After last week’s article on Keppel Infrastructure Trust, some of you have asked for an update on the Singapore Banks.

DBS, UOB and OCBC are down about 10 – 15% from their highs.

At this price, they pay about 5% dividend yield, which is pretty juicy.

And yet conventional wisdom is that banks are a bad buy here because of (1) peak interest rates means falling net interest margins going forward and (2) we’re going into a recession so loan defaults are going up.

As always, the truth is seldom so straightforward.

So let’s spend some time discussing whether the banks are a good buy here.

DBS, UOB and OCBC share prices are down from their peak

From it’s high of $36, DBS is down 15% from the top.

You can also see how share price hasn’t really gone anywhere since Jan 2022, so apart from the dividend this has been dead money for 18 months now.

It’s why I wrote a piece in early 2022 suggesting whether to sell banks back then.

Likewise UOB is down 12% from the top, and also hasn’t gone anywhere for 18 months.

Funnily enough OCBC’s relative performance is the best, down only 8% from the top.

But this is partly because OCBC didn’t go up so much in the 2020 – 2021 period (because of worries over their China exposure).

Dividends for Singapore Banks are very strong at this price – 5% yields

At current prices, dividend is very attractive though.

You’re looking at about 5% dividend yield across the board for DBS, UOB and OCBC.

In fact if you count the special dividend, you’re even looking at a 6.5% trailing dividend yield for DBS.

|

Bank |

Dividend yield (trailing 12 months) |

|

DBS |

6.5% (including special dividend, 5.5% excluding special dividend) |

|

UOB |

4.8% |

|

OCBC |

5.5% |

Why conventional wisdom is that it is time to sell banks?

As I’m sure you know by now.

Conventional wisdom (not necessarily my view though) would tell you that this is not the time to buy banks.

Rather, this is the time to be selling banks.

Dr Wealth and Beansprout both wrote on this.

That banks are not a good buy for 2 simple reasons:

- Peak interest rates means falling net interest margins going forward

- Recession means loan defaults will go up

Let’s discuss each of them.

And I will share my views on why there is more than meets the eye here.

Peak interest rates means falling net interest margins going forward

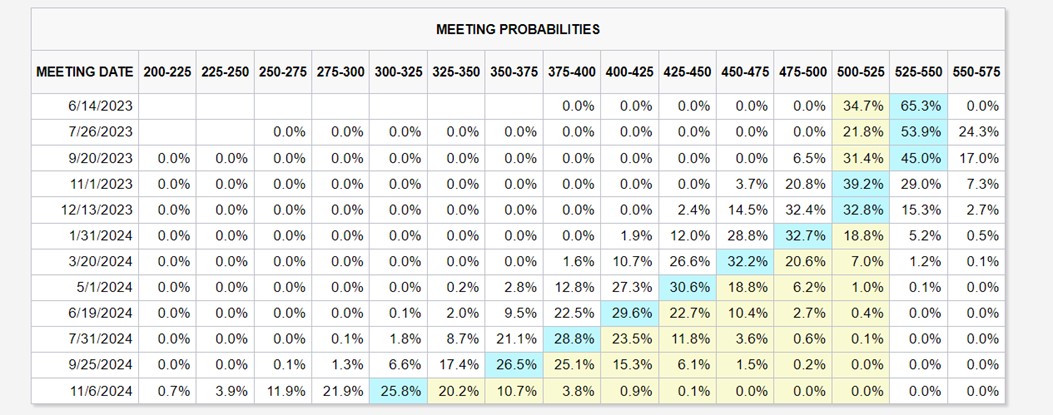

This is the latest market pricing on interest rates.

50% chance of 1 more rate hike, and a slim chance of 2 more rate hikes.

With interest rate cuts in late 2023 or early 2024.

We are at close to peak interest rates here

But let’s not miss the forest for the trees here.

Yes we can debate over exactly how many more rate hikes we will see.

But the fact of the matter is that this is no longer June 2022.

We have hiked 5.0% in 12 months, in one of the fastest rate hike cycles in over 30 years.

