Okay so A LOT of you have asked for my views on Lendlease REIT.

I did an article for Patreons a couple of weeks back.

But given that Lendlease REIT’s share price has stabilised in the $0.55 range since.

And given the overwhelming demand – I decided to do an updated deep dive.

Lendlease REIT’s price action is a disaster

Let’s not mince words.

The price action is an absolute disaster.

$0.60 is a key support level that goes back to 2020.

Over the past few weeks, Lendlease REIT broke below that key support – which is never pretty.

Since Lendlease REIT went ex-dividend in early August, the share price has collapsed from $0.66 to $0.55.

That’s a 17% drop, at a time when most other retail REITs have only dropped 5% (or so).

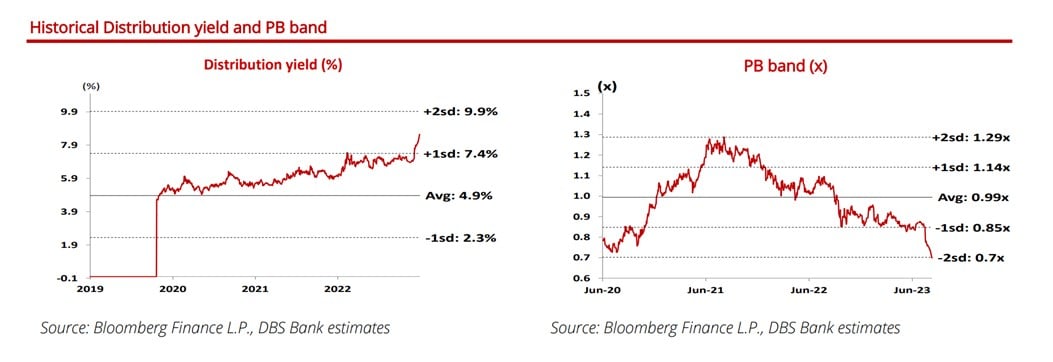

Lendlease REIT is very cheap on a valuations basis

Whatever way you look at it, Lendlease REIT is very cheap on a valuations basis.

