In a remarkable feat amidst the challenging landscape of the aviation industry, Singapore Airlines (SIA) has achieved unprecedented success, catapulting its financial performance to unprecedented heights in the fiscal year 2023 with the highest net profit in its 76-year history!

Here, we delve into the factors behind SIA’s remarkable achievement, exploring the key drivers that propelled the airline to this enviable position and, more importantly, finding out what the future holds for the company.

Overall performance

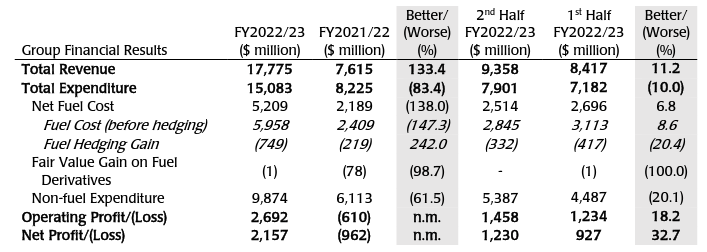

Singapore Airlines’ revenue reached an unprecedented high of $17.8 billion, representing a significant increase of $10.2 billion or 133.4%. This remarkable growth was primarily fueled by a substantial surge in passenger flown revenue, which rose by $10.6 billion or 376.3% to reach $13.4 billion, outpacing the expansion of capacity.

Despite a decline of $735 million or 16.9% in cargo flown revenue, the group still achieved its second-highest annual figure in this category.

Regarding expenditures, Singapore Airlines successfully employed fuel hedging strategies, resulting in savings of $530 million. Additionally, the growth rate of non-fuel expenditures was comparatively slower, enabling expenditures to increase at a more moderate pace than revenue.

As a result, the group’s operating profit reached a record-breaking $2,692 million, marking a significant turnaround from the $610 million loss incurred in the previous fiscal year (FY2021/22).

Continued Strong Performance

The ongoing improvement in performance by Singapore Airlines is evident not only on a yearly basis but also on a half-year basis, demonstrating consistent progress and dispelling any concerns about a mere rebound effect from previous losses.

In the latest six-month period, Singapore Airlines achieved remarkable growth, with revenues increasing by $941 million or 11.2% compared to the previous six months, reaching a record half-year revenue of $9,358 million for the SIA Group.

Furthermore, expenditure growth remained below revenue growth, with an increase of $719 million or 10.0% half-on-half, resulting in total expenditures of $7,901 million.

As a result, the group achieved a significant second-half net profit of $1,230 million, representing a growth of $303 million or 32.7% compared to the first half. This impressive increase not only indicates sustained growth since the previous half but also reinforces the company’s record-breaking earnings.

Outpacing Other Airlines in Recovery

While the significant revenue growth can be attributed to the gradual relaxation of travel and pandemic-related restrictions in the region, leading to a resurgence in air passenger traffic, the reason why Singapore Airlines was able to do so well was its faster recovery compared to other airlines in the Asia-Pacific region.

What sets Singapore Airlines apart from other Asia-Pacific airlines is its ability to capitalize on the pent-up demand prevalent across the region.

