I received this question from a Patreon recently:

Hello FH, any recommendations regarding a diversified dividend portfolio to hold and grow over time to generate cash flow for retirement. What to watch out for and any recos on best stocks (RIO, BHP for eg?)

I am OK to see a -20% in the portfolio, yield wise it will depend on the time one holds the portfolio, contributions and div growth rate, but perhaps we can combine stocks and REITs

And simulate cash flow in % of total investment

As you can imagine – this led me down a whole rabbit hole of portfolio building and tweaking.

And after all that playing around, I wanted to share my thoughts with you guys.

How I will invest $1 million in a dividend yielding portfolio in 2023, as a Singapore investor.

For obvious reasons – please note that nothing in this article should be construed as financial advice. I have tailored the portfolios here to my own risk appetite, and not any other investor. If you are in doubt as to the action you should take, please consult your financial advisor.

How I would invest $1 million in a dividend portfolio for myself in 2023 (as a Singapore investor)

Let me cut to the chase.

I came up with 2 different portfolio extremes.

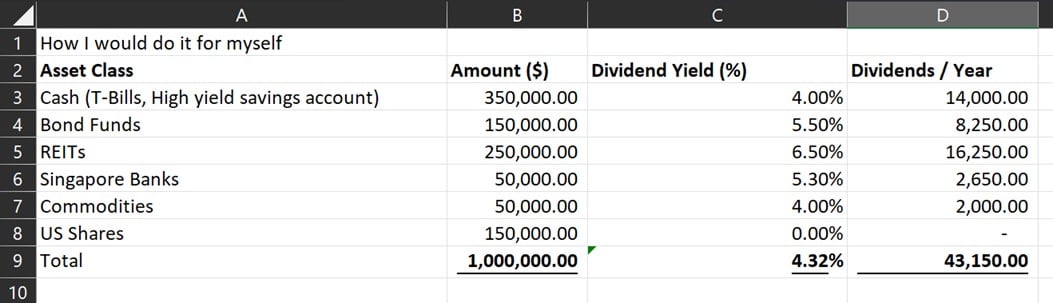

The first is how I would do it for my own portfolio:

- Cash – $350,000.00

- Mix of T-Bills and high yield savings accounts like UOB One

- Bond Funds – $150,000.00

- Either a managed solution like Syfe Income+ or DIY via Endowus Fund Smart (eg. PIMCO GIS Bond Fund)

- REITs – $250,000.00

- Equal weight:

- CapitaLand Integrated Commercial Trust

- Ascendas REIT

- Lendlease REIT

- Keppel REIT

- Keppel Infrastructure Trust

- Equal weight:

- Singapore Banks – $50,000.00

- Equal weight:

- UOB

- DBS

- Commodities – $50,000.00

- Equal weight:

- Shell

- BP

- US Shares – $150,000.00

- Overweight AI/FAANG as a short term momentum play

But FH… this portfolio only pays a 4.3% dividend yield on $1 million

I know what you’re going to say.

FH… this dividend portfolio only pays a 4.3% dividend yield.

On $1 million that’s only about $3,500 dividend income a month.

If I were happy with a 4% dividend yield I would just dump $1 million in T-Bills and get that “dividend” risk free.

Okay fair enough.

The portfolio above is what I myself would run, but I sacrificed some dividends for capital gains, and I upped the cash allocation for optionality.

Gun to my head if you forced me to buy a dividend portfolio today.

This is what I might run instead.

