I’ve been getting a lot of questions about blue-chip REITs recently.

The REITs from Mapletree, CapitaLand, Frasers etc.

Prices of the blue-chip REITs have not dropped as much as the smaller REITs, so comparatively I think there is less value here.

But I know many investors value price stability, and like the peace of mind that comes with owning a blue-chip REIT.

Top 3 REITs I will Buy in 2023 / 2024 – As a Singapore Investor, Blue Chip REITs only

So in today’s article, we’ll look at blue chip REITs only.

Which are the Top 3 blue chip REITs I may consider buying in the next 12 months?

When I say blue chip I mean a REIT from a top tier sponsor, with a long-term track record of stability.

In my mind, this means REITs from one of the 3 sponsors:

- CapitaLand

- Mapletree

- Frasers

- Keppel (maybe)

CapitaLand Integrated Commercial Trust

Current Price: $1.89

Annualised Dividend Yield: 5.6%

CICT – CapitaLand Integrated Commercial Trust, needs no introduction.

Formed by the merger of CapitaLand Mall Trust and CapitaLand Commercial Trust, this REIT holds one of the best retail mall portfolios in Singapore, with one of the best office portfolios.

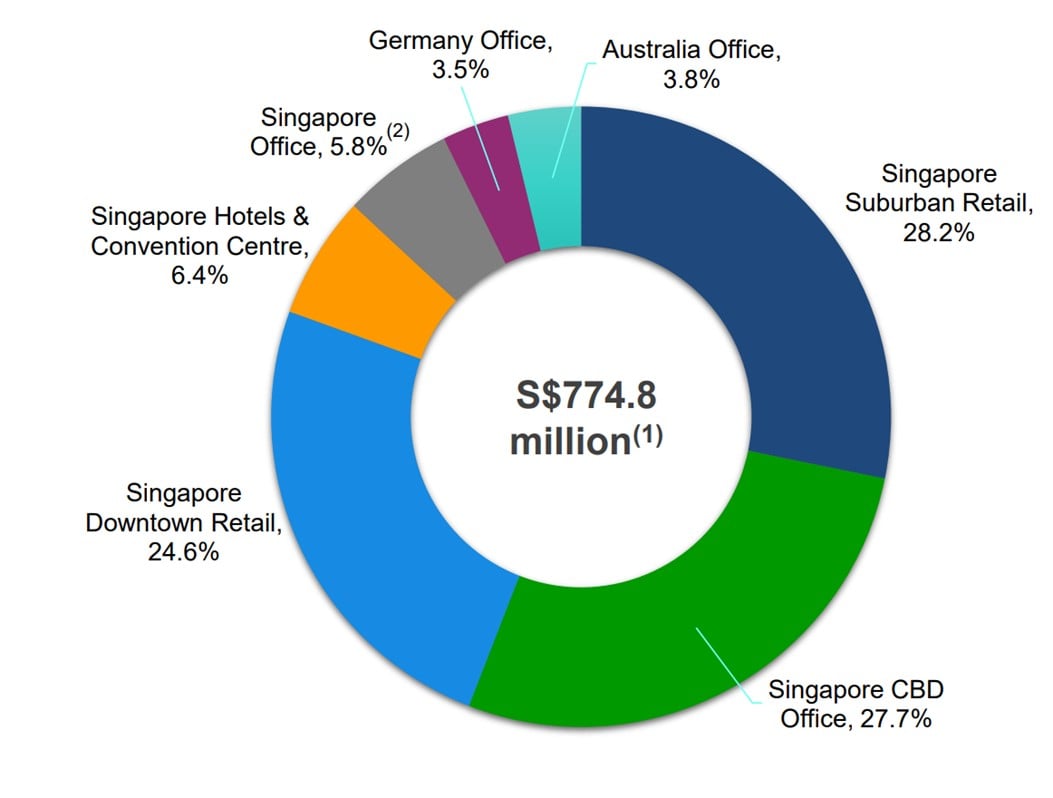

More than 90% of the revenue is derived from Singapore properties, which is exactly what you’re looking for today with all that uncertainty over global real estate.

Just like all other REITs, CICT’s share price has not been doing well due to rising interest rates.

At current price of $1.89, it sits at a long term support level going back the past decade.

