So there were quite a few interesting developments in fixed income (interest rates) this week that I wanted to talk about.

And also share my views on how I think interest rates might play out in the short term (2 – 3 months).

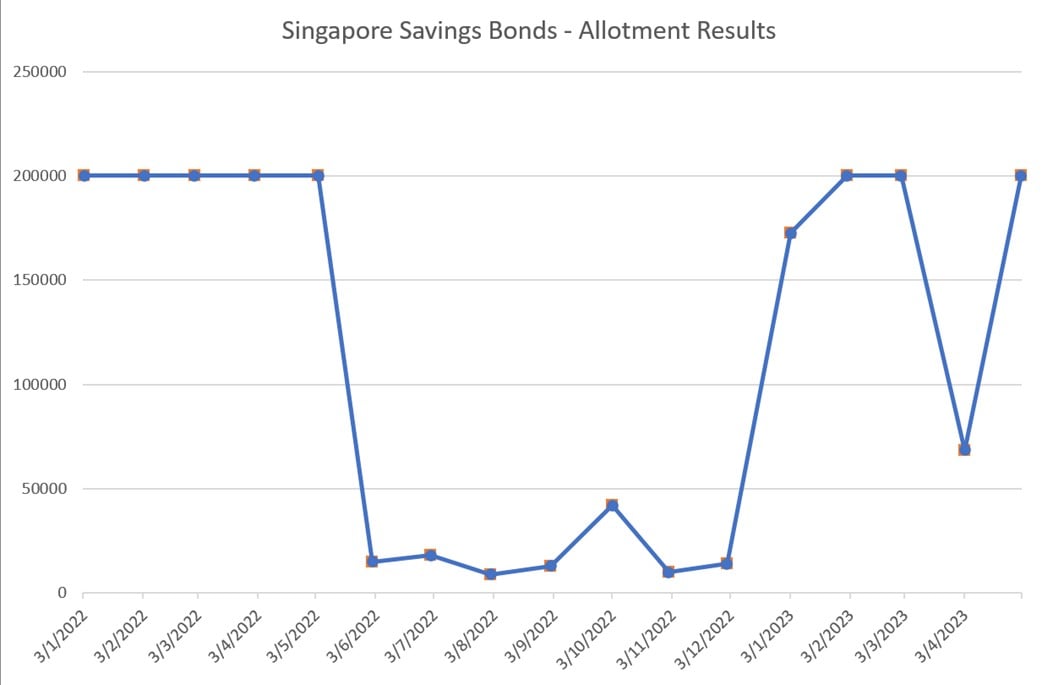

Singapore Savings Bonds Full Allotment

First off – Singapore Savings Bonds see full allotment.

Everyone who applied would have gotten what they applied for, up to the $200,000 limit.

You can see the long term chart plotted below.

Allotment fell to $68,500 last month.

Before rebounding back to the maximum $200,000 limit this month.

