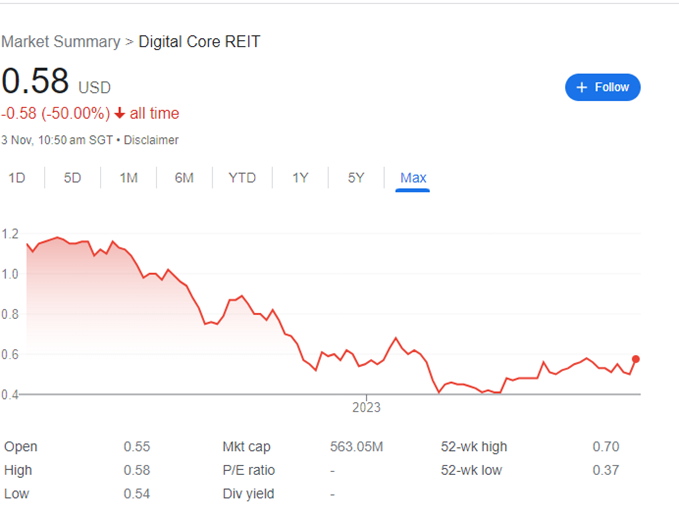

Digital Core REIT hasn’t had the best year.

On top of dealing with rising interest rates, it also had to deal with the bankruptcy of its 2nd largest customer:

Digital Core REIT’s tenancy woes

Digital Core’s second-largest customer, Cyxtera, a global colocation and interconnection provider representing approximately $16.3 million, or 22.4% of Digital Core REIT’s annualised rental revenue, filed for chapter 11 bankruptcy protection.

During this time, Cyxtera continued to be prompt in meeting their rental obligations to Digital Core. However, investors were concerned that due to the current oversupply in the market, should Cyxtera not be able to make payments, Digital Core would have difficulties backfilling the space that Cyxtera leased.

Even though Digital Core explained that Cyxtera’s in place rent were below market and market conditions were tight with low vacancy rates, with the risk crystallising and no resolution being provided by the management, coupled with a high interest rate environment, investors were fearful and sold down the REIT.

Digital Core REIT’s poor performance

The data centre REIT also reported lacklustre 1H23 results.

Operationally, Digital Core REIT was doing okay. Its Revenue and NPI were both stable with occupancy maintained at 97%.

However, its DPU fell 12.7% vs its forecast and 6.8% YoY. This was mainly due to financing cost as the weighted average cost of debt was approximately 4.4% while the weighted average debt maturity was approximately 3.4 years with approximately 72% of total interest rate exposure hedged as at 1H23.

Investors lost confidence and a selloff occurred in March 2023:

Digital Core REIT’s share buyback

As the share price was trading below NAV and was yielding more than 7.5%, Digital Core took the opportunity to repurchase 4.6 million units at an average price of $0.462.

With this move, the management delivered 0.4% DPU accretion while preserving balance sheet flexibility with aggregate leverage at about 34%.

Making a few big moves in one go

On top of its share buyback, Digital Core’s share price reacted positively to the slew of announcements, increasing 10% after it resumed trading.

Digital Core resolved its overhang, carried out accretive capital recycling and diversified its portfolio through acquisitions.

1) Resolving its overhang

Digital Core was able to resolve its Cyxtera bankruptcy overhang in part due to Brookfield’s acquisition of Cyxtera. Brookfield is a global asset management firm who acquired most of Cyxtera’s asset with the intention of merging it with their other colocation provider.

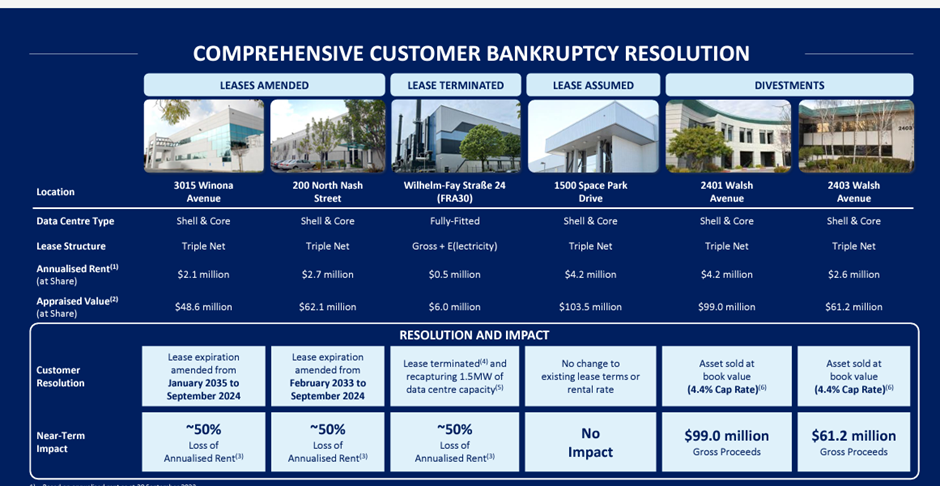

Amendment of leases

Two leases were assigned from Cyxtera to Brookfield as part of the sale of its business in bankruptcy.

