Okay let’s not mince words.

This month’s December Singapore Savings Bonds are probably the best SSBs – in the history of SSBs.

And with the sharp drop in 10