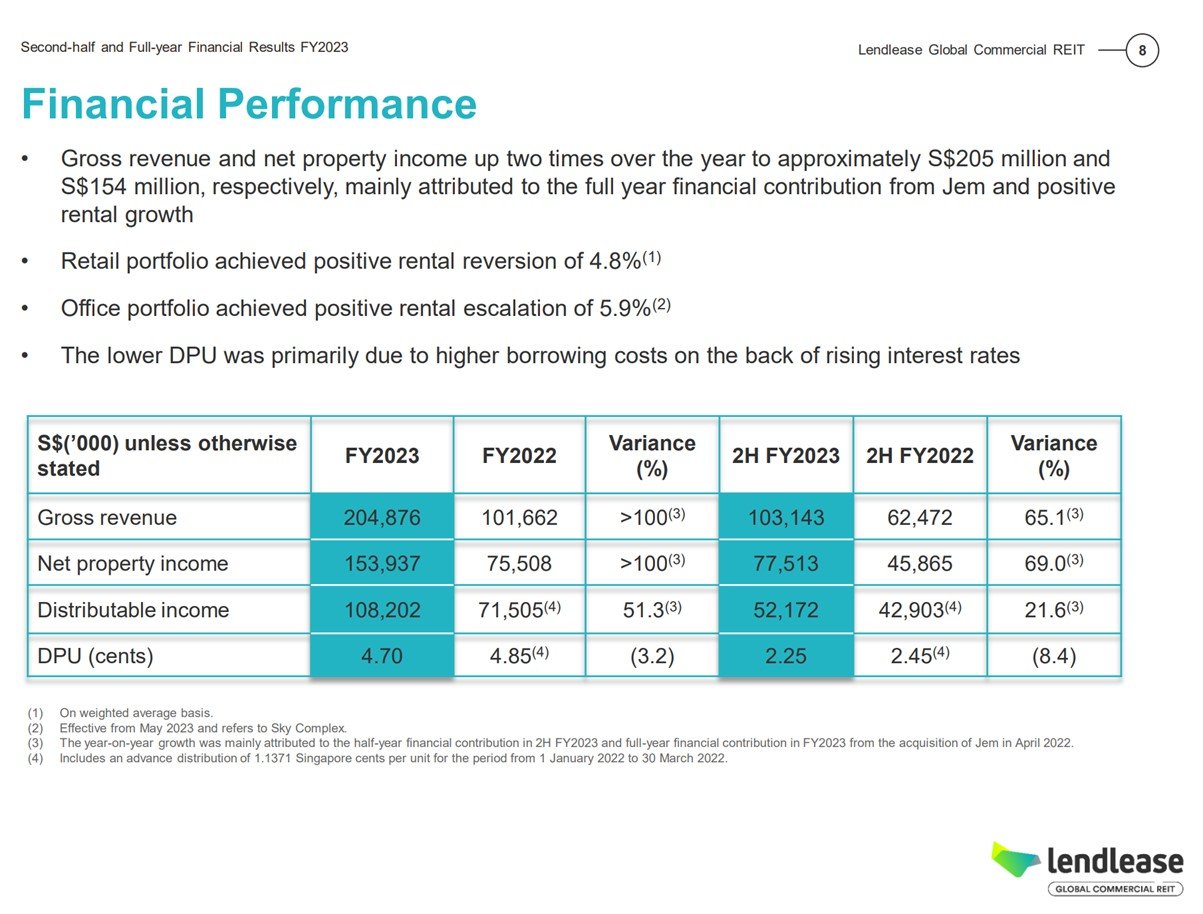

Lendlease REIT pays a 8.5% Dividend Yield

Trailing twelve month dividend yield is 8.5%.

DPU did drop quite a bit (8.4%) for the most recent financial results due to higher financing cost.

But even if you annualise the lower 2H FY2023 DPU – it gives you a 8.1% dividend yield at the current price ($0.55).

Lendlease REIT trades at a 0.7x book value

Book value is equally cheap.

NAV is $0.79 – which works out to 0.7x book value.

That’s 2 standard deviations below mean – at the levels Lendlease REIT was trading at during COVID.

Crazy stuff.

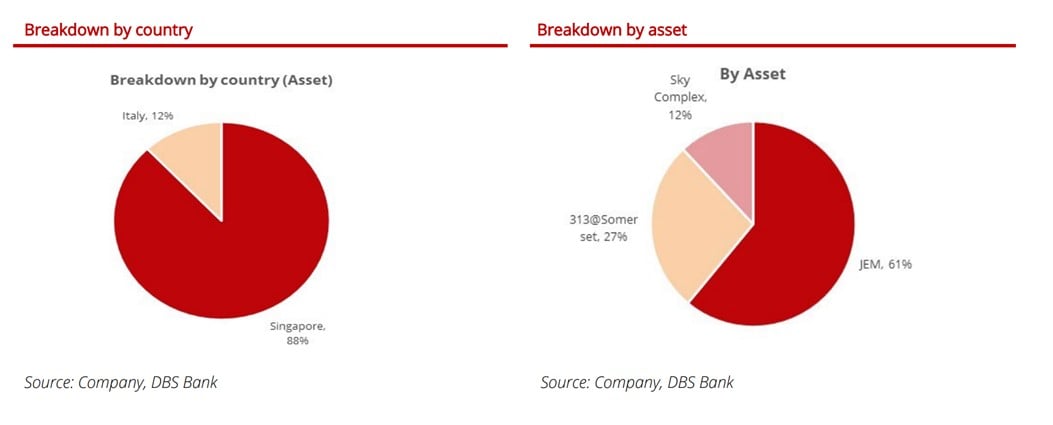

Lendlease REIT has arguably one of the best retail portfolios out there

If you look at the valuation metrics above – you would think this is some small REIT holding low quality assets.

But no.

In my view – Lendlease REIT has arguably one of the best Singapore retail portfolios out there today.