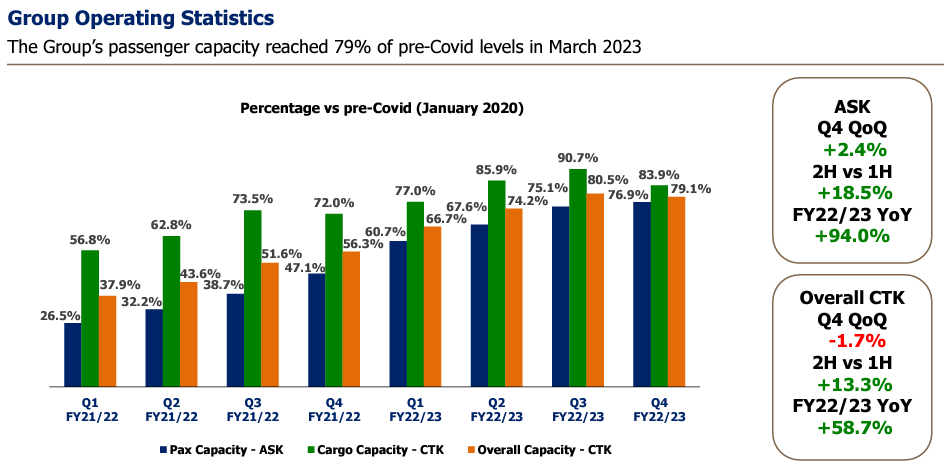

In March 2023, the group’s passenger capacity reached 79% of pre-Covid levels, surpassing the 58% level achieved by international scheduled services of Asia-Pacific airlines, which encompasses data from 40 airlines in the region, including SIA and Scoot.

The combined efforts of Singapore Airlines and Scoot resulted in carrying 26.5 million passengers, a six-fold increase compared to the previous year.

Moreover, the passenger load factor (PLF), which represents the proportion of occupied seats by paying passengers on flights or over a specific period, experienced a jump of 55.3 percentage points, reaching a record high of 85.4% for the group.

These figures highlight Singapore Airlines’ ability to leverage the resurgence in demand and optimize passenger capacity, leading to higher seat occupancy rates. This outstanding performance not only underscores the airline’s success in recovering faster than its regional counterparts but also represents historical milestones in terms of passenger load factors for the group.

Moderation in Cargo Performance

It is important to note though, that not all aspects of Singapore Airlines’ operations experienced growth.

The cargo segment’s performance was affected by the subsiding supply chain disruptions caused by the Covid-19 pandemic and macroeconomic factors that dampened consumer demand. As a result, there was a decline in the demand for air freight, leading to a moderation in the cargo segment’s year-on-year performance.

The increased availability of belly hold capacity, resulting from the gradual resumption of passenger flights, contributed to a decrease in cargo yields compared to the previous year.

While it is noteworthy that cargo revenue remained 83% higher than the pre-Covid level recorded in the calendar year 2019, in absolute numbers, there was a significant decline of $594 million or 28.3% in cargo flown revenue due to reduced loads (-5.2%) and lower yields (-24.3%).

Looking ahead, this slowdown in the cargo segment is expected to persist, and substantial growth should not be anticipated in this area. The combination of factors such as supply chain disruptions, macroeconomic headwinds, and the restoration of passenger flights contributing to increased belly hold capacity will likely continue to impact the cargo business.