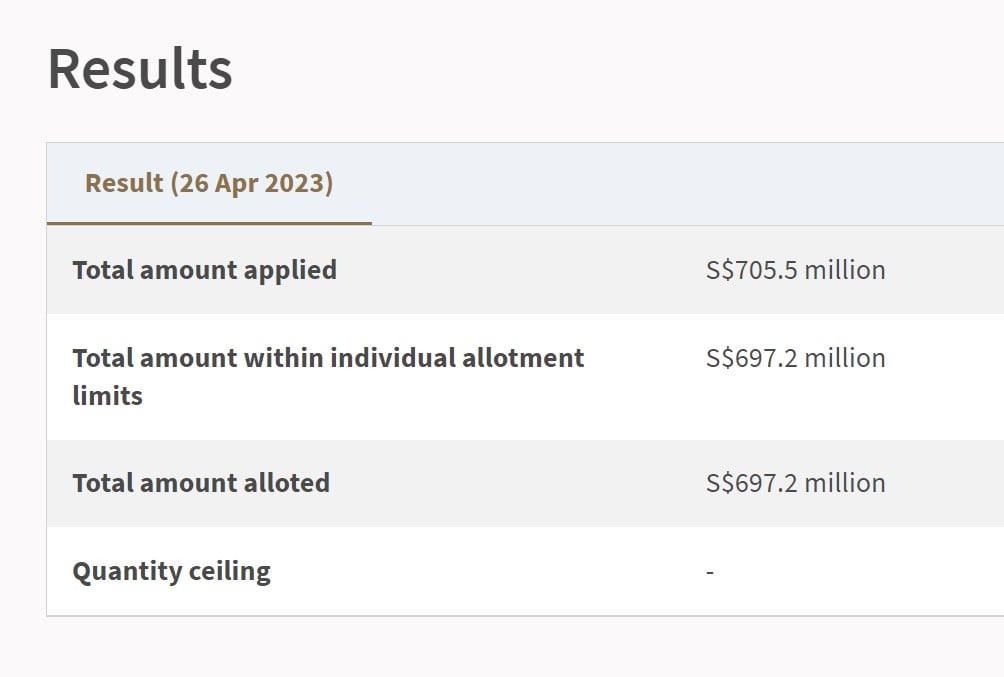

Diving deeper into the numbers – Singapore Savings Bonds received $697.2 million worth of valid applications.

Interestingly almost $8.3 million worth of applications were beyond the individual allotment limits of $200,000.

Seems like some people forgot that they were already maxxed out on Singapore Savings Bonds, or perhaps just forgot to put in the redemption request.

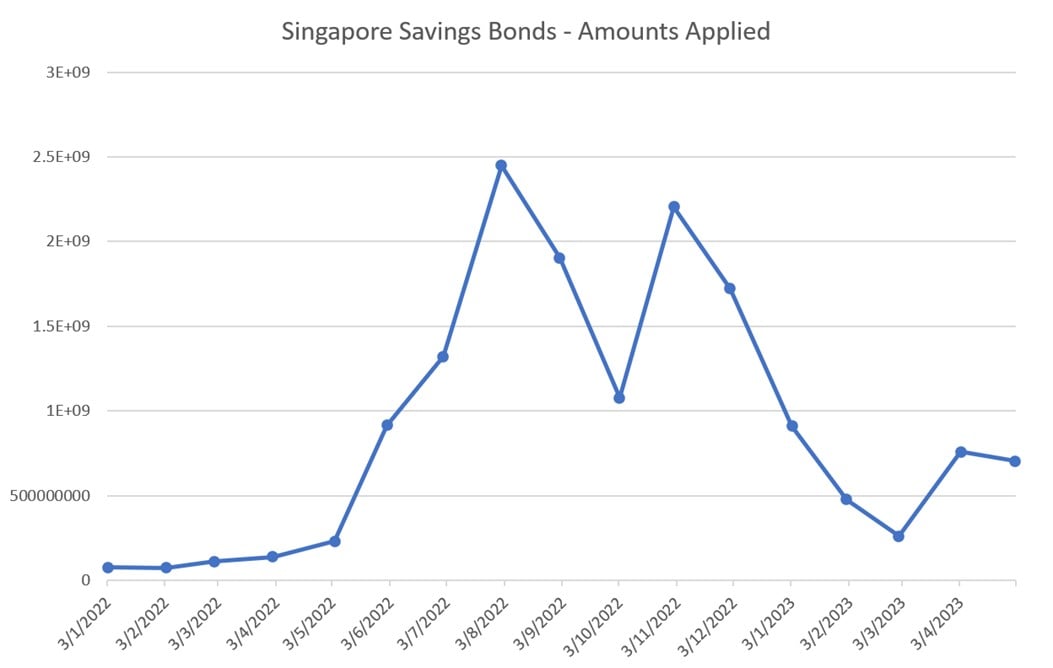

Demand for Singapore Savings Bonds only dropped slightly

Very interestingly though – the application amount of $705 million is only slightly below last month’s $758 million.

In other words – application amount only declined slightly, but that was more than enough to bring allotment amount up from $68,500 to the $200,000 limit.

This shows you how much impact a small shift in demand can have.