In fact if you ask me to pick the REIT with the strongest Singapore retail portfolio today, Lendlease REIT would rank way up there together with MPACT, CICT and FCT.

Jem, Somerset 313, and recently a 10% stake in Parkway Parade.

All very strong malls.

Jem is arguably one of the best suburban malls in Singapore – and at 61% of Lendlease REIT, this is what you are buying.

Somerset 313 is a very unique mall in Orchard targeting a younger crowd.

While Parkway is another solid suburban mall with a strong catchment.

Okay there is Skycomplex in Italy, but that’s only 12% of the asset base (even lower after the Parkway acquisition).

Asset quality shows in rental reversions

For what it’s worth, the asset quality shows in the financial results.

Rental reversion of 4.8% for the retail portfolio, and 5.9% for the office portfolio.

Pretty solid.

2 big risks with Lendlease REIT

So… what would explain the big sell-off?

The way I see it, it comes down to 2 reasons:

- Lendlease REIT has a lot of debt – risk of (a) breaching gearing ratios, or (b) higher interest expense

- Market is pricing in a big dilutive equity fundraise – to (a) pay down debt, or (b) buy Parkway Parade

Let’s discuss each.

Lendlease REIT has a lot of debt

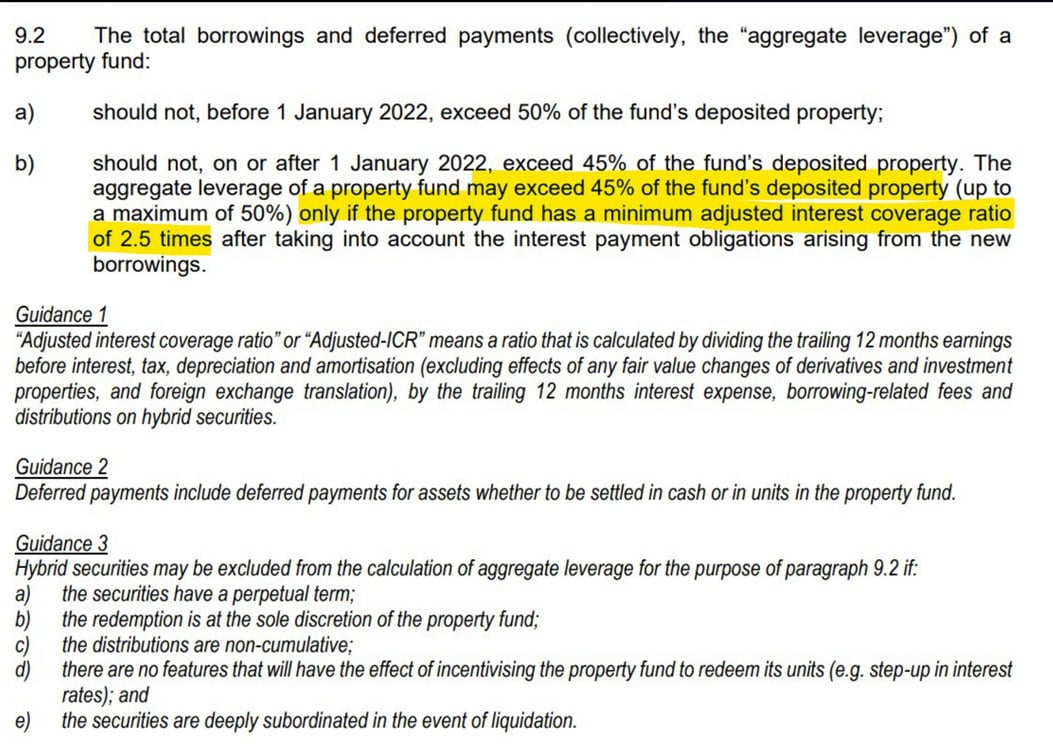

Current gearing ratio is 40.6%.

But they have $400 million in perpetuals on top of that.

Add that in and you get a total effective gearing of 50%, definitely on the high side.

Average cost of debt is 2.69% which is low (most other REITs are running 3.2% – 3.3%).