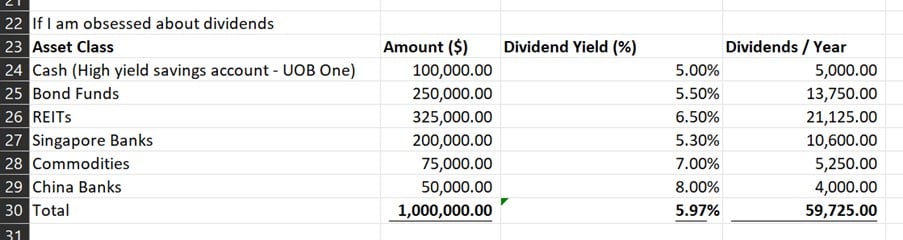

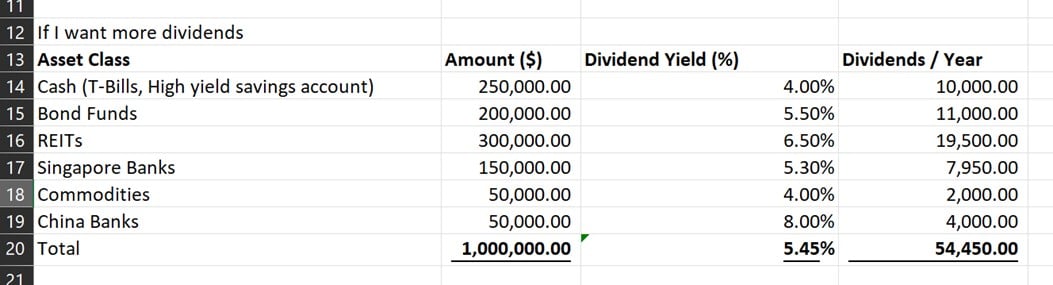

How I would invest $1 million if I only care about dividends – 6% dividend yield

- Cash – $100,000.00

- High yield savings accounts like UOB One

- Bond Funds – $250,000.00

- Either a managed solution like Syfe Income+ or DIY via Endowus Fund Smart (eg. PIMCO GIS Bond Fund)

- REITs – $325,000.00

- Equal weight:

- CapitaLand Integrated Commercial Trust

- Ascendas REIT

- Lendlease REIT

- Keppel REIT

- Keppel Infrastructure Trust

- Note that if you are comfortable with more risk you can get a higher yield by overweighting the smaller REITs

- Equal weight:

- Singapore Banks – $200,000.00

- Equal weight:

- UOB

- DBS

- OCBC

- Equal weight:

- Commodities – $75,000

- Equal weight:

- Rio Tinto

- BHP Billiton

- China Banks – $50,000.00

- Equal weight:

- ICBC

- BOC

- CCB

Running a portfolio like that would give me a roughly 6% dividend yield.

On $1 million, that’s about $5,000 dividend income a month.

Let’s discuss some high level questions for both portfolios.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

How much cash to hold in 2023? As a Singapore Investor?

I think the biggest question every investor needs to think about in this climate.

Is how much exposure to risk assets do you want.

Yes, I know that this is the most telegraphed recession in history.

Yes, I know that most commentators now think the recession is cancelled and we’re going to see a “soft landing”.

The way I see it, whether we get a hard or soft landing is going to depend on how the Feds react in the next 12 months.

How they prioritise fighting inflation, vs preventing a recession.

All the soft landing folks are making a big assumption as to how the Feds are going to react.

Which may turn out to be right of course – but when it comes to my life savings I rather be safe than sorry.

So the challenge is trying to find the right balance such that if we get a soft landing you do enjoy the upside, and if we get a hard landing you have cash to buy in.

Personally for me I would want to hold anywhere from 30% – 50% of my portfolio in cash or low risk bonds today.

But frankly there’s no right or wrong here, and you can see 2 different portfolio variations above with very different cash allocations.

REITs – Are Singapore REITs a good investment now? What to buy and how much?

As shared with Patreons, I have been buying REITs the past month or two.

I think where we are in the cycle, we are close to peak interest rates.

The key question now is how long we stay at this level of rates, and whether we see a mild or deep recession.

Whatever the case, it makes sense to start buying some REITs at current prices, while saving enough cash for whatever happens next.

I do think you want to keep it mainly to REITs with heavy Singapore assets though, because the outlook for US and European real estate is much more uncertain in the years ahead.

A lot of names I like are trading close to cycle lows, with 7% ish yields.

That’s a 3.5% yield spread (assuming a long term SG 10 Year yield of 3.5%).

Those valuations are acceptable for me, and I’ve been accumulating.

You can see my fuller thought process and the exact names I’m buying on Patreon.

Bonds – Are Bonds a good investment now? What to buy and how much?

If you agree that we’re at close to peak interest rates, you’ll like bonds (fixed income) as well.

Bonds used to be really hard to access for retail investors.

But the arrival of fintechs like Syfe and Endowus have totally shaken up this space.

If you want a managed solution you can go with something like Syfe Income+ or Endowus Income.

You’re looking at 5-6% yields, with an average duration of 4 year on the bonds.

There is potential for small capital gains if interest rates go down, but because of the short duration you’re buying primarily for the yield.

If you prefer to DIY you can buy the bond funds directly – for eg. PIMCO GIS Income Fund pays a ~6% yields and is SGD hedged.

Do buy via Endowus instead of a traditional broker for the lower fees and trailer fee rebate.

What about long term bonds?

A notable exclusion from both portfolios is exposure to long term bonds.

Think something like the TLT (20 year+ Treasuries), which will do well if we get a hard landing and interest rates are slashed.

I didn’t want to include long term bond allocations because I don’t see risk-reward as attractive for cash investors.

Let’s put it this way.

The US 10 Year trades at 3.7%, versus the US Fed Funds Rate which may go as high at 5.75%.

