As you guys know, there are only four 12-month T-Bills issued each year.

And the next 12-month T-Bills auction so happens to be next week (20 April).

3 key questions I wanted to discuss today:

- What is the expected yield on the next 12 month T-Bills?

- For CPF-OA investors – 12 month T-Bills a good buy?

- For cash investors – 12 month T-Bills a better buy than 6 month T-Bills (or Fixed Deposit / Singapore Savings Bonds)?

What is the expected yield on the next 12 month T-Bills?

Let’s look at the market pricing data.

12 month T-Bills on the open market – 3.72%

12 month T-Bills trade at 3.72% on the open market today.

Note how close that is to the 6 month T-Bills – trading at 3.74%, and where the latest auction closed at 3.75%.

Based off this pricing the market expects interest rates to be flat (no hikes or cuts) 6 – 12 months from now (October 2023 – April 2024).

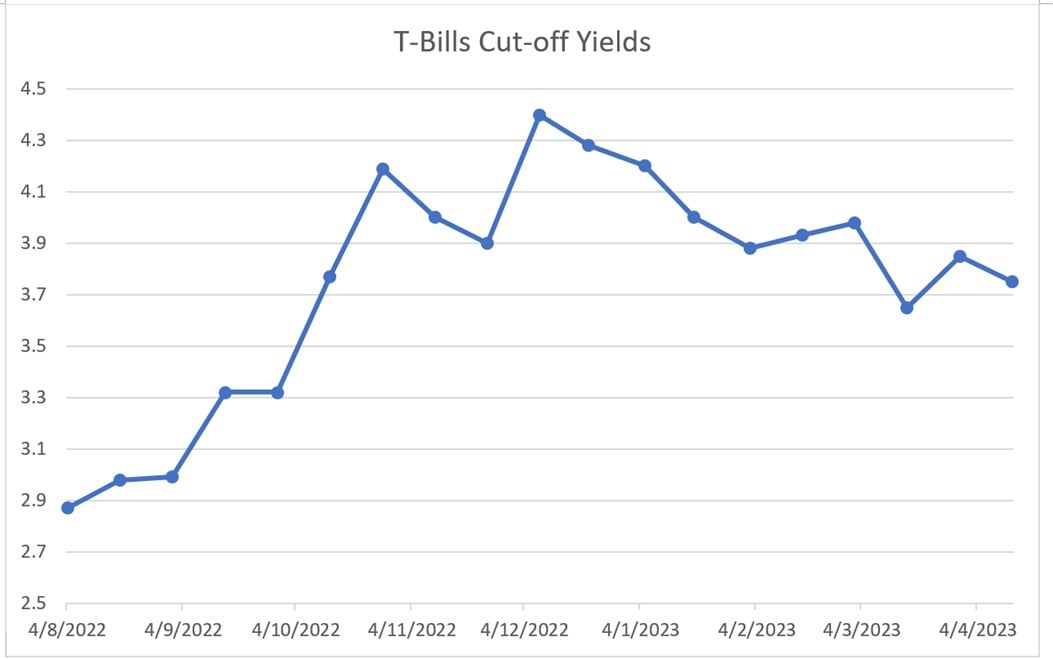

Interest Rate Trend is down

That said – the 6 month T-Bills are on a firm downtrend since December 2022:

The most recent 6-month T-Bills auction also had a final cut-off yield that came in below it’s market price.

This suggests a similar pattern might repeat with the 12 month T-Bills.

12 month T-Bills tend to close below market price

In any case – the same thing happened with the previous 12-month T-Bills auction back in January 2023.

The reason I suppose, is because 12-month T-Bills are prized by CPF-OA investors.

Demand from CPF-OA investors may be high

I myself wrote an article on this last week on why CPF-OA investors might prefer 12-month T-Bills over 6-month T-Bills.

It ultimately comes down to the fact that market yields on the 12-month an 6-month T-Bills are very close.

So locking in a 12-month T-Bills with CPF-OA today protects you from any unexpected rate cuts over the next 12 months.

And you don’t need to worry about rolling your CPF-OA into new T-Bills in 6 months time.

It’s simple, fuss free, and might even turn out to be the superior option if interest rates get cut.

If this turns out to be true, it might further skew yields to the downside.

12-month T-Bills auction on 20 April 2023 – Estimated yield of 3.6 – 3.7%?

Because of this, I think realistically the yields on the 12-month T-Bills auction might come in slightly lower than market pricing (3.72%).