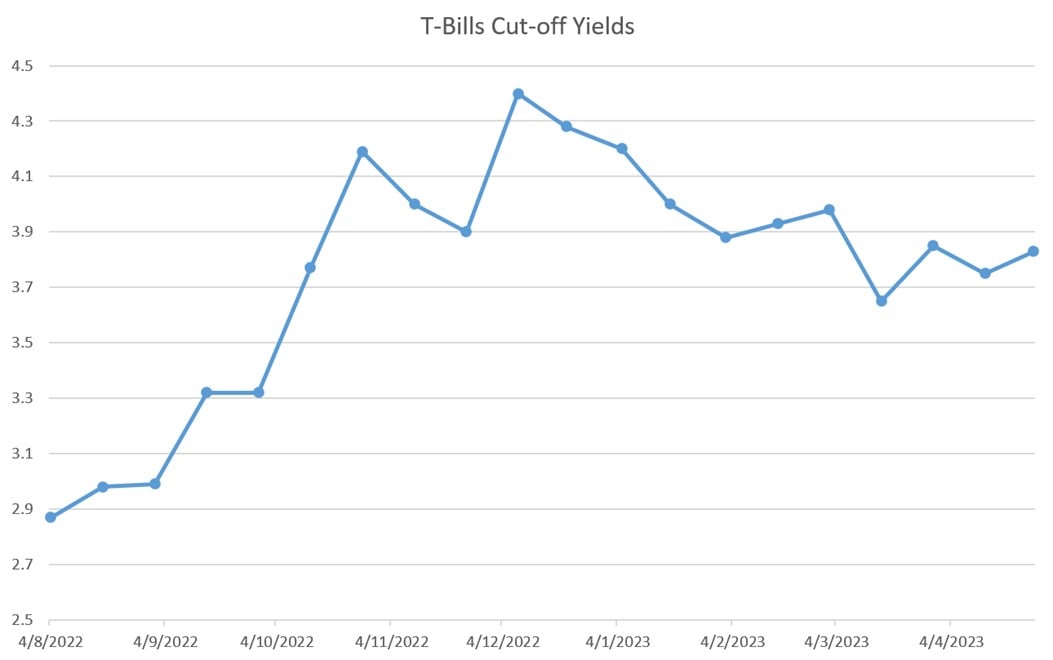

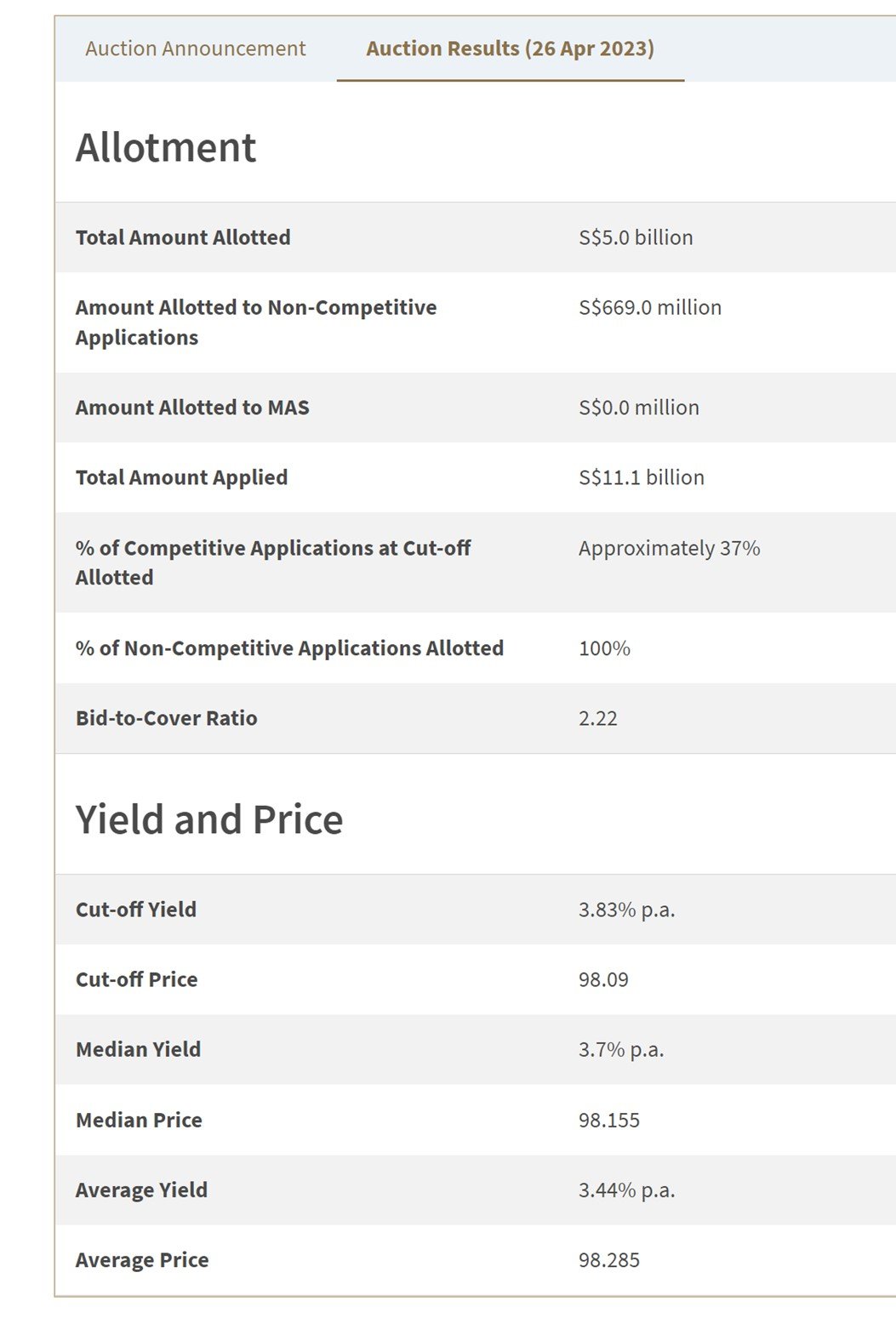

6 month T-Bills issued at 3.83% yields (26 April 2023 Auction)

We also saw auction results for the 6 month T-Bills this week.

6 month T-Bills were issued at 3.83% yields.

You can see the cut-off yields below, it’s actually a nice pickup from the March lows.

Do note however that a big part of this is due to a drop in demand from CPF-OA buyers.

The problem is that this round of T-Bills had an auction date of 26 April 2023.

Which means that CPF-OA buyers would see their CPF-OA deducted on 27 April 2023, while the T-Bills themselves were only issued on 2 May 2023.