Note that if this support level breaks, the next support is at $1.75 (2022 lows), and after that $1.5 (COVID levels).

Dividend yield of CapitaLand Integrated Commercial Trust

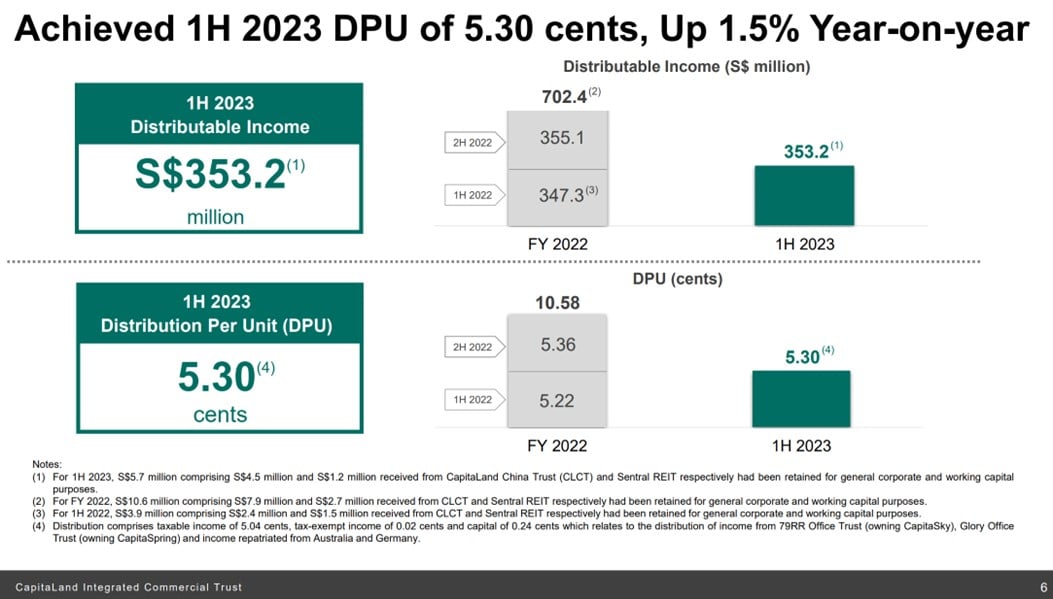

DPU is up 1.5% year on year, which is frankly very good when you compare with most other REITs that are reporting negative DPU due to higher interest rates.

If you annualise the 1H 2023 DPU, you’re looking at a 5.6% dividend yield.

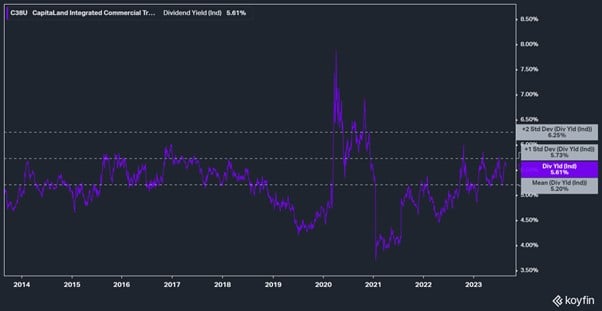

Here’s what the dividend yield looks like over the past 10 years.

Current dividend yield is about 1 standard deviation above the average.

If CICT drops to 2 SD below average, that means a 6.25% yield or $1.7-ish, which would be great value if it gets there.

Do note that the chart below mainly reflects CICT’s dividend yield in a decade where interest rates were stuck at rock bottom.

So in a decade of higher interest rates, technically speaking the yields will need to adjust up to compensate (CICT at a 5% yield when T-Bills yield 1% makes sense, CICT at a 5% yield when T-Bills yield 4% doesn’t make sense).

