most of the manufacturing capacity is located.

Out of the SGD58.7M of non-current assets (mostly plant, property & equipment), SGD43.0M (or 73% of the total) are located outside China. This suggests that majority of the US-based revenue are generated from factories outside China.

Next, will part of the China-based revenue actually be meant for export to the US? Fig. 2 below shows the breakdown of revenue according business segments and countries where the customers are based.

Customers in China generated a total revenue of SGD54.2M, or 35% of the total revenue. Out of the SGD54.2M revenue, 84% comes from Machinery & Automotive (M&A). Given that vehicle population in China is still growing, it is likely that Spindex’s M&A customers are manufacturing and selling their vehicles in China instead of exporting them to US. Hence Spindex’s M&A business in China are unlikely to be affected by the trade war between US and China.

Although the Imaging & Printing (I&P) business in China might be affected, it only constitutes 14% of the revenue generated from China. In any case, given that Spindex already has factories in Vietnam and Malaysia, if Spindex’s I&P customers were to move to these countries, Spindex would be able to retain the I&P business.

Thus, Spindex should be relatively immune to the trade war, i.e. increase in tariffs for US-bound goods exported from China and relocation of supply chains from China to ASEAN countries. Nevertheless, it might still feel some impact arising from the cooling of China’s economy due to the trade war.

3. Customer-Oriented

Being a small precision engineering firm, Spindex has many competitors. However, one key strength that Spindex has that allowed it to thrive to-date is being customer-oriented. It has won several awards from its key customer, Bosch, including:

- “Preferred Supplier” award in 2010

- “Long-Term Strategic Partner – 20 Years” award in 2013

- “Superior Quality and Excellent Performance” award in 2017

The awards are testimony that Spindex is able to provide high-quality products and good customer service to its customers. Assuming Spindex can continue to do so in future, Spindex can count on continued business from them.

Risks

1. Customer Concentration

Although Spindex can count on Bosch for continued business, it also means that Bosch accounts for a large portion of Spindex’s business. Losing Bosch’s business will have a major impact on Spindex’s profitability.

For Spindex, key customers with revenue more than 10% of the total revenue account for 60% of the revenue in the M&A segment and 52% of the revenue in the Others segment. In total, key customers account for 43% of the total revenue.

Spindex will need to take extra care to ensure that it does not lose its key customers. On the positive side, because it cannot afford to lose its key customers, Spindex will spare no efforts in ensuring high-quality products and good customer service to its key customers.

One area that needs to be watched is mergers & acquisitions involving its key customers. When 2 companies merge, there will be rationalisation of both companies’ supply chains. Existing suppliers could either gain more business from the merged entity, or lose the entire business.

2. Foreign Currency Exposure

Being in an industry in which business is transacted in USD and having factories in various countries, Spindex has exposure to foreign currencies (USD, RMB, VND, RM). In FY2019, approximately 68% of the revenue is denominated in USD while 14% of the costs are denominated in RMB, VND and RM. Thus, there is a mismatch between revenue and costs, exposing Spindex to currency risks. Sensitivity analysis shows that a 10% decrease in USD relative to SGD would decrease pre-tax profit by SGD4.23M (or 23.5%) in FY2019. Conversely, a 10% increase in USD relative to SGD would increase pre-tax profit by the same amount.

More generally, there are 3 types of impact from forex exposure, namely:

- Transactional – Arising from impending cashflows, e.g. sales, payments, etc.

- Translational – Arising from assets and liabilities on the balance sheet, e.g. foreign currencies, factories in overseas countries, etc.

- Economic – Arising from changes in competitiveness due to forex movements.

When USD appreciates against SGD and SGD appreciates against RMB, VND and RM as is the case in FY2019, the effects are as follow:

- Transactional – Favourable. Sales are in USD while labour costs are in RMB, VND and RM. In SGD terms, sales are higher while costs are lower. For FY2019, Spindex reported forex gains of SGD0.3M and reduced administrative expenses of SGD0.5M.

- Translational – Generally unfavourable. Spindex has factories in China, Vietnam and Malaysia. These assets will have lower value in SGD terms. On the other hand, Spindex holds cash in USD for operational needs, which will have higher value in SGD terms. As the amount of property, plant and equipment is higher than USD deposits, the net effect is unfavourable. For FY2019, Spindex reported forex translation loss of SGD3.5M, which is equivalent to 23% of its net profit. Nevertheless, this loss has not much relevance, since Spindex has no intention to sell away its factories in China, Vietnam and Malaysia and convert the proceeds back into SGD. It is a paper loss only.

- Economic – Generally favourable. Depreciation of RMB, VND, RM relative to other currencies means that Spindex is more competitive relative to its competitors in other countries. However, the economic effects of forex exposure usually cannot be quantified.

Thus, when USD depreciates against SGD, RMB, VND and RM, it is negative for Spindex even though it will post a forex translation gain under other comprehensive income. As an example, in FY2018, Spindex’s pre-tax profit decreased by 7.6% while posting forex translation gain of SGD2.5M.

3. Leadership Transition

Spindex is a family-owned business. The current chairman, Mr Tan Choo Pie, is currently 73 years old. He has handed over the company’s management to his son, Mr Tan Heok Ting, who is 39 years old. The younger Mr Tan has been the Managing Director since 2013. However, when there are leadership changes, there are always uncertainties in the strategic directions of the company, especially when the elder Mr Tan retires from the company. The younger Mr Tan might take the company to new heights, or might make too many changes, to the detriment of the company.

Financials

I seldom write about a company’s financials (EPS, NTA, valuation, etc.) in my blog posts because these are all backward-looking metrics. Without an understanding of the business, one can never be sure whether the historical performance will continue. However, for Spindex, I will make an exception, but I will let the charts themselves do the talking. The 2 charts below shows the revenue, pre-tax profit, earnings per share and Net Tangible Assets for the past 10 years. Clearly, Spindex is a growing company, with revenue, pre-tax profit, earnings per share and NTA doubling over the past 10 years.

Conclusion

Spindex is a small but growing company. Its key strengths include having a low-cost manufacturing base and being customer-oriented in serving multi-national corporations in the region. The geographical diversification of its factories allows it to be relatively immune to the ongoing trade war between US and China.

On the other hand, key risks include heavy reliance on several key customers, foreign currency exposure and leadership transition. Do note that some of the strengths and risks go hand in hand. For example, being customer-oriented enables Spindex to win the business of MNCs, but it comes at the cost of increasing customer concentration.

Being located in several different countries provides geographical diversification and relative immunity from the trade war, but there is increased foreign currency exposure. As the saying goes, “no risks, no gains!”

So far, Spindex has been able to manage the risks well. I am happy to continue as a shareholder.

Editor’s notes: Using the G5D5 Strategy, we invest in only the very best of stocks. Our analysis will differ slightly here in that we think we’ve missed the boat on Spindex. It’s price has gone up and rightly so given its long consistent track record. More so, I like it when insiders care enough about their business to try and retain control by buying up to and controlling 75% of the ownership. I would consider the chances of shareholder value being destroyed much lower. Watch this carefully and enter on opportunities presented!

If you’d like to know how we invest at Dr Wealth, feel free to register for a seat here to find out more.