The lease expiration was amended from January 2035 to September 2024. Upon expiration of the amended lease agreements in September 2024, Digital Core expects to enter into direct agreements with the end-user colocation customers currently occupying the facilities and expects to enhance the return on these facilities over time by leveraging Digital Realty’s (its sponsor’s) global platform to gain efficiencies, lease up existing vacancy, and invest prudently to enhance marketability and build out additional capacity.

Termination of lease

Digital Core REIT owns a 25% interest and its sponsor Digital Realty owns the remaining 75% interest in its Frankfurt asset, where the customer leases approximately 4% of the facility.

Digital Core REIT and Digital Realty have agreed to pay US$10 million, of which Digital Core REIT’s 25% share will be US$2.5 million, to terminate the customer’s lease agreement as part of the broader transaction under which Brookfield is acquiring the Cyxtera’s business out of bankruptcy.

Digital Core REIT and Digital Realty expect to create long-term value by re-leasing this capacity at more favourable terms.

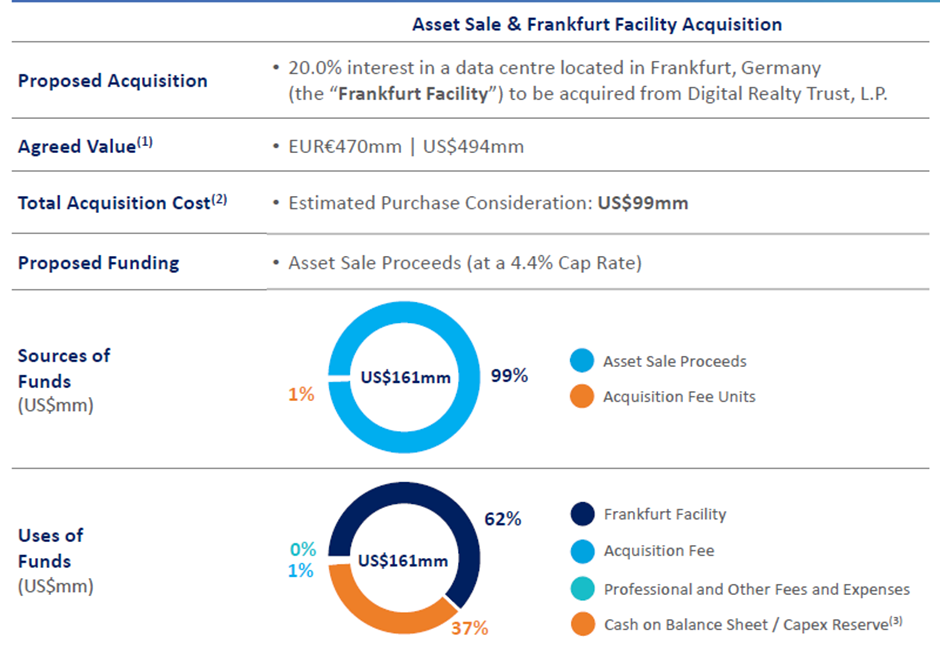

2) Accretive capital recycling

Digital Core is selling two of the three Silicon Valley facilities to Brookfield for US$178 million. Digital Core REIT owns a 90% interest in both assets and the transaction values Digital Core REIT’s 90% interest at US$160 million, in line with current book value. Based on the REIT’s 2024 contractual cash net operating income, the transaction represents a 4.4% cap rate.

In this current market environment, it is fortunate for Digital Core to be able to sell an asset with a distressed tenant base at current book value. At the same time, it also benefits Brookfield who can own the asset that Cyxtera previously utilised as part of its flexible