This implies interest expense will go up in the months ahead – meaning more drops in DPU.

The results in 2 potential problems:

- Risk of breaching the 45% gearing limit

- Higher interest expenses

Risk of breaching the 45% gearing limit

Lendlease REIT’s interest coverage ratio (ICR) is very low – adjusted ICR is 2.0 times.

This means that under MAS’s CIS Code, Lendlease REIT cannot raise its gearing above 45% (40.6% right now).

Investors may be reminded of what happened with Manulife REIT.

Think about it this way – imagine the REIT has $100 in assets, and $40 in debt.

That’s 40% gearing which is fine.

Now imagine the asset value drops to $80.

That same $40 in debt works out to a 50% gearing ratio (40/80).

Even though debt didn’t go up, your gearing went up because of a fall in property prices.

And now the REIT is in breach of its gearing ratio and cannot take on new debt.

While being in breach of financial covenants (can’t pay distribution yield), and needs to sell assets to bring gearing down.

In a doom loop – exactly what happened with Manulife REIT.

Is there a risk of the same happening with Lendlease REIT?

DBS released an absolutely fantastic report on Lendlease REIT this week.

They address this exact question in the report, and here is their analysis (emphasis mine):

Asset values supported by improving cashflows; LREIT has buffer for a further 10% decline in asset value declines before gearing hits 45%. Overall gearing for the REIT has risen from an average of 32%- 35%% in FY20/21 to the current c.40.6%, which remains manageable in our view. Our confidence stems from LREIT’s exposure being concentrated to Singapore and defensive retail assets. We believe these properties show capital value resilience, on the back of cashflow recovery

Singapore assets (namely JEM and 313@Somerset) continue to see stable cap rates and higher valuations on the back of cash flow transactions and supported by market transactions.

We believe the strong cashflow improvement, coupled with recent retail asset transactions at cap rates of 4.5%-4.9% support capital values during this stage of the interest rate cycle. Based on our estimates, LREIT has a buffer against further softening of assets prices of c.10% before it hits the c.45% gearing limit. This implies a cap rate expansion of 50 basis points, a scenario we believe is unlikely for now within both its Singapore and Italy assets, unless interest rates continue to rise unabatedly.

What is DBS saying?

Basically, DBS is saying that underlying cash flow from the properties are strong.

These are high quality Singapore retail malls, not US offices (in the case of Manulife REIT).

Lendlease REIT needs to see a 10% drop in property prices before it hits the 45% gearing limit.

Which DBS doesn’t see as likely for now – given the quality of the portfolio.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

What do I think?

For what it’s worth, I’m inclined to agree with DBS on this one.

Jem, Somerset 313, Parkway – these are very high quality Singapore retail malls.

At 4.5% and 4.25% cap rates, they are not cheap (a fair retail cap rate is probably around 4.75% today).

But not to the extent that it would need to be revalued down 10% in the next 12 months.

Cash flow from the properties should remain stable going forward.

Manulife’s situation was very different with US offices and the whole remote working trend leading to soaring vacancies.

Higher Financing Cost for Lendlease REIT?

What about higher financing cost, because of all that debt?

Again, DBS has a fantastic analysis on this (emphasis mine):