Robust balance sheet

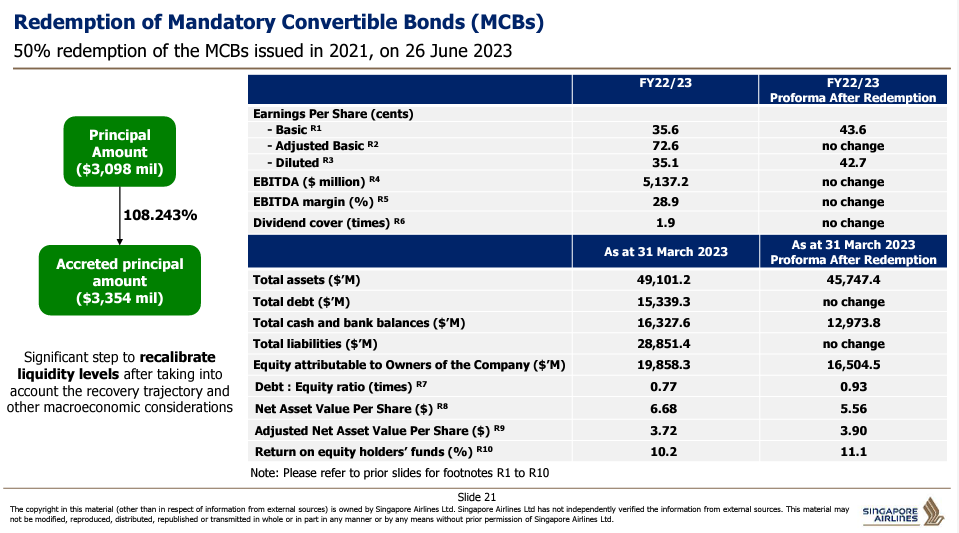

From a financial stability standpoint, Singapore Airlines’ balance sheet remains strong. As of March 31st, 2023, the company had a cash and cash equivalent balance of $16 billion, representing a $3 billion increase from the previous year, even after the redemption of mandatory convertible bonds costing $3.8 billion.

With this impressive cash position, Singapore Airlines has the flexibility to redeem the remaining mandatory convertible bonds, especially now that the improved results have likely given management more confidence in the company’s financial position.

In fact, on May 10th, 2023, the company announced its intention to redeem 50% of the tranche of Mandatory Convertible Bonds issued in June 2021, with the remaining bonds possibly being redeemed in the future.

This redemption will be carried out on a pro-rata basis and will provide eligible bondholders with a accreted principal amount payable of approximately $3.4 billion, which will be paid on June 26th, 2023.

SIA Final Dividend for FY22/23

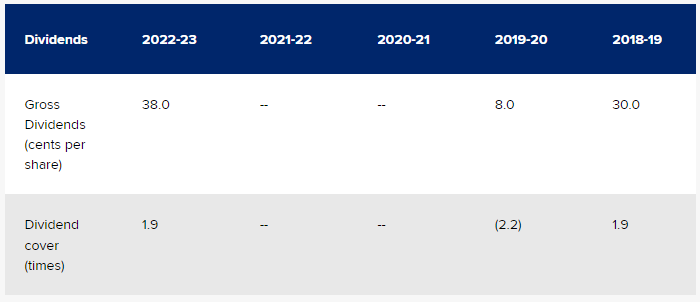

In terms of dividends, following a successful year, Singapore Airlines’ management has announced a final dividend of 28 cents per share. When combined with the interim dividend of 10 cents per share paid in December 2022, the total dividend for FY2022/23 amounts to 38 cents per share, bringing it to a level similar to 2018.

It is worth noting that this comparison is made pre-dilution; therefore, the 38 cents per share dividend announcement represents a notable improvement.

Considering the last closing price of $5.92, Singapore Airlines then offers a dividend yield of 6.4%.

Looking Ahead: Short-Term Growth and Long-Term Challenges

Focusing on the road ahead, in the short term, Singapore Airlines (SIA) is expected to continue its growth trajectory as it fills up its remaining capacity and resumes flights to various destinations, including China.

Forward sales remain healthy across all cabin classes, driven by strong bookings to China, Japan, and South Korea. The company projects its capacity to reach an average of around 83% of pre-Covid levels in the first half of FY2023/24, with the current capacity at 79%. These factors paint a positive picture for SIA, at least for the initial half of FY2023/24.

However, looking ahead in the long term, the company may face more challenges. Geopolitical and macroeconomic uncertainties and high-cost inflation could pose difficulties for the airline industry in the coming months. Although fuel prices have moderated recently, they remain at elevated levels.

Furthermore, as SIA nears full capacity and pent-up travel demand subsides, competition from other regional airlines may normalize ticket prices, potentially leading to lower passenger yields and revenue normalization or decline.

Similar challenges can be expected in the cargo segment, where inflation and weak economic conditions may impact consumer demand and trade. The increased belly hold capacity, coupled with softer demand, is likely to exert downward pressure on cargo yields, especially on key trade lanes.

Can SIA keep up the performance?

In conclusion, Singapore Airlines performed well for the full year of FY2022/23, leveraging its adaptable management and faster recovery than regional airlines.

However, going forward, the road may become more challenging.

While SIA may see some growth in the near term, the entrance of regional airlines and the subsiding of pent-up demand, along with worsening macro conditions, raise questions about SIA’s sustained success.