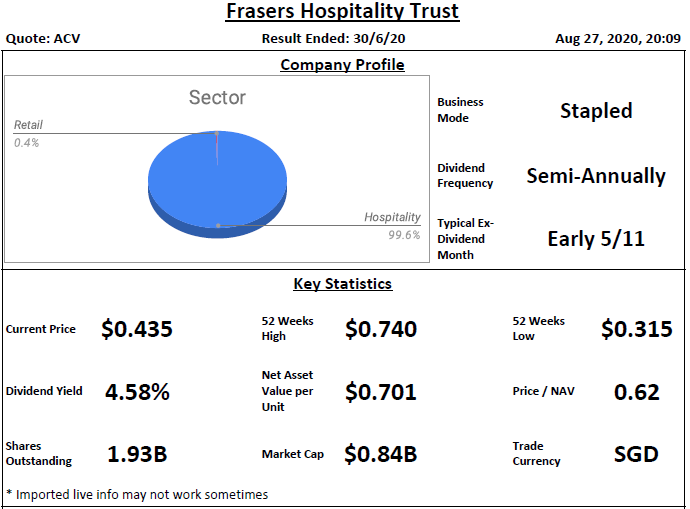

Basic Profile & Key Statistics

Frasers Hospitality Trust (FHT) is a stapled group comprises of Frasers Hospitality Real Estate Investment Trust (“FH-REIT”) and Frasers Hospitality Business Trust (“FHBT”). FHT invests in 15 hospitality properties across 9 key cities in Asia, Australia and Europe. Its japan property - ANA Crowne Plaza Kobe has a small portion of income from retail.

Lease Profile

In the latest business update, FHT only announced countries REVPAU without revenue contribution weightage, so we are unable to calculate weighted REVPAU, but all the countries REVPAU are not rosy. WALE is long at 13.55 years, which excluded Novotel Melbourne on Collins as it is an internal master lease arrangement between FH-REIT and FH-B. Weighted average land lease expiry is long at 81.85 years.

Debt Profile

Gearing ratio is healthy at 35.9%. Cost of debt if low at 2.3% with high unsecured debt % at 96.3%. Fixed-rate debt % is low at 71.9%. Interest cover ratio is low at 3.2 times. WADE is long at 3.88 years where the highest debt maturity of 30% falls in the year 2024.

Diversification Profile

Top geographical and top property contributions are estimated to be at 20.9%, which is low for top geographical but moderate for top property weightage. Top tenant and top 10 tenants contributions are high at 16.8% and 92.3%.

Key Financial Metrics

Property yield is low at 4.3%. FHT retaining S$ 25.3 mils from distribution, therefore affected management fees over distribution, distribution on capital, and distribution margin, the values are 29.5%, 2.2%, and 28% respectively. Without retention, the values would be 15.7%, 3.3%, and 52.8% respectively. Management fee is still not competitive which unitholders receive S$ 6.37 for every dollar paid, while distribution on capital and distribution margin are moderate. However, as FHT never announce the latest quarter financial result, so we are unable to know the detail for retained distribution.

Related Parties Shareholding

As compared to SREITs median, sponsor, manager and directors of REIT manager are holding higher stake.

Trend

If we look at post rights issue from 4Q 2016 to pre-COVID. DPU and distribution margin are at downtrend while NAV per unit is at a slight downtrend.

Relative Valuation

i) Average Dividend Yield

Dividend yield of 4.58% is based on annualized DPU for the past 1 year. Apply annualized DPU of 1.992 cents to average yield of 6.74% will get S$ 0.295. However, if we take annualized DPU without retention , we will get 3.746 cents, which translates into S$ 0.555.

ii) Average Price/NAV

Average value is at 0.92, apply latest NAV of S$ 0.701 will get S$ 0.645.

Author's Opinion

| Favorable | Less Favorable |

|---|---|

| WALE | Interest Cover Ratio |

| Weighted Average Land Lease Expiry | Top Property Weightage |

| Cost of Debt | Top Tenant & Top 10 Tenants Weightage |

| Unsecured Debt | Management Fee |

| WADE | DPU Downtrend |

| Top Geographical Weightage | Distribution Margin Downtrend |

Since April, all UK properties were closed and only resumed operations in August. The Westin Kuala Lumpur in Malaysia has also temporarily ceased operations since May. However, Novotel Melbourne on Collins, Sofitel Sydney Wentworth, and InterContinental Singapore have the full quarter hosted for returning residents to serve quarantine orders. Hopefully, with the lifting of domestic travel restrictions in Australia, Japan and the UK and also green lane/fast lane open for more countries in Singapore could improve FHT performance in the coming quarters.

The above analysis information is extracted from SREITs Dashboard, you are welcome to use the information there for your analysis. You could also refer SREITs Data for an overview of Singapore REITs. If you like my sharing, please join the Facebook group - REIT Investing Community where you could read, share, and discuss REITs related topics. Please also invite your like-minded friends to the group.

*Disclaimer: Materials in this blog are based on my research and opinion which I don't guarantee the accuracy, completeness, and reliability. It should not be taken as financial advice or statement of fact. I shall not be held liable for errors, omissions as well as loss or damage as a result of the use of the material in this blog. Under no circumstances does the information presented on this blog represent a buy, sell, or hold recommendation on any security, please always do your own due diligence before any decision is made.

No comments:

Post a Comment