Financial Results of CapitaLand Integrated Commercial Trust

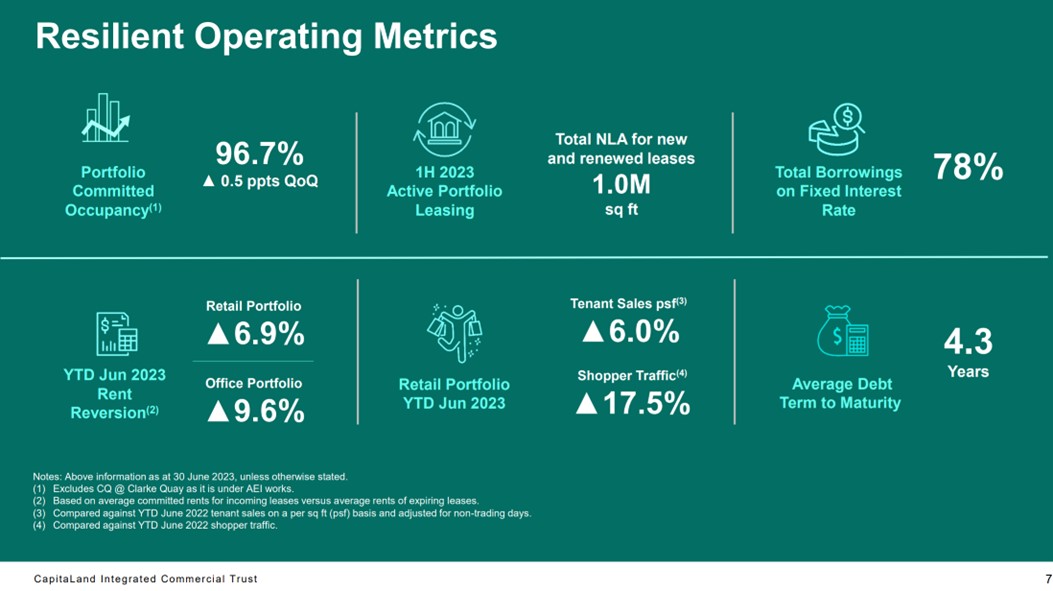

Operating metrics are very good as well.

6.9% rental reversion for the retail portfolio, and 9.6% for the office portfolio.

I’m not so sure if CICT can keep up this kind of rental reversions going forward though.

With the economy slowing, and more office supply coming online, I would expect rental reversions to moderate going forward.

Which means that you won’t have higher rentals to offset for the higher interest expenses.

Of course, it also depends on how quickly the Feds cut interest rates in 2024, and that’s a whole discussion in itself.

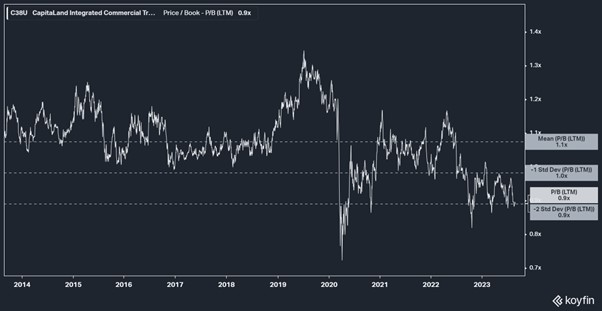

Book Value of CapitaLand Integrated Commercial Trust

NAV is $2.07, which means CICT trades at 0.91x book value today.

You can see this in historical context below.

CICT trades at 2 standard deviations below average

Whereas dividend yield is only 1 standard deviation below average.

This just goes to show you the devastating impact higher interest rates can have on REITs.

This CapitaLand REIT has a 3.2% cost of debt, 3.3x interest coverage ratio, and 40% leverage.

As you’ll see with the other REITs on this list, this is pretty much baseline standard for Singapore REITs today.

Yes, these kind of leverage ratios would look out of place any time in the past decade.

But in this new paradigm of higher interest rates, REITs are running much higher gearing today.

My views on CapitaLand Integrated Commercial Trust?

If you want to buy one REIT to get broad exposure to Singapore office and retail, and you don’t want to fuss too much about stock picking – CapitaLand Integrated Commercial Trust is probably your go to REIT.

Current price works out to a 5.6% dividend yield, and 0.9x book value.

I wouldn’t say that it’s an absolute must buy at this price, but I don’t deny that you’re looking at support levels going back into the mid 2010s.

It’s probably a decent enough buy at this price.

If you want to get greedy and wait for it to get lower.

The next support level is $1.75 (2022 low), followed by $1.5 (COVID low).

Full disclosure that CICT is one of my biggest REIT positions today.

At this price, I don’t see a big need to add given my already large exposure.