Where we are today – we are at the tail end of this rate hike cycle.

We are at close to peak interest rates here.

The next big move in interest rates, is unlikely to be to the upside, but to the downside.

Interest rates going down is not good for banks

Banks make money by lending money right – so if interest rates go down, banks make less profit?

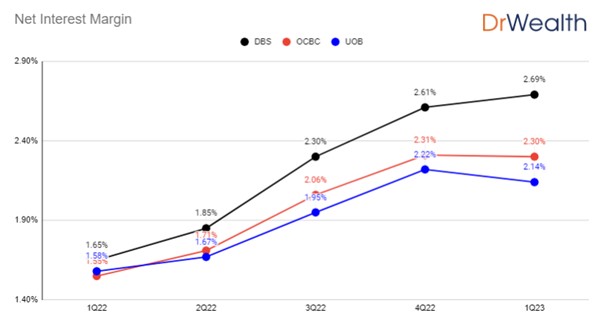

Here’s a chart from DrWealth, suggesting that bank net interest margins may have peaked (or are in the process of peaking).

You can see how while DBS’s net interest margin is still going up.

OCBC’s net interest margin is flat, while UOB’s has actually gone down.

Suggesting that perhaps conventional wisdom is right – bank net interest margin may be peaking here.

What people are missing? – Funding Costs for banks are coming down

Remember how I said things are seldom so straightforward?

I think what people may be missing here, is that while headline interest rates are peaking.

Funding costs for the 3 local banks are also peaking.

Funding costs for the banks are coming down

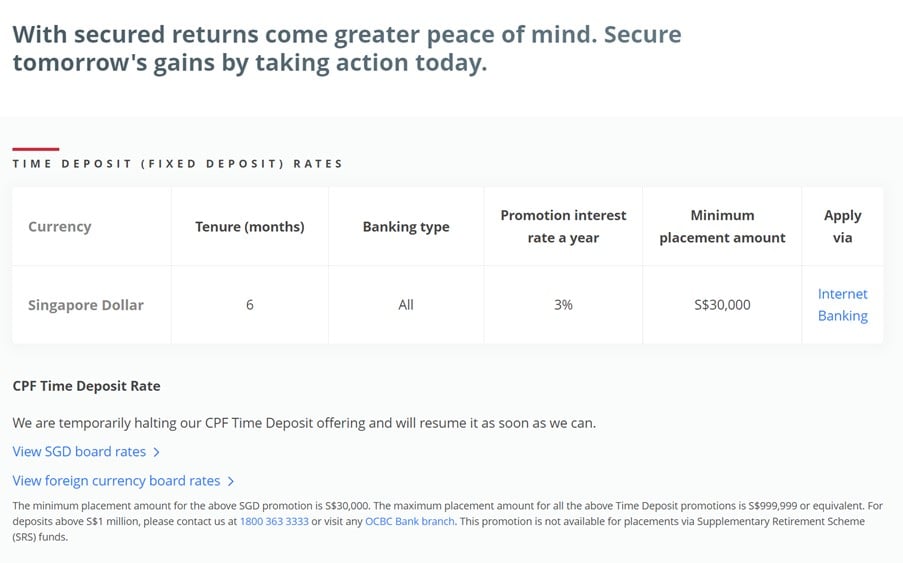

You just need to take a look at OCBC for an example.

Just a few months ago I was dumping whatever spare cash I could get my hands on into OCBC’s Fixed Deposit at 4.08% for their Chinese New Year promo.

And today – what interest rates is OCBC offering?

3.0%.

Heck, even their CPF Fixed Deposit option has been “temporarily halted”.

So OCBC went from paying 4.08% on their fixed deposits, to paying 3.0%.

All in the span of 4 months.

That’s a massive drop in the funding cost for the local banks.

So yes, interest rates may be peaking.

But banks are getting much cheaper funding too.

Is it big enough to offset the impact from peak interest rates?

I mean I don’t know the answer, but I’m willing to bet the answer is a lot more nuanced than what conventional wisdom is suggesting.