If you’re wrong and long term interest rates go up, you could be taking big capital losses on long term bonds.

And even if you’re right, what is the upside here?

Now if you’re doing a macro trade and buying call options on the TLT to bet on a hard landing that’s a completely different story.

But as a longer term asset allocation, not so sure if I’m comfortable putting a meaningful amount of cash into long term bonds here.

Commodities – Are Commodities a good investment now? What to buy and how much?

I still like commodities with a 3 – 5 year horizon.

But going into the economic slowdown phase of this cycle.

Do I really want to have heavy exposure to commodities?

Zero commodities doesn’t make sense in case the Feds panic and cut early.

But you don’t want too much exposure too, which is why I dialled back the commodities exposure in both portfolios.

Just look at the past 12 months for Energy, the chart looks terrible.

I do see myself loading up on commodities later on in this cycle, but the exact timing remains to be seen. I would want to get more clarity on how this economic slowdown plays out before adding to commodities.

Patreons will get regular updates as and when I change my view on commodities.

US Shares – Are US Shares a good investment now? What to buy and how much?

The US market has broken into a 2 speed market of late.

You have AI/FAANG which is making new highs.

And you have everything else which hasn’t been doing so great.

If you’re a short term trader you probably want to get in on the AI/FAANG move – but be very flexible and watch out for reversals.

If you’re a long term investor, you probably still want some exposure to US shares, but given the uncertainty over the next 12 months I don’t think you want to overdo it.

Which $1 million dividend portfolio do I prefer?

As you would have realised from the discussion above, I like the first portfolio a lot more.

With a 50% allocation to cash and low risk bonds, it gives me fantastic optionality over the next 12 months.

If we get a hard landing I can buy whatever comes.

If we get a soft landing I can rotate out of cash into equities.

All while collecting a 4.5% yield on this 50% of the portfolio.

While the other 50% is heavy on REITs and US Tech that will do well if we do indeed get a soft landing and interest rate cuts.

I don’t deny that the 4% dividend yield is on the lower side though.

If you do care only about dividends, then the other dividend portfolio gives you a 6% dividend.

But the risk exposure is definitely much higher in my view.

If we get a hard landing, this portfolio is not going to do so well, with much less cash to absorb the impact.

What is the main risk with the pure dividend portfolio?

Going through the exercise above has really made clear to me the dangers of running a pure dividend focussed portfolio.

You see the risk is that if you want to run a dividend portfolio with a yield decently above the T-Bills 3.84% yield.

You’ll be forced to run a portfolio that is very overweight dividend plays, with less exposure to stocks with capital gains.

You’re pretty much limited to a handful of banks or REITs.

And with the commodities you need to go out the risk curve for a higher dividend yield.

Depending on how the next few years play out, there are quite a few scenarios that a portfolio like that might not do so well.