If it drops to 1.75 or 1.5 support levels though – I’m probably going to add.

Let’s see.

Mapletree Pan Asia Commercial Trust

Current Price: $1.53

Annualised Dividend Yield: 5.7%

How the great have fallen.

A long time ago when I started Financial Horse.

One of my first articles was on how Mapletree Commercial Trust with Vivocity and Mapletree Business City was probably my favourite REIT at the time.

In my view, Vivocity and Mapletree Business City are best in class retail and commercial properties respectively.

As fate would have it – Mapletree Commercial Trust merged with Mapletree Greater China Commercial Trust.

While CapitaLand Mall Trust merged with CapitaLand Commercial Trust.

And today I would say portfolio wise – CapitaLand Integrated Commercial Trust is probably the better REIT.

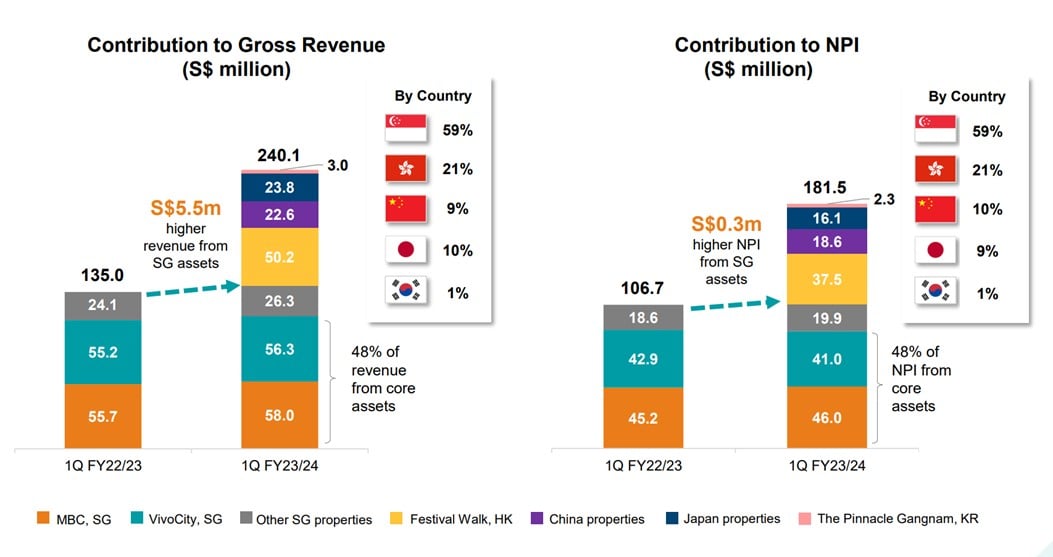

Mapletree Pan Asia Commercial Trust’s share price has been very disappointing of late – primarily due to the Hong Kong exposure.