I would probably go with a range of 3.60% – 3.70%.

As always, I encourage investors to submit competitive bids to protect against the risk of a freak result.

If 12 month T-Bills issued at 3.60% yield – still worth it to buy with CPF-OA?

Assuming the 12-month T-Bills fall within the lower end of my expected range (3.60%).

Does it still make sense to buy 12-month T-Bills over 6-month T-Bills with CPF-OA?

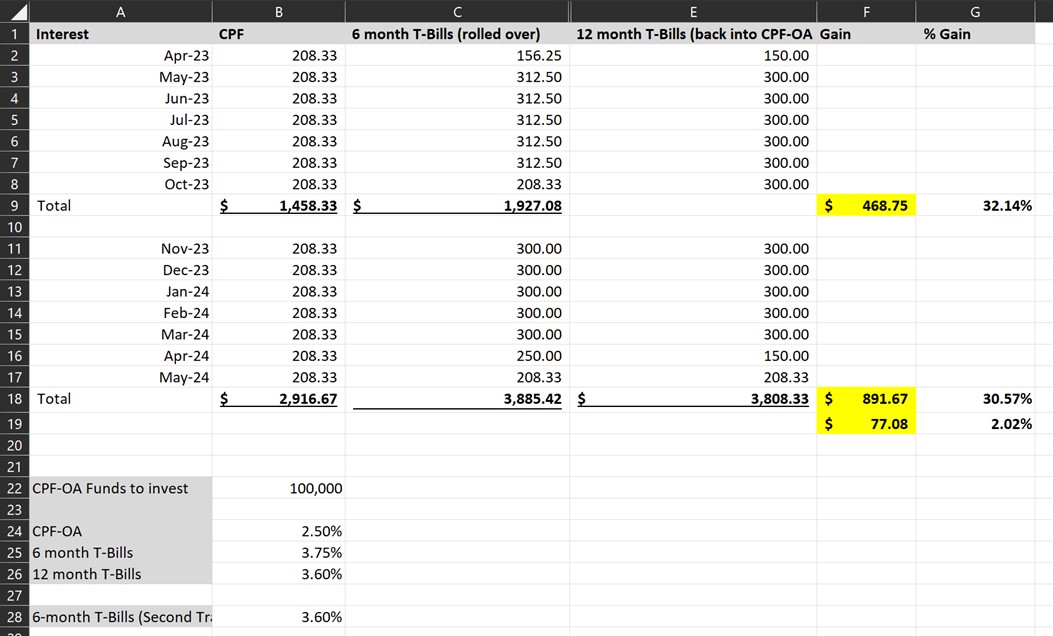

I ran the numbers below assuming that:

- 12-month T-Bills bought at 3.60%

- 6-month T-Bills bought at 3.75% (latest auction price)

- 6-month T-Bills rolled over at 3.60% (within the same month so no loss of CPF-OA interest)

Then the 6-month T-Bills option comes out only slightly ahead by $77.

But you do need to understand that there are 2 key assumptions above:

- That you can roll over the 6-month T-Bills in the same month (without losing another month of CPF-OA interest

- 6-month T-Bills can be rolled over at 3.60% in 6 months’ time

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

That you can roll over the 6-month T-Bills in the same month (without losing another month of CPF-OA interest

Let’s say the 6-month T-Bills interest rates drop to 3.40% in 6 months’ time – suddenly the 12-month T-Bill option comes out on top.

6-month T-Bills can be rolled over at 3.60% in 6 months’ time

And don’t forget the 6-month T-Bills option has you worrying about rolling over the T-Bills in 6 months.

That’s real time and effort there, whereas the 12-month T-Bills is fuss free for the next 12 months.

Don’t underestimate the peace of mind.

Personal View for CPF-OA investors?

So my personal here.

Is that if I can get the 12-month T-Bills at 3.60 – 3.70%, I probably would just buy it over the 6-month T-Bills.

It’s close enough to market pricing, it’s not that much lower than the 6-month T-Bills.

And it protects me against any unexpected interest rate cuts, and is fuss free for the next 12 months.

That’s probably what I would go for if I were applying with CPF-OA this month.