3) Diversification through acquisition

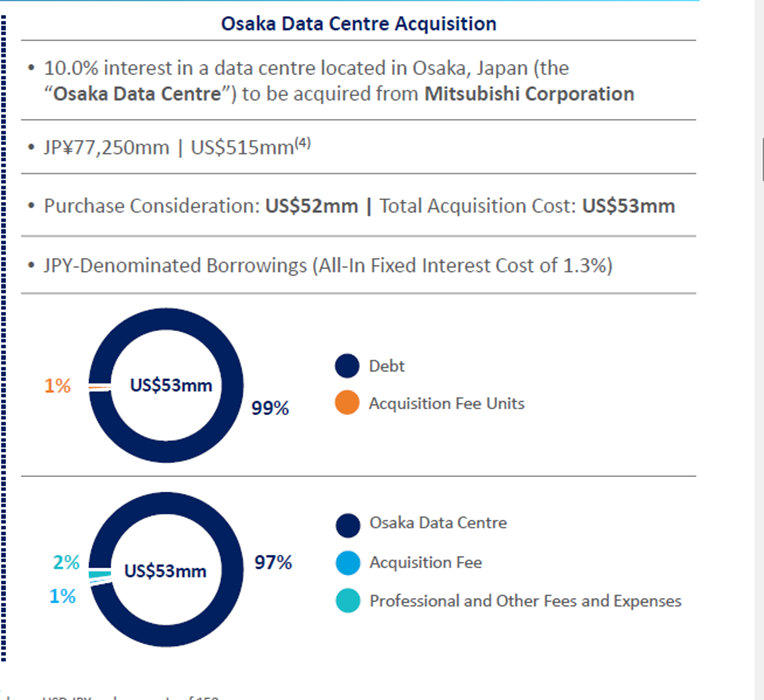

Acquisition of a Data centre in Japan

Digital Core is acquiring 10% interest in a freehold facility located in Osaka from Mitsubishi Corporation for approximately US$51.5 million.

The transaction will establish Digital Core’s presence in Japan, improve geographic diversification and achieve international expansion, while also enhancing portfolio quality with the addition of an investment in a robust data centre market.

Digital Core REIT expects to fund the transaction with Japanese Yen-denominated borrowings and has entered into a swap agreement to fix the rate on a portion of the borrowings for a three-year term at an all-in borrowing cost of 1.3%.

Not only is the yen at a favourable level now, Japan is also in an expansionary interest rate environment and hence the costs of debt is much lower as compared to the US.

Increased stake in Frankfurt asset

Digital Core will also acquire an additional 20% interest in its Frankfurt asset, from Digital Realty for approximately US$99 million.

The transaction is expected to further improve geographic and customer diversification while enhancing overall credit quality. This is a sign of Sponsor support providing a suitable pipeline of acquisition to strengthen the REIT’s portfolio when necessary.

Is Digital Core REIT finally out of trouble?

The actions to resolve the exposure to Cyxtera have significantly reduced Digital Core’s revenue exposure to Cyxtera from 22% down to 5%.

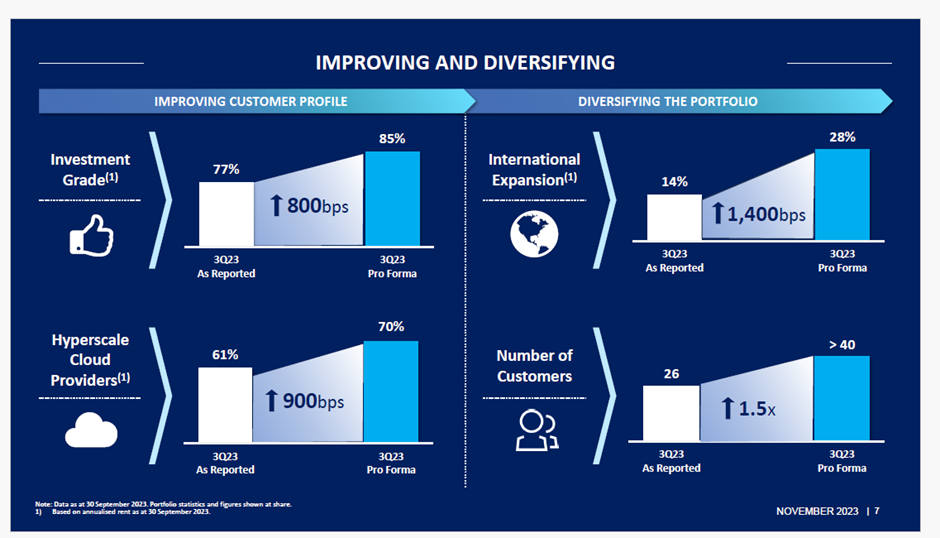

The acquisitions made have improve Digital Core’s customer profile, increasing the percentage of investment grade customers from 77% to 85% and hyperscale cloud providers from 61% to 70%.

The acquisitions will also increase the percentage of annualised rental revenue generated outside North America from 14% to 28%. The REIT’s portfolio of customers also increases from 26 to 40.

Digital Core provided an adjusted projection of its FY22 DPU based on FY23’s interest rate and operating expense environment and explained that based on current conditions, FY22’s DPU would have been 3.50 cents instead of the actual 3.98 cents, a 12% decline.

Additionally, any further impact arising from Cyxtera’s bankruptcy would further pull down FY23’s DPU.

With the actions taken to mitigate impact from Cyxtera, coupled with the acquisitions and disposals, Digital Core REIT’s pro forma DPU, would be 3.50 U.S. cents, in line with its previous expectations.

NAV would be $0.82 compared to the reported NAV of $0.832 while leverage would be 34.1% compared to reported aggregate leverage of 34.0% after the disposal of the 2 Silicon Valley assets raised $160 million in gross proceeds to fund $151 of acquisitions comprising the acquisition of the 10% stake in the Japan data centre at $52 million and the 20% stake in the Frankfurt data centre at $99 million.

We think Digital Core is looking ok now.

It is worth acknowledging that Digital Core’s management has done well, substantially removing the overhang in one fell swoop and improving its portfolio profile.