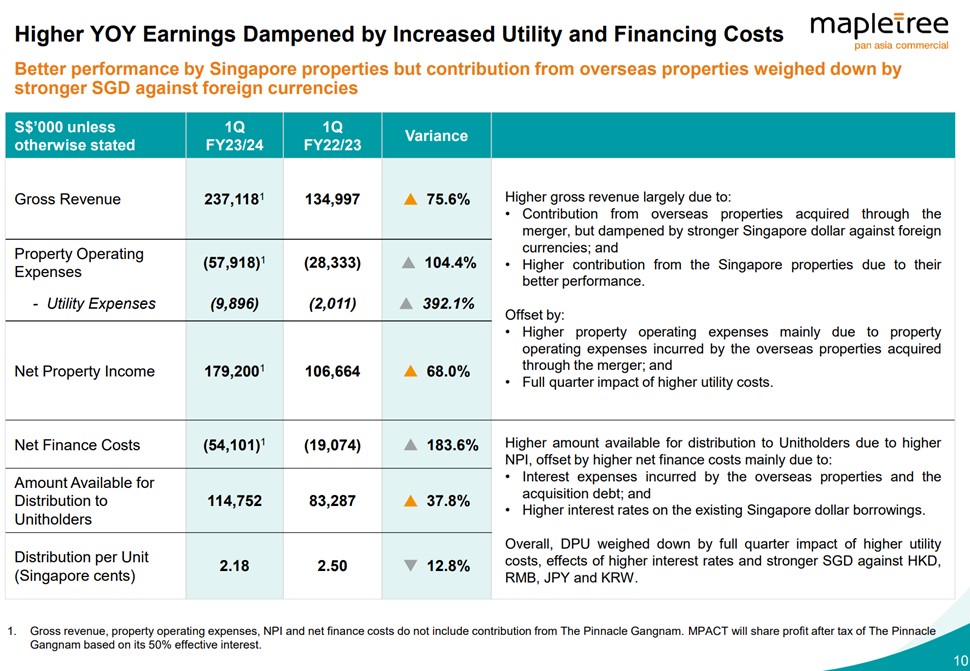

Financial Results of Mapletree Pan Asia Commercial Trust

Here’s DPU – down an absolutely ridiculous 12.8%.

Official reason is due to:

- Higher interest expenses

- Stronger SGD

Book Value of Mapletree Pan Asia Commercial Trust

NAV is $1.75, which works out to a 0.87x book value.

Notice how this is only slightly cheaper than CICT (0.9x book), despite having almost 40% exposure to HK assets.

What is a fair value for this Mapletree REIT?

Let’s say we assume a 1x book value for SG portfolio (premium to CICT because Vivocity and Mapletree Business City are best in class assets).

But the HK/rest of portfolio we’ll use a 0.55x book value, which is where Link REIT (Asia’s largest retail REIT) is trading.

That gives us a fair value of 0.8x book value – $1.4.

So conclusion is either that (a) Link REIT is very cheap, or (b) Mapletree Pan Asia Commercial Trust is expensive.

Either way, it doesn’t look so good for MPACT.

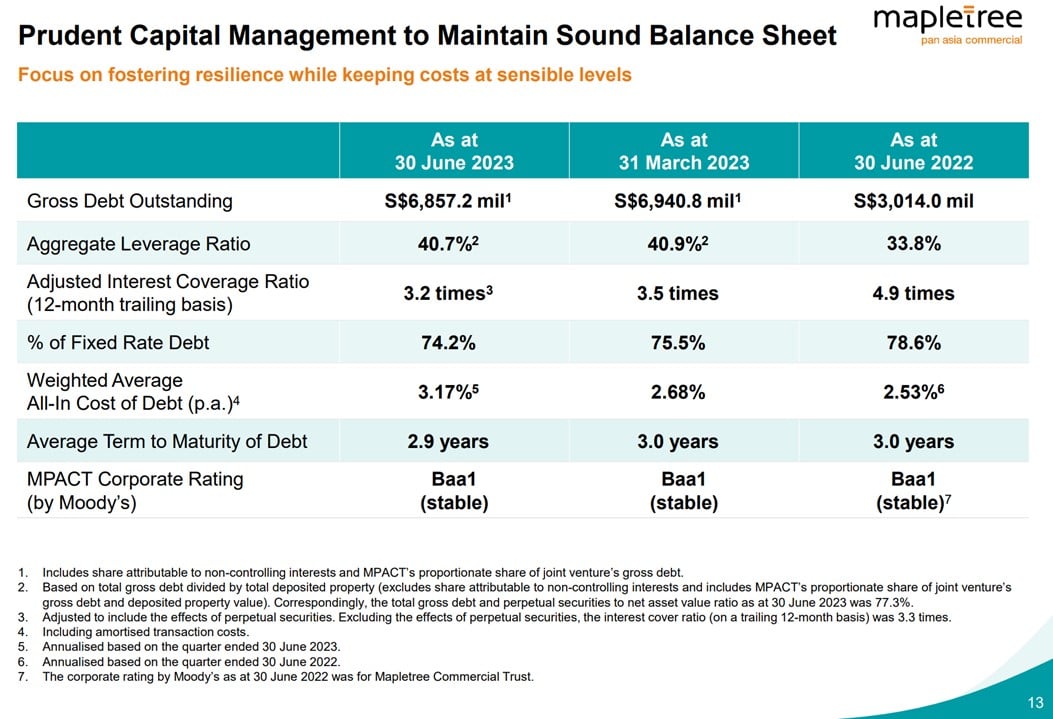

Debt metrics for Mapletree Pan Asia Commercial Trust

This REIT has a 3.2% cost of debt, 3.2x interest coverage ratio, 40% leverage.