In other words CPF-OA buyers would lose the whole month of April CPF-OA interest, while only earning T-Bills interest starting in May.

This was not that good a deal – and because of this I wrote that CPF-OA buyers may want to skip this round of T-Bills.

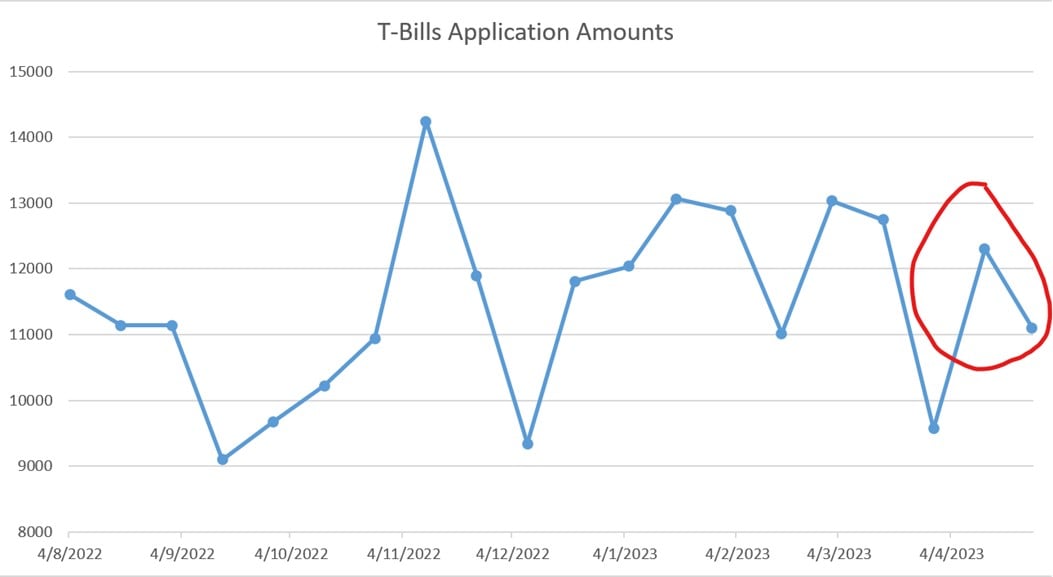

And indeed you do see application amounts dropping quite drastically from the previous auction:

So this round of T-Bills yields can be considered slightly a “freak result” in the sense that many CPF-OA buyers may have skipped it.