We’re going into a recession so loan defaults are going up

Now let me put it out there that I don’t deny we are likely to head into a recession the next 12 months.

Germany is already in technical recession.

US is likely to follow in the second half of 2023 or early 2024.

And Singapore may find itself in a technical recession as early as 2023.

In a recession, loan defaults go up

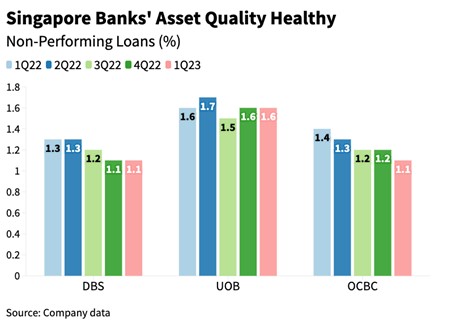

So conventional wisdom is that in a recession – Loan defaults are going to go up.

With bank non-performing loans at a record low, this can only go up in a recession, which is bad for banks.

Right?

Source: Beansprout

What people are missing? – The depth of the recession is not clear

As always, there is more than meets the eye.

While I don’t deny a recession is coming.

I think the million dollar question now is how deep the recession is going to be.

Remember that the definition of a recession is negative real growth.

As in inflation adjusted growth.

When your core inflation is raging at 5%, even GDP growth of 4% is going to trigger a technical recession.

So yes, we are going into a recession.

But a recession with the economy growing at 4% nominal, vs a recession with the economy growing at -3% nominal, are very very different things.

As of today, it’s not so clear which one we’ll get – much will depend on policy makers actions over the next 12 months.

What about Government stimulus? Can Singapore weather the storm?

To further complicate the matters, we’ve seen how governments were quick to roll out stimulus in 2020 when COVID hit.

If we get a bad recession, how long before you think governments are going to start handing out cash to people?

Don’t forget 2024 is an election year for both the US and Singapore.

Are we going to see fiscal support for companies and individuals in the next recession?

Are we going to see pauses on mortgage payments?

Again, I don’t know the answers to this question, but it would be naïve to not as least consider their possibility.

Loan defaults soaring in a recession is not a foregone conclusion, as 2020 has shown.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Are valuations for the Singapore banks attractive?

With that in mind – are the Singapore Banks of DBS, UOB and OCBC a good buy?

Valuations are below, and you’re generally buying in at a small premium to book, while getting a nice 5% dividend.

|

Bank |

Price / Book |

Dividend yield (trailing 12 months) |

|

DBS |

1.4x |

6.5% (including special dividend, 5.5% excluding special dividend) |

|

UOB |

1.1x |

4.8% |

|

OCBC |

1.0x |

5.5% |

I’ve set out the long term price / book chart for DBS below.

At 1.4x, it’s slightly higher than the long term average of 1.3x

Would I buy DBS, UOB or OCBC now?

The more I think about it, the more I think investing this decade is going to be quite different from the previous.

It’s no longer about buying a broad index and holding for 10 years.

This decade, a much more active approach to investing may be required.

And whether a stock is a good buy or not, may depend very much on the investor.

Let’s discuss this both from the perspective of a short term (2 – 3 year) holding, and as a long term (5 – 10 year) holding

Short Term (2 – 3 year holding) – What is the upside for the Singapore banks here?

What’s the upside for say DBS here?

At $30 and 1.4x price to book.

Let’s say we get a mild recession, and price goes back up to 1.6x book ($35).

That’s a 16% upside.

Throw in the dividend and you’re looking at a 20% – 30% gain.

What if you get a hard landing?

What if you get a hard landing though?

Book value is $22, so in a hard landing its not impossible to see it going back there, with the dividend getting slashed.

That’s about a 30% downside if you’re wrong.

Is the risk-reward attractive?

30% gain if we get a soft landing, vs 30% loss if we get a hard landing.

If I were a gambling horse (and I am), would I take those odds?