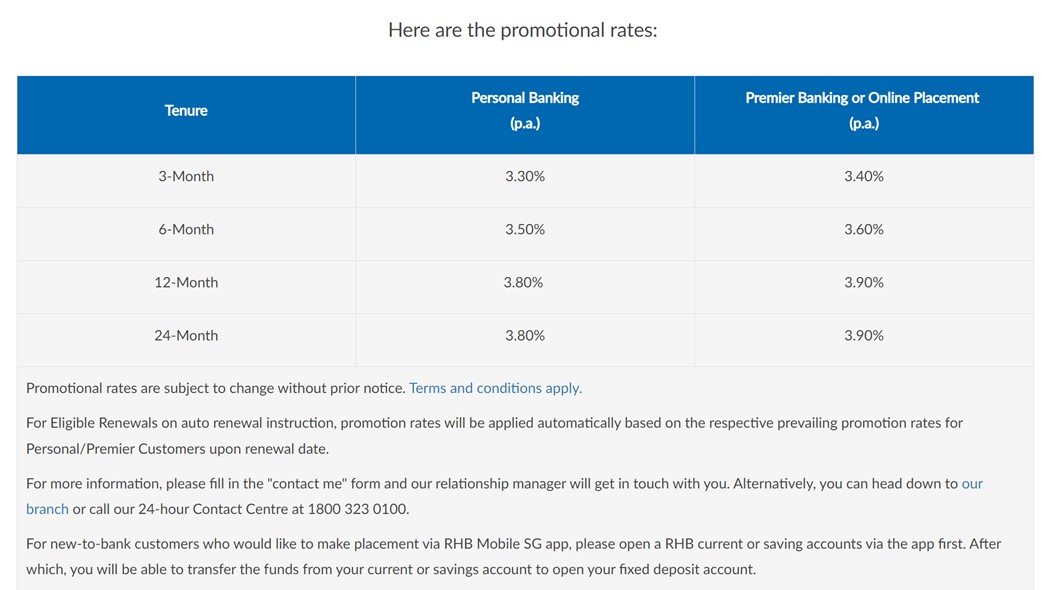

What about for cash investors – Fixed Deposit Rates yields up to 3.9%?

For cash investors though, I don’t think the 12-month T-Bills are all that attractive.

The highest yielding fixed deposit in the market right now is with RHB bank.

You can get 3.90% on a 12 month fixed deposit (4.00% if you are premier banking).

Minimum amount is $20,000.

With Fixed Deposit you even have the option of breaking it early and getting your money back by paying a penalty (usually you need to forfeit the interest).

So between a 12-month T-Bill and a 12-month Fixed Deposit – I would go with the Fixed Deposit.

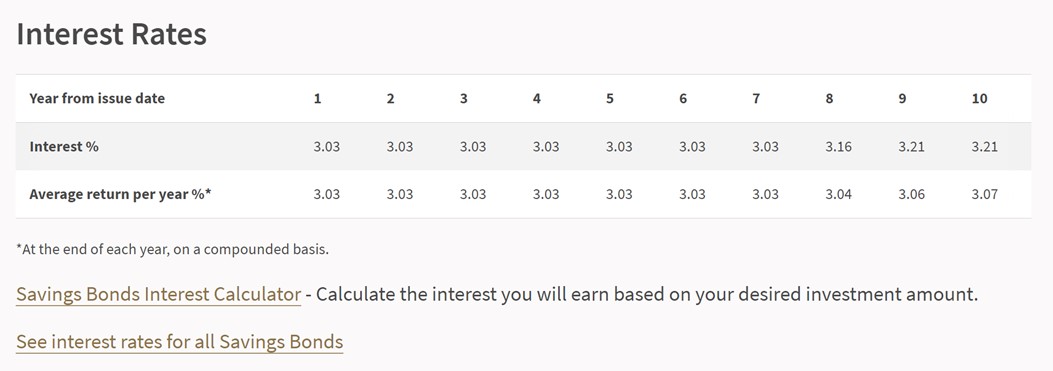

Better Buy – Singapore Savings Bonds vs T-Bills

For reference, here are the interest rates on the latest Singapore Savings Bonds.

You’re looking at 3.03% for the first 7 years, stepping up to 3.07% after 10 years.

Singapore Savings Bonds are quite a different product from T-Bills.

With the current inverted yield curve, I would say go with T-Bills or Fixed Deposit if you want to benefit from the high short term interest rates.

Go with Singapore Savings Bonds if you want the optionality to hold up to 10 years.

I myself hold my cash in a mix of T-Bills, Fixed Deposit and Singapore Savings Bonds.

So yes – there is a place for each of them in a Singapore investor’s portfolio.

It’s ultimately a trade off between yields, liquidity, and duration – and I suggest each investor put some thought into what the right balance for them is.

This article is written on 14 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!