So the yields might not be so representative of what you will see in the next auction.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Where are Interest Rates headed in 2023?

I also wanted to talk a bit about where interest rates may be headed in the months ahead.

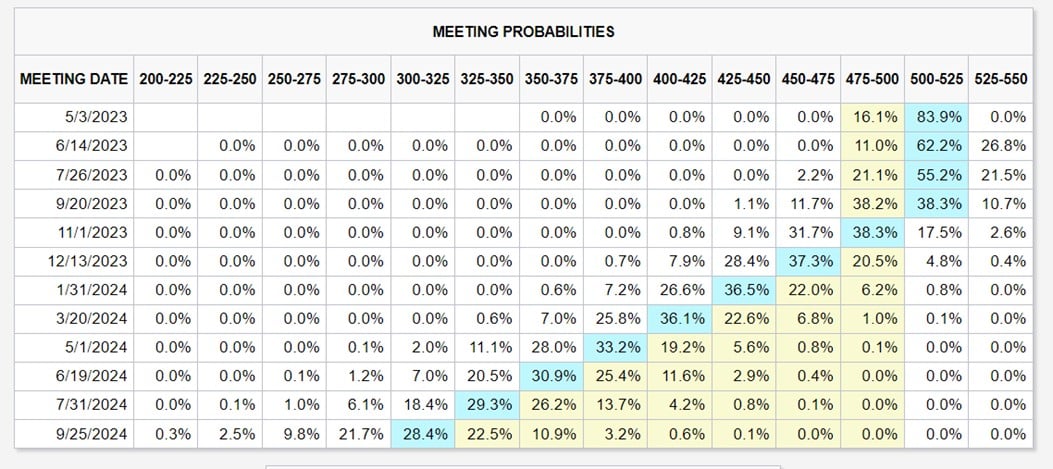

Here’s what market is pricing in.

1 more interest rate hike in May’s FOMC.

Followed by a pause in rate hikes for the next 4 months.

And then 2 interest rate cuts by end of 2023.

Personal View – I think the market is wrong on this

I’m going to put it out there that I think the market is just wrong on interest rate pricing.

For the simple reason that the economy is proving more resilient than expected.