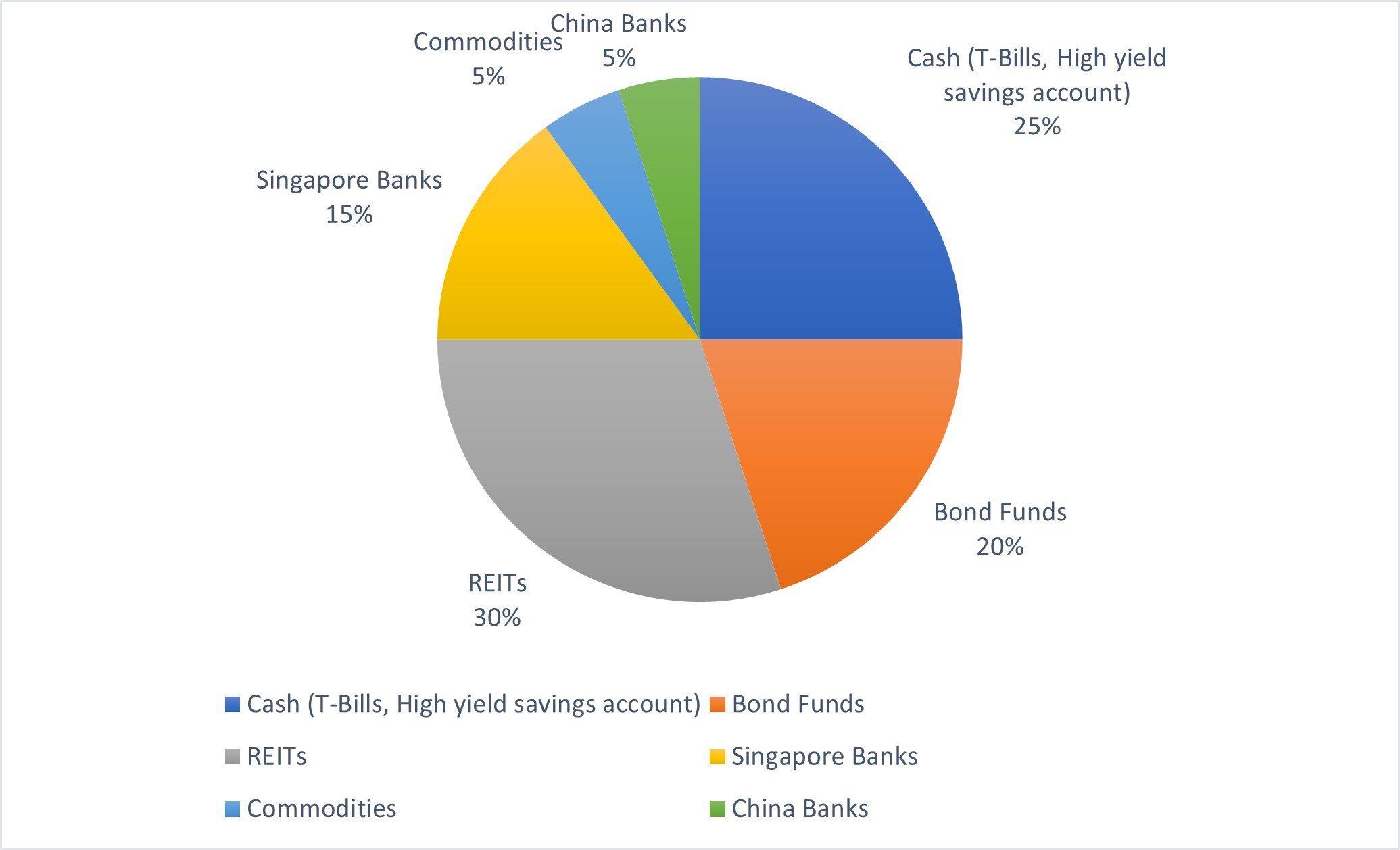

A possible middle ground to invest $1 million? 5.5% dividend yield?

In the course of writing this article I actually came up with a third portfolio, which was a middle ground between the two:

- Cash (T-Bills, High yield savings account) – $250,000.00

- Mix of T-Bills and high yield savings accounts like UOB One

- Bond Funds – $200,000.00

- Either a managed solution like Syfe Income+ or DIY via Endowus Fund Smart (eg. PIMCO GIS Bond Fund)

- REITs – $300,000.00

- Equal weight:

- CapitaLand Integrated Commercial Trust

- Ascendas REIT

- Lendlease REIT

- Keppel REIT

- Keppel Infrastructure Trust

- Equal weight:

- Singapore Banks – $150,000.00

- Equal weight:

- UOB

- DBS

- Commodities – $50,000.00

- Equal weight:

- Shell

- BP

- China Banks – $50,000.00

- Equal weight:

- ICBC

- CCB

The main change of course, is dropping the US shares component which doesn’t pay much dividends, and rotating that into Singapore REITs / banks for a higher dividend.

This allows you to achieve a higher 5.5% dividend yield, which keeping while healthy 25% allocation to cash.

But of course – you’re giving up that capital gains potential for the dividend yield.

Which just goes to show there is no free lunch in this world.

Closing Thoughts: There is no free lunch in dividend investing (or life)

Which frankly, should be the biggest takeaway from this article.

I see many investors just shooting purely for yield – trying to maximise the dividend yield they can get.

But never forget that a 20% drop in portfolio value wipes out 3 – 4 years worth of dividend income.

Yes, you can build a 6% dividend yield portfolio.

Heck, you can even build a 8% dividend yield portfolio if you want.

But don’t let the obsession for yield cloud your judgment over the risks you are taking on.

In the wealth building game, knowing how to keep the money you earn, is as important (probably more important) as knowing how to make the money.

Of the 3, I still think I like the first portfolio the most, as I find it the most balanced dividend portfolio. With the best balance between dividends and capital gains, and optionality in the months ahead.

But hey I would love to hear what you guys think!

This article was written on 22 June 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 500 worth of fractional shares (expires 30 June)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $100 SGD

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH could you walk us through your process on choosing a bond fund? How did you arrive at your choice of the PIMCO GIS fund?

Thanks!

Well the point of the bonds in this portfolio was to get a slightly higher yield in exchange for longer duration and more risk (vs the cash), but not take on too much duration risk (like a 20 year TLT).