This is almost exactly in line with CICT above.

Will I buy Mapletree Pan Asia Commercial Trust?

I don’t think Festival Walk (HK retail mall) is best in class.

Because of this, I took the all cash option from Mapletree Greater China Commercial Trust’s merger.

And I never rolled the position into Mapletree Pan Asia Commercial Trust (nor have I added to this REIT since the merger).

Does that change today?

Well – if I wanted HK exposure, there are a ton of options out there with better HK real estate portfolios, trading at better prices today (because of the sell-off on China contagion fears – check out Patreon for fuller views).

So I’m not buying MPACT for the HK portfolio.

I’m buying MPACT mainly for the SG portfolio, which I still do not doubt is best in class and one of the best ways to play the Greater Southern Waterfront story.

Today’s MPACT price I would say is probably fair, and I don’t mind adding.

But like I said, I don’t find this REIT particularly cheap when you consider that the largest Asia REIT with a much better HK portfolio (Link REIT) trades at a 0.55x book value and 7% dividend value.

Mapletree Commercial Trust used to be a best in class REIT, but today the HK portfolio is dragging it down.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Ascendas REIT

Current Price: $2.76

Annualised Dividend Yield: 5.6%

Okay, so many of you have asked for my views on Ascendas REIT.

So let’s have a closer look.

Latest Financial Results of Ascendas REIT

Latest DPU shows a 2% drop in DPU, largely due to higher interest expenses.

You know how you guys asked me last year whether REITs are a good buy because higher rentals will offset the rise in interest expenses?

And my answer was that the rental increase will not be sufficient to offset the massive rise in interest rates from the fastest Fed hiking cycle in 25 years?

Well, we’re pretty much seeing that play out today.

Rental reversions are very strong at 14.2%, and yet DPU is going down.

Never underestimate the impact of rising interest rates as a real estate investor.

Dividend of Ascendas REIT

Annualised dividend works out to about 5.6%.

This is surprisingly close to the 10 year average dividend yield (5.6%) – which is strange because most other REITs are trading well above historical yields.

I’ve never really understood why.

But for some reason investors love Ascendas REIT and price it at a premium to other retail / commercial blue chip REITs.

Book Value of Ascendas ERIT

NAV is $2.32 so PB is 1.19x

You can see the 10 year chart below, this is about 1 standard deviation below average – not particularly cheap given the interest rate climate.

I do want to highlight that Ascendas REIT today – is only 63% Singapore assets.

The rest being a mix of the US, Australia and Europe.

Is such a premium valuation justified for a REIT that is only 63% Singapore assets?

As the real estate / interest rate cycle plays out over the next 12 months, how will the US / Europe / Australia portfolio perform?

Debt levels of Ascendas REIT

You’re looking at 3.3% cost of debt, 4.3x interest coverage ratio, and 36% leverage.

You’ll notice that the interest coverage ratio is significantly better than CICT or MPACT above despite the same cost of debt.

And that really comes down to the lower 36% leverage Ascendas REIT is running (vs 40% for the other 2 REITs).

REITs are really in a catch 22 situation here.

Issue equity and the market will absolutely hammer your share price.

Issue debt and pay up for the privilege to borrow in this climate.

The longer that interest rates stay high, the more pain REITs will see.

Will I buy Ascendas REIT?

There is soft support at the 2.6s range, so if I wanted to pick up Ascendas REIT I would probably wait for that range.

I do want to highlight that Ascendas REIT today – is only 63% Singapore.

The rest being a mix of the US, Australia and Europe.

And throw in the fact that dividend yield at 5.6% and P/B at 1.2x is not particularly attractive by historical standards.

And I’m not sure if I see a lot of value in Ascendas REIT today.

For the record, I do hold a position in Ascendas REIT today, and at the right price I will likely add.

But as of today, I’ll probably just hold my position for now.

Mid Cap REITs offer much better value?

Having gone through all the blue-chip REITs to come up with this list.

I still can’t shake the feeling that comparatively speaking – I think the mid cap REITs offer better value today.

But just to pull up some charts for illustration (not saying these are good buys).