Not so sure, like I said I can see both a soft landing and hard landing playing out, depending on how quick Powell is to cut interest rates in the months ahead.

Are there alternative investments that are more attractive now?

Let’s say I don’t buy the banks.

Where do I put my money instead?

If I wanted to flip money for a short term gain, I think there are 2 key places I see as attractive right now.

REITs – as a Fixed Income Proxy?

The first would be bonds (fixed income).

Or fixed income proxies like REITs.

Given that we are at close to peak interest rates here, you can start thinking about playing the next phase of interest rate cuts.

As shared with Patreons, I myself started buying high quality REITs with solid underlying cashflow that I think are attractively valued the past week.

A lot of the names I’m looking at are at close to cycle lows and 7%+ valuations, which is attractive enough for me (full sharing of the REITs and thought process on Patreon).

Embrace the momentum – AI or FAANG

Or you can embrace momentum, and buy the (a) bubbly AI stocks like NVIDIA or AMD, or (b) recession plays like FAANG.

Yes of course this area is in a bubble, but in a bubble you can make money both on the way up and on the way down.

Just be careful with your risk management, because I do think this will end in tears.

Don’t jump into the bubble unless you have a decent risk appetite.

Sadly I sold out my NVIDIA position a bit too early, but my AMD position which is more than double my NVIDIA position has been performing very well, as have my FAANG positions.

What if you are a long term (5 – 10 year investor)?

Remember how I said the question of whether a stock is a good buy is going to be far more nuanced this decade?

If you’re a long term investor and you just want to buy and hold a stock for the next 10 years, I think the answer could be very different.

If I had no exposure to the banks today, and I were a long term investor, I might just buy a small position at today’s prices.

Who knows, maybe Powell does pull off a soft landing, and we only get a mild recession.

What about me? Am I buying DBS, UOB or OCBC today?

Full disclosure that I hold positions in DBS and UOB today.

I did sell about half of my bank positions this cycle though (to rotate the cash elsewhere).

Will I buy or sell more today?

Frankly I don’t think so.

I would buy REITs (or Momentum plays) instead for now

As shared above, I actually like the REITs more at today’s prices.

Given that we’re close to peak interest rates here, I’m buying high quality REITs with solid underlying cash flow.

A lot of the names I’m looking at are at close to cycle lows and 7%+ valuations, which is attractive enough for me (full sharing of the REITs and thought process on Patreon).

Of course, a hard landing may come, so I’m not blowing all my cash just yet, and saving enough in case things get really bad.

And as a long term investor, I already have exposure to DBS and UOB.

To the point where I don’t see a big need to add to my positions, unless prices become more attractive.

DBS are closer to book value, or UOB at a discount to book – sure I will add.

Today’s prices, I will just hold my existing bank positions and buy the REITs (or momentum plays if I’m feeling adventurous) instead.

But… we are very late cycle, be very flexible here

But like I keep saying, we are very late cycle, and things move very fast these days.

As an investor, you want to be flexible and nimble.

So this is what I think as of today, but I may easily change my mind in a month or two and load up on the banks. And Patreons will get access to my latest up to date thinking, and if / when I decide to buy or sell the Singapore banks.

But whatever the case, I don’t doubt that we’ll see lots of great investment opportunities over the next year or two as this hard/soft landing plays out.

2024 is a US election year, so you’re going to have to deal with bipartisan politics at the same time the US economy will be going into a recession.

Buckle up!

This article was written on 1 June 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 500 worth of fractional shares (expires 30 June)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $100 SGD

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Definitely food for thought, especially that bit factoring the election year. And yeah, buckle up coz 2023-2024 is gonna be a helluva wild ride lol

I do think it’s gonna be interesting to say the least. Whatever your views and positioning, I would as least keep some cash for how the next 18 months is going to play out. 😉

Definitely. I was sitting on plenty of cash when I saw the opportunity to buy into DBS towards the end of 2019 (when trumpity was US prez & creating a lot of havoc in the markets with his economic “policies”) & then a second tranche of DBS in early 2020 (Covid-19 became a pandemic for real & people were just dumping all equities in a blind panic). Held onto it until today & still one of my best buys.