The economy is stronger than what the interest rate market is pricing in

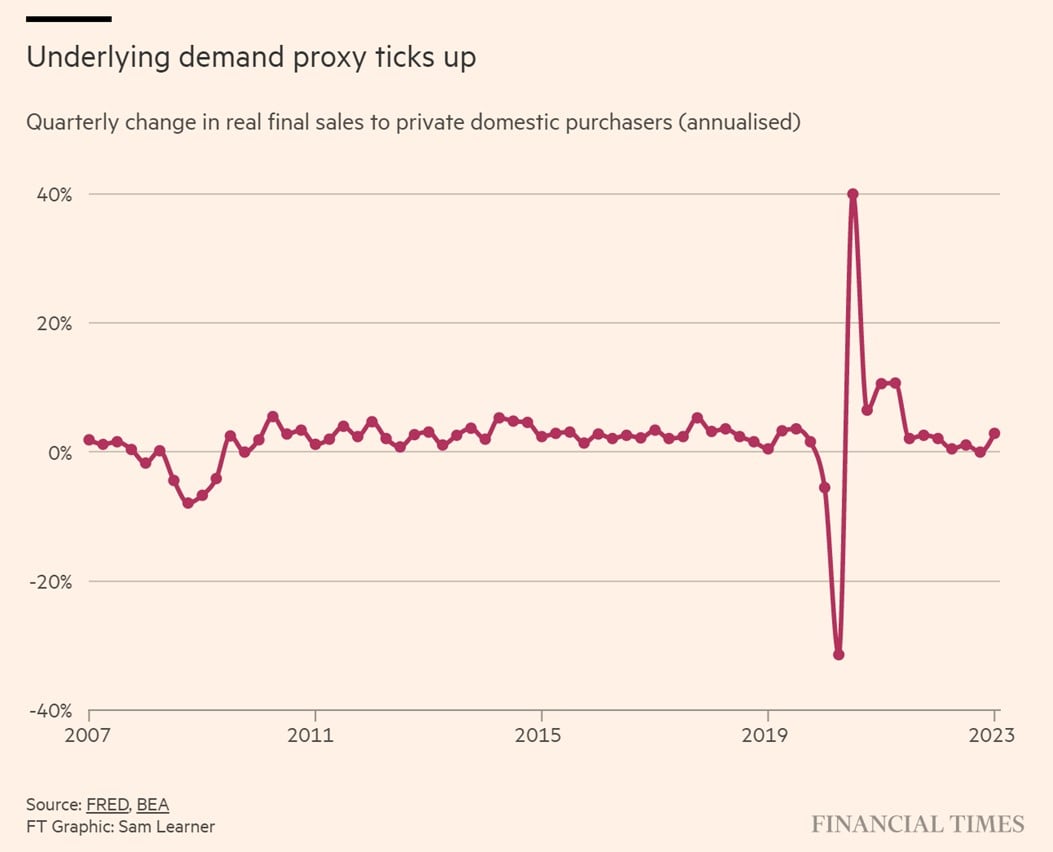

Q1 GDP numbers for the US came out this week, and yes quarterly change in real GDP has slowed from the past 2 quarters:

But look under the surface, and you see that consumer demand is the strongest it has been since Q2 2022.

Consumer is still looking very strong here, with signs of a pickup:

Look at the latest PMI data, and you see signs that the economy is actually starting to rebound instead of slowing down.

Look also at the recent round of corporate earnings.

You can see that yes some parts of the economy is slowing, but other parts remain red hot.

What does this all mean?

What has been a very difficult business cycle to read, only gets worse.

My personal takeaway, is that the economy is proving more resilient than bond / interest rate markets are pricing in.

Interest rate markets are pricing in the economy to collapse in 2023, that allows the Feds to cut interest rates by end 2023.

But economic data is throwing serious doubt on this narrative.

Economic data is showing no showing signs of an immediate recession just yet.

Yes, there is no doubt if we continue down this path a recession will come eventually.

But the markets are pricing in a recession in the next 3 – 6 months, and economic data just disagrees with that view.

There is a little bit more juice left in this cycle.

Why I think interest rates may go up in the short term (before going down later)

Personal views here.

With the latest economic data coming in, I think the 25 bps rate hike next week is a done deal.

In fact with economic data this hot, I think Powell may talk up the possibility of another rate hike for June’s FOMC.

He might want to raise market pricing for a June rate hike beyond the current 20%.

And he will likely want to reiterate that market pricing on interest rate cuts in 2023 looks very optimistic, given the economic data that is coming in.

In other words – current market pricing on interest rate cuts looks too optimistic.

More pain on interest rates is likely to come (in the short term, before it gets better).

Does this change the mid term recession outlook?

Don’t get me wrong though, the discussion above is purely on the short term.

The mid term outlook still looks the same to me.

I might even go out and say the more the Feds tighten today, the greater the slowdown / recession will be when it comes.

And the more the Feds will have to cut interest rates when the time comes.

Timing wise, I wrote previously that I see the stars aligning for a period of economic slowdown in 2H2023 – 1H2024.

Thinking remains broadly the same, and I extract the reasoning below:

“And if you ask me, I think the economic weakness will start to bite in 2H 2023.

Couple of reasons why.

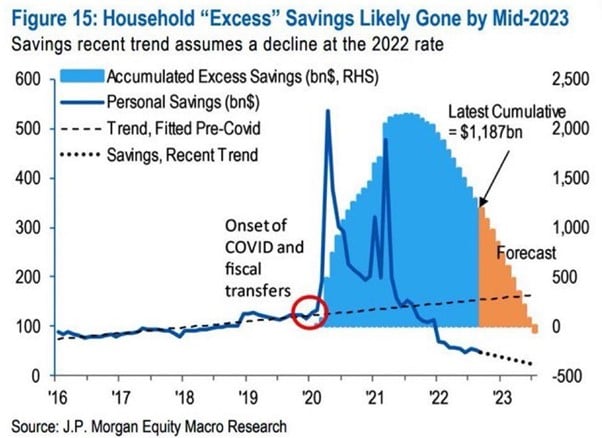

Firstly – by the second half of 2023, consumers will start to run down all the excess savings built up during COVID:

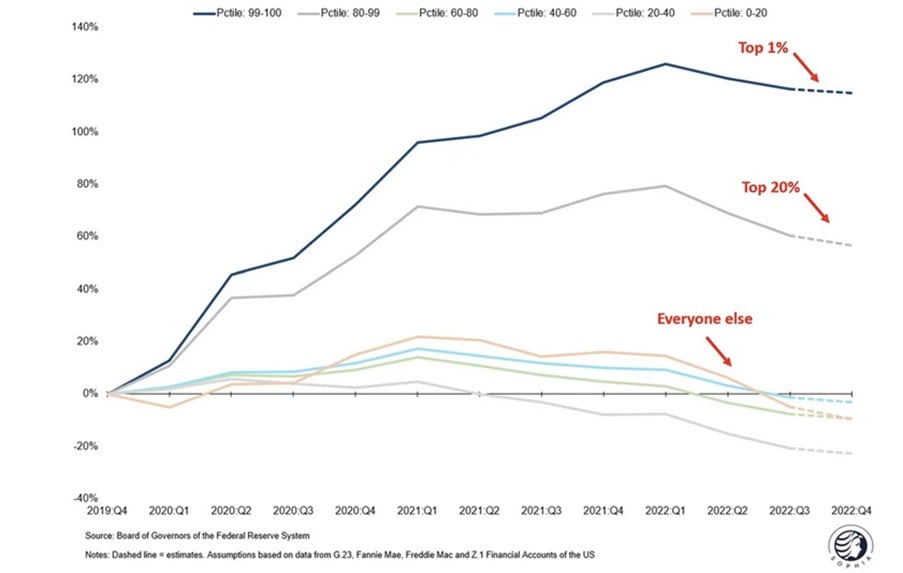

At the same time, higher inflation will start to bite for everyone outside of the top 20% of earners.

While most of the G7 central banks will be at terminal interest rates.

While COVID era stimulus programs start to roll off.

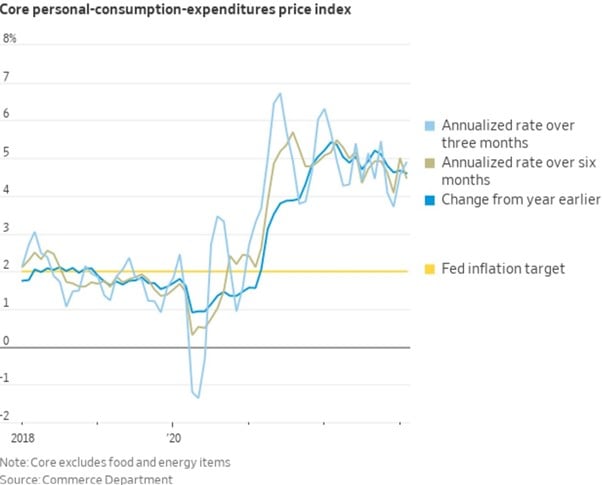

All while inflation starts to stabilise at a 4% range – which bites into consumer purchasing power.

So the stars are starting to align for a period of economic weakness in 2H 2023 – 1H 2024.

That being said – How long from then until Powell is forced to cut interest rates?

Really depends on what breaks, and Powell’s desire to fight inflation vs avoid a recession.”

Jury is still out on that one.

This article is written on 29 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

It looks like demand is going to stay strong. If inflation doesn’t slow down more significantly, the central banks are going to be forced to raise interest rates more than some people expect. What we see all around us are very busy airports, full (or nearly full) airliners and restaurants, and higher prices for a whole range of things. The expressways are busy, and rush hour jams are again the norm. I think rates are (eventually) going to go higher, probably back to the historical average, and that’s not a bad thing.

Yes inclined to agree on this. Economy is proving more resilient than expected, which may lead to further tightening (or stay high longer than expected).

Which will eventually worsen the slowdown / recession to come.

Either way, more rates pain lies ahead (before it gets better).

The armchair economist in me says that we are due for another round of tightening of the SGD because MAS refused to do it the last round and inflation has slowed but still not stopped….

It’s funny because there was indeed a slowdown towards the end of last year. But in 2023 things seem to have picked up again.

So yeah… inclined to agree that in the immediate term more tightening is in store.