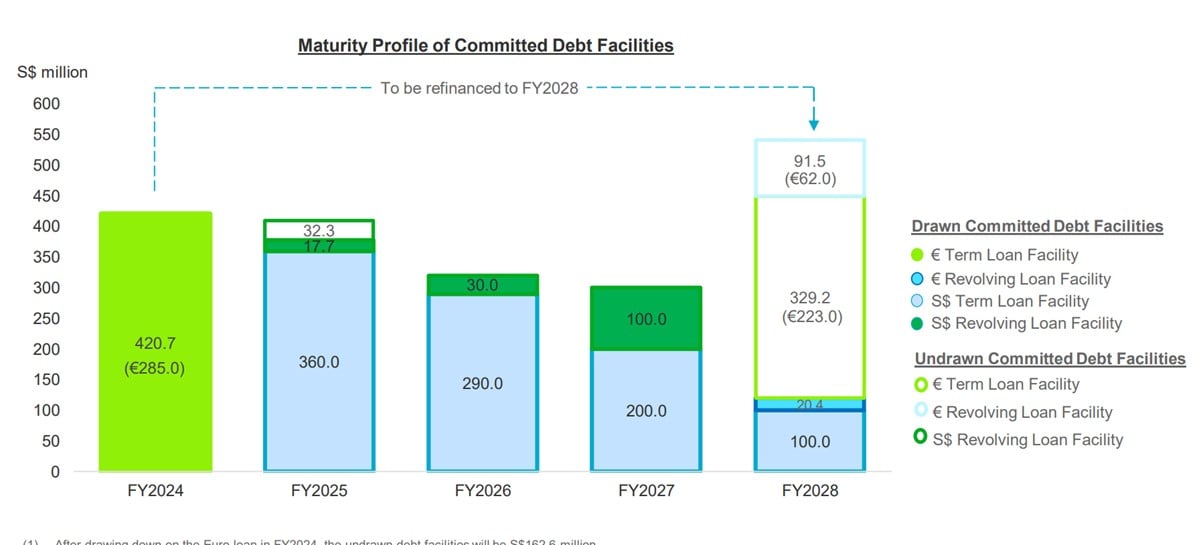

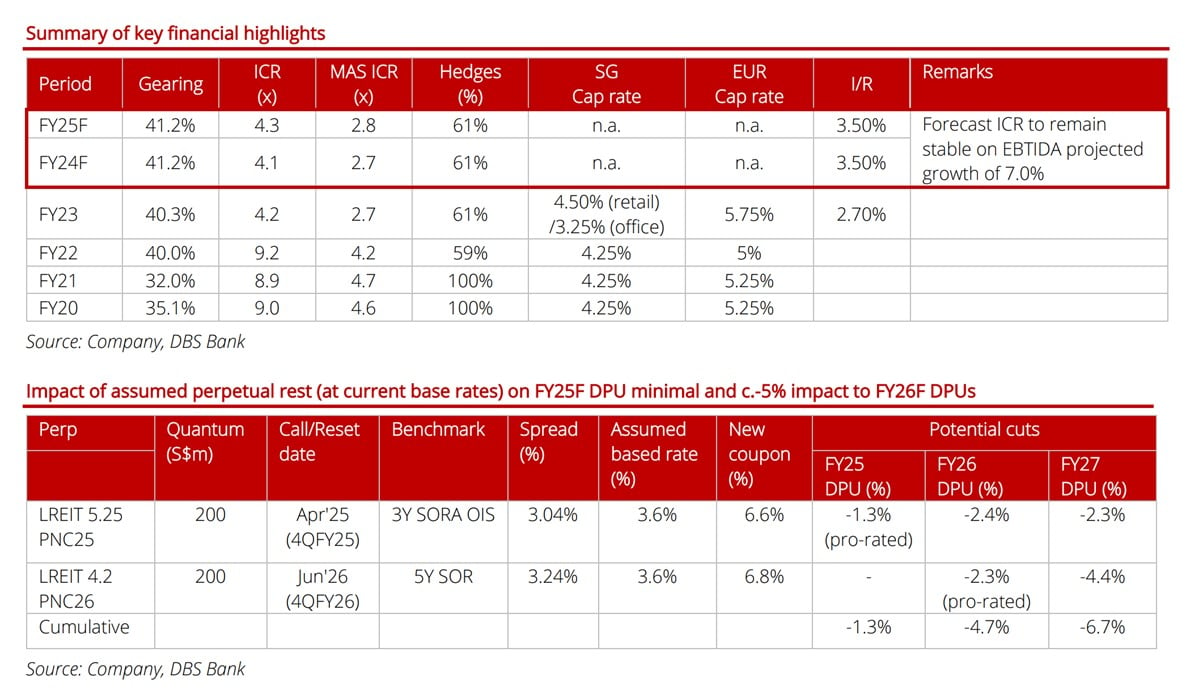

LREIT’s interest coverage ratio (“ICR”) has been declining over time and as of Jun’23, stands at 4.2x (or 2.7x based on MAS computation of ICR ratio). This drop in ICR ratio is mainly due to higher interest costs, which is projected to settle around 3.3%-3.5% in FY24-25F after refinancing of its EUR285m (or c.S$421m loan) loan sometime in Oct’23 (2QFY24), its only debt that is expiring in this financial year.