Nicely played!

I too was heavy cash in late 2019 as well, that turned out incredibly useful in 2020. Like you, I picked up large DBS positions in 2020 that delivered very nice returns.

Lol, in finance, you’re only as good as your last trade.

I put in career defining trades in 2009 and 2020, but I would slap myself for missing this unloved bull rally that clearly started 236 days ago, mumbling recession to myself as NFP clocks over 300K a month.

Haha fair point.

I’m up about 20% year to date in this unloved bully rally. Could I be up more had I gone longer into NVDA/FAANG late 2022? Absolutely – so definitely a learning point.

Like you said tho, you’re only as good as your last trade.

So where we are today in the cycle – does one go even heavier into NVDA/FAANG to ride the last wave before the recession? And what is the right position sizing for that trade?

Hi FH, can you do an analysis on ADR/SDR?

Dear FH

Nice article

There are a few points that I would like to make

1- The rate cycle is peaking but the market is actually positioned ahead anticipating a MILD recession only that has been priced in as far as SG banks are concerned

2- On the contrary, the REITS here have priced in a LONGER and HIGHER (relatively) interest rate scenario

This, to me , is an opportunity as a long term investor and I am inclined to buy the banks steadily as I have been doing over the past 12/18 months

The fall in the NIM will be offset by lower NPA as well as higher wealth management income. Soaring markets almost invariably being in more in terms of non-interest income. Additionally, the lower rates would mean higher loan volumes that will once again offset the NIM fall

Overall two steps forward despite one step backward

This, will also help REITS as their finance costs fall with more activity

My allocation in SG is 2:1:1

respectively for the SG banks: SG REITS: Other SG stocks

This , in my opinion, will be a naturally hedged portfolio allocation for the current situation

I have started paring my US tech last week and will do so if tech goes higher as valuations to me, despite all the AI frenzy, are very stretched !

That money will rotate into the Oil, healthcare and consumer staples sector – this will recession proof my portfolio at least partially.

Regards

Garudadri

Hi Garudadri,

Interesting comment, but it seems that our views on how to position differ. Couple of points from me:

1. Another way to view it is that the market is pricing in a higher for longer interest rates, that eventually triggers a recession. Curious to hear why you are overweighting the banks vs REITs at this point in the cycle. If anything I would overweight REITs because of peak interest rates and the right REITs can serve as a fixed income proxy due to stability of underlying cash flow.

2. I was actually thinking of taking profit in my oil positions. Given that we are going into an economic slowdown, I don’t really want to overweight commodities at this point in the cycle. Granted I don’t know your oil allocations and perhaps you are underweight at this point in time, but curious to hear why you think oil would act as a recession hedge.

In any case, great comment as always.

Dear FH

The return in equity, cost to income ratio as well as the P/BV for all out three banks are quite good and they will withstand well as I anticipate only a mild recession

The fed will panic easily especially with 2024 presidential elections as well

This is the reason I am optimistic on banks and gradually adding very slowly. The current share prices have factored in this anticipated mild recession BUT NOT a prolonged and/or severe one. I am inclined to think it will be a mild one. Hence I am not selling banks and actually adding on down days

As regards REITS, I started adding last October at the trough and again recently. I am a bit fed up with their constant expansion fuelled private and preferential placements that dilute holdings and forces us to part with cash. Despite this, I bought Keppel and Lendlease recently and will add the Fraser’s, CICT etc but they are still not at the right price

Once again, I am adding XLE as the long term story for oil, Imho, is still intact. Both CVX and XOM , the major components of XLE, are great long term holdings and I nibble very small number of units each time to build up my oil holdings. I am a very long term holder of BP and SHEL through thick and thin! Dividends will go higher once again as all oil majors have wisened after the lessons learnt and will be very stingy with capex

Structurally under supplied market!

Regards

Garudadri

Thanks Garudadri – I understand where you are coming from. Appreicate the sharing!