So I picked a mid term bond fund with about 3 – 5 years duration, and something Investment Grade which would yield about 5-6ish yields at today’s pricing. Has to be SGD hedged as well because it’s supposed to be lower risk.

PIMCO GIS Fund is just one option, but it doesn’t have to be the only one. the Syfe/Endowus options are more diversified and offer Asian exposure, but they do charge fees. Enterprising investors can DIY if they want to save on the fees.

Hi FH,

You said “You’re looking at 5-6% yields, with an average duration of 4 year on the bonds.

There is potential for small capital gains if interest rates go down, but because of the short duration you’re buying primarily for the yield.”

Personally, I disagree with you that average duration of 4 years is considered short duration. I thought 2 years or less is more accurate definition of it.

As to your view of retail investors being hard to access bonds before these fintech players coming up with managed solutions, I think bond funds had been available in the market for very long time for retail investors. It is just that the industry is not promoting them much due to lower management fees in running them. It is just not a good story to sell than equity funds. So, it is not really lack of options, but rather lack understanding that these products are there.

Fair point, I understand where you’re coming from.

I was comparing vs say a 20 year bond fund, so I viewed 4 years as short. But you are right, the proper word should probably be “mid term” duration.

If I recall correctly, before this bond funds had to be bought via the banks, which charge sales charges, and no trailer fee rebates. Cost wise it was slightly prohibitive.

And also with interest rates at rock bottom the past decade, there was very little incentive to buy bonds as well. This is only just starting to change.

So it’s a bit of a right place right time too I guess.

Hi FH,

Bond funds had already been available via online platforms like Fundsupermart, Dollardex, POEMS etc before this. Most do not charge sales charges, though some do charge platform fees if you invest on their platform via cash. For CPF funds, they don’t charge platform fees.

I think one should not just look at interest rate and then look at bond funds. It should be part of one’s overall asset allocation plan, regardless of where interest rate is heading.

Thanks, appreciate the sharing. 🙂

Hi FH,

You have forgotten to add that out of the $1 million, some funds should be set aside to support your Patreons articles. Heehee.

Regards,

Gerald

https://sgwealthbuilder.com

Hahaha, good point. Good to hear from you Gerald!

Hi FH, appreciate your post. I seem to see u post similar post every other month, wld appreciate if you stick to one strategy and monitor its progress over the year not change every time the market has some adjustments

I think the issue is that new evidence comes to light every day that changes the outlook going forward. So active investors will need to continually tweak their asset allocations.

If one wants to go pure passive, then one can run something like an all weather. In which case there is no need to monitor daily news at all, you just run that portfolio for the next few decades rain or shine.

So it really depends on whether the investor wants to be active or passive. If you’re active the portfolio changes are inevitable. If the world changes, investors will need to change as well.

Hi FH,

What is your take on gold? With the uncertainty in the banking sector, there is a strong possibility that gold price will cross the pivotal US$2,000 per troy ounce resistance level to smash a record US$3,000 per troy ounce. This is not an impossible scenario as the emergence of the pandemic in 2020 led to gold price surging to a high of US$2,040 per troy ounce in August 2020. Gold price was in buoyant form in 2020 because the precious metal is viewed as a safe haven in times of uncertainties.

The series of interest rate hikes in 2022 to early 2023 had caused gold price to plummet to a low of US$1,620 per troy ounce in November 2022. However, with the banking crisis unfolding, the Fed had signalled a pause in the interest rate hikes.

In my view, it is too early to claim that the global banking crisis is over as Deutsche Bank shares plunged recently following a surge in credit default swaps. Let’s face it. Unless one works in the investment banking industry, most retail investors will never know what’s going on behind the scene. In fact, the bushfire could be raging right now. Question now is: how many more banks would blow up like Silicon Valley Bank and Silvergate? The collapse of Credit Suisse and the ongoing crisis of confidence of Deutsche Bank could be just the beginning of another massive financial crisis. Henceforth, in my opinion, there is a strong possibility that the Fed would start to trim interest rates in the latter half of the year.

Regards,

Gerald

https://sgwealthbuilder.com

I think the problem with gold is twofold.

Firstly if real rates stay high (or go higher) in the short term, gold is going to underperform.

Secondly, if we do get a hard landing / liquidity style event, gold is going to sell off.

So the question then is what scenario would gold do well.

Some kind of goldilocks event where we get a soft landing, and real interest rates stay low, with money printing. But I struggle to see how we get from where we are today to that goldilocks scenario for gold without one of the 2 scenarios above.

China banks’ share prices drop to near the lows in late 2022. This is partly due to price trading at ex-dividend. Now could be a good time to re-look at China banks.

Interesting indeed. Let me write on them this weekend.