FY25 (from Jul’25) will be the year to monitor as LREIT looks to refinance close to S$400m of SGD loans taken to partly fund the acquisition of its Singapore properties. Depending on the interest rate environment then, cost of renewal could be stable from current levels or see a softening of interest rate environment which will benefit LREIT’s loan renewal given its c.61% loan hedge ratio.

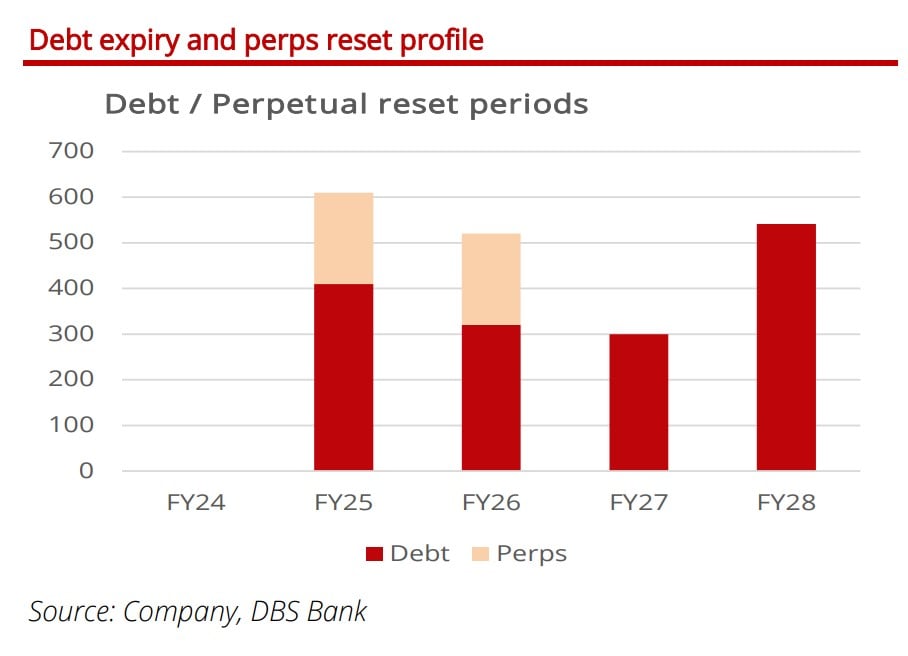

We note that LREIT will be looking to refinance 2 tranches of perpetual securities (S$200m 5.25 PNC25) in April’25 and S$200m 4.2% PNC26 (call in Jun’26). These will be reset at the prevailing swap rates with a spread of 3.043% and 3.24% respectively. These reset in perpetual securities has not been priced into our estimates given that recall dates are >1.5 years away.

Factoring in impacts of a reset in perpetual securities via a sensitivity analysis, we note that near-term concerns in FY25/FY26 on perpetual renewals will be at a -1% and -5% impact to DPUs respectively.

In the rare event that we do see high interest rates lasting more than 3-years into FY27, the cumulative impact of a reset of both perpetuals will see a 7% impact to our FY27 DPUs. We believe that the current share price has more than priced in impact of the renewal of perpetuals, even in the worst-case scenario.

What is DBS saying?

It’s a bit technical, but what DBS is saying can be summed up as follows.

Lendlease REIT has no debt due for refinancing until July 2025.

So you’re clear for basically the next 1.5 years.

The problem comes in 2025.

In July 2025 Lendlease REIT will need to refinance $400 million of SGD loans.

On top of that, it has $200 million in perpetuals to be refinanced in April 2025 and June 2026 respectively.

If they don’t refinance, the interest rates on the perpetuals will go up.

Assuming both Perpetuals reset, then that is a 7% drop in DPU, in FY2027.

What do I think?

The way I see it.

Lendlease REIT *should* be able to manage the financing issues for 2024.

But if interest rates are still high in 2025.

Or if interest rates continue to go up further in 2024.

There may be problems for Lendlease REIT.

But then again, if interest rates stay at these levels for the next 1.5 years it doesn’t matter what REIT you buy.

All the REITs are going to be crushed anyway.

And the way I see it, the interest rate risk over the next 12 – 18 months is tilted to the downside, not the upside.

So personally I don’t see the financing problems as the big risk.

The big risk to me is this next point.

Market is pricing in a big dilutive equity fundraise for Lendlease REIT?

The thinking goes like this.

Lendlease REIT has very high gearing.

It also recently bought 10% in Parkway Parade, which implies that it is likely to buy the rest of Parkway in the years ahead (just like Jem).

Given how depressed share price is, if they do an equity fundraise in this climate – that is going to be massively dilutive.

How realistic is this?

DBS’s response

DBS again, has a response ready:

While investors are concerned if LREIT could be pressed to do a capital raise to address perceived balance sheet weakness, we believe management is unlikely to pursue this strategy, given that raising equity at 0.6x – 0.7x P/B with forward yields reaching 9% will wreck the goodwill and track record that management has built over time. We believe that any fund raising being considered by the management is likely to be on the back of an accompanying acquisition that will be DPU accretive. While LREIT has an attractive acquisition pipeline in Paya Lebar Quarters and the remaining stake in Parkway Parade, we believe these are likely to be medium term opportunities, after the interest rates environment stabilises.

In the worse-case scenario of management requiring to bring down its gearing, we believe that an asset sale of JEM Tower or Sky Complex could be the more likely route. Based on our estimates, either property could fetch c.S$430-480m. Assuming an asset sale of either of these 2 properties at book value with proceeds used for debt repayment, this could result in an accretion of c.1.0%-1.1% (sale of JEM Tower that is on tight cap rates of 3.5%) or a dilution of up to 6% for Sky Complex. In both instances, gearing could fall to a conservative c.32%. These initiatives, if executed upon, would preserve investors’ capital in the REIT.

My thoughts?

From a logical perspective, I am inclined to agree with DBS bank.

To do an equity fundraise in this market would be hugely dilutive, and incredibly unpopular with unitholders.

That would ruin the Lendlease track record for years to come, among local investors.

Logically it makes no sense.

If you want to buy Parkway, you wait until 2-3 years later when interest rates go down and the macro stabilises.

If you try to buy Parkway today you likely need shareholder approval given the size, and no guarantees you get it given how upset unitholders will (likely) be.

But… what am I missing?

But in investing I always try to look at how I may be wrong in my analysis.

And when I look at Lendlease REIT’s share price below – and the huge decline after going ex-dividend.

I can’t help but shake the feeling that the market (or insiders) knows something I don’t?

When a stock moves this much this fast, it usually suggests something deeper.

Is there someone in the pipeline for Lendlease REIT that is hitting the share price this hard?

If so, I don’t know what I don’t know here.

So… Will I buy Lendlease REIT?

Full disclosure that I hold a position in Lendlease REIT.

And from a fundamental perspective everything checks out.

Valuations are dirt cheap, rental reversions are strong, retail portfolio is almost best in class.

There are no doubt financing issues, but can probably be managed until early 2025, by which time the interest rate climate should be quite different.

Here’s great summary from DBS, on the fundamental bull case for Lendlease REIT.

Attractive returns for an emerging suburban landlord. Lendlease Global Commercial REIT (“LREIT”) has underperformed its retail focused S-REIT peers lately, with its share price weakening by close to 15% while its peers have declined only around 3%. This is despite the REIT’s strategic pivot to Singapore (now c.88% of assets) for which we remain comfortable that asset values (retail) will remain sticky. LREIT trades at a FY24F yield of c.8.2% and P/B of c.0.7x, at -1 standard deviation of its historical mean, and implies expectations of a significant cut in DPUs.

Steady organic growth, recent acquisition of Parkway Parade will contribute in FY24-25F. We forecast LREIT’s EBITDA to grow at a CAGR of c.7% in FY23-25F, driven by further rental reversion upside for its key assets – 313@Somerset and JEM. We expect these properties to see positive rental reversions of 5-15% in coming years, underpinned by strong tenant sales exceeding pre-Covid levels by 15%. In addition, LREIT will see a boost from (i) acquisition of a 10% stake in Parkway Parade, and (ii) rental escalations from Sky Complex.

Asset sale rather than an equity fund raising at this price. Contrary to market speculation, we think management is unlikely to pursue equity fund raising (“EFR”) at 0.7x P/B, given its stable financial metrics and strong lender support, implying pressure to reduce gearing is lower than market’s perception. Instead, our preferred scenario is an asset sale of JEM Tower of Sky Complex, Milan. Selling these could reduce gearing to c.32% with minimal DPU dilution.

BUY, TP maintained at S$0.90. Our TP is based on DCF and implies upside of >50%. We believe the recent sell-off is unwarranted and we see significant value emerging, with concerns over LREIT’s balance sheet overblown.

For the record, I agree with all the points DBS raised, and they’re very similar to my personal views on Lendlease REIT.

But in investing – you want to respect the price action.

When a stock moves this much this fast, it usually suggests something deeper.

And here my fear is that the market / insiders know something I don’t (for eg. a big upcoming equity fundraise, or other hidden problems).

Because of that, I want to give it some time for any potential news to flush out before making any decisions.

I don’t want to make any decisions on Lendlease REIT until any such potential news comes out, or the price action stabilises.

As always, Patreons will get updates as and when I change my mind and add to my Lendlease REIT position (or sell it entirely).

Closing Thoughts: Lots of opportunity for single stock (or REIT) pickers

I also just want to add that there are a lot of other attractive REITs out there right now for stock pickers, all at 7 – 9% yields.

But this interest rate cycle hasn’t turned fully yet, so you want to be quite careful when picking as not all REITs may survive this cycle unscathed.

I would focus on REITs with a strong asset portfolio, a stable sponsor, and ideally a strong balance sheet.

Patreons have access to my full REIT and Stock watchlist, on the names I am looking at.

This article was written on 15 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

WeBull Account – Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH,

Just want to add, OUE is even cheaper. Their book value is 0.36.

Sponsor is the Lippo group though. You need to be comfortable with that if you are investing in OUE CREIT.

Maybe investors fear this becomes the next MUST?

The property portfolio is pretty solid though. JEMs & 313.

And sounds like DBS got answers for every likely risk.

Possible – but the asset portfolio is completely diff vs MUST though.

Yes, but this is sell-side research so take it with a pinch of salt. For what it’s worth though, I actually agree with DBS from a fundamental perspective. It’s the funky price action that troubles me, and I’ve learnt the hard way not to ignore price action when it moves like this. Whatever the case, we’ll find out soon enough.

I believe this is as buffet as you can get.

Where the fundamentals check out, but the pricing looks suspicious.

Anyway risk reward makes sense. I’m going in.

Hi FH

Do you have any general impression of Lendlease group as their sponsor? From what i see, their price seems quite choppy over the last few years and they made a loss in their most recent earnings report. Basically what im asking is, should i be concerned about their long term prospects as a sponsor?

That’s a good question.

Lendlease definitely isn’t in the same level as CapitaLand/Mapletree/Frasers.

Lendlease’s track record in SG is only 4 years (since IPO in 2019), and during this time the track record hasn’t been amazing. Although not as bad as some other sponsors out there (not naming names).

I would say Lendlease isn’t best in class sponsor, but also not on my list of sponsors to actively avoid. Somewhere in between, and definitely a point to watch.

Noted and thanks for taking the time to reply! Im a huge fan of your weekly articles.