Starhill Global REIT well below pre-COVID prices (8% yields).

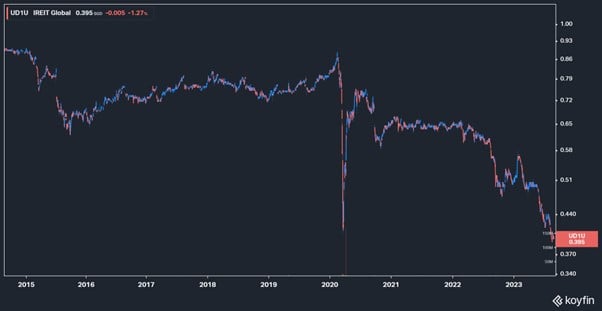

IREIT Global below COVID lows (8%+ yields):

Suntec REIT close to COVID prices (7%+ yields):

I’ve shared fuller views with Patreons on the mid cap REITs that I like and may add, so do sign up if you are keen.

Yes, I know the mid cap space is much more volatile.

But look at the charts above, and I think that for investors keen to stock pick individual names, and hold long term for yield, there are some unbelievable buys out there right now.

Whereas the large-cap, blue chip REITs are attractive no doubt, but I don’t think you will see the same upside potential on the other side of the interest rate hike cycle.

But hey – we’re only at the point in the interest rate cycle where the Feds pause for an extended period.

If history is any guide, the fireworks usually comes when the Feds start cutting, and not before.

For REIT pickers, there looks to be some unbelievable buys in the months / years ahead.

I recently updated the REIT & Stock Watchlist on Patreon – that sets out the REITs / Stocks I am keen to purchase, and approximate price targets.

Some pretty crazy valuations out there for mid cap REITs.

Do sign up if you are keen.

This article was written on 31 August 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Any comments on oue reit? The dividend looks very attractive now after the recent drop. The portfolio is mainly Singapore.

Not the biggest fan of the sponsor. At least for me – but I can’t speak for all investors.

Really disappointed with the performance and management of MPACT! Been a long-time shareholder since they only had SG assets, progressively adding more as they hit lows during COVID and the stock performance is still dismal.

Indeed! I haven’t added to this REIT ever since the merger, and for good reason given how terrible performance has been.

At 1.5 there is very strong support going back a decade or more, but I wonder if this REIT will touch 1.4+ this cycle. If you compare with something like Link REIT the HK portfolio is not cheap even at this price.

Agreed on the consistently poor share price performance of MPACT. FH, I’m interested in hearing your thoughts; hypothetically speaking, what do you think the management of MPACT should do to unlock value for the shareholders? Divest the HK properties & refocus/reinvest in SG assets?

That’s a very good question.

For what it’s worth, I dont think they should sell FW.

Won’t get a good price for it, and even if they sell what do they do with the proceeds? No more good malls to buy in SG that are not already in a REIT, and everything else is too small to move the needle for MPACT. If they sell HK to buy US/European real estate you’re stuck with the exact same problem.

Short of the Sponsor coming in to buy out FW (which they likely wont because they already sweetened the deal significantly for MGCCT unitholders), dont see any easy solutions here.

Best option probably is to do nothing and hope for a turnaround in HK.

Thanks for the well thought-out reply; makes sense. As for us shareholders, there’s also nothing else we can do except hold onto MPACT for the SG assets.

Hi FH,

Despite the sluggish form of Mapletree Logistics Trust unit price for the past two years, I have conviction in this S-REIT. This is because I had made money from this counter before. In April 2021, I had bought 40,000 shares at an average price of $1.965 and then cashed out at $2.12 per share. Excluding the distributions, I had made a tiny profit of $6,200. The profit represented 15.5% within the span of three months.

Given the track record, I don’t see why this counter would not recover its form again. It’s only a matter of time that light at end of tunnel will arrive for Mapletree Logistics Trust unit price. The latest financial result provides some interesting data and I will share my insights in this article.

Regards,

Gerald

https://sgwealthbuilder.com

Interesting – thanks and appreciate the sharing.

I hope a position in MLT as well, but not a big position. Never really added the past few years as I dont really see the upside other than the yield. At this price isnt it already pricing in a lot of future growth, especially when you look at the other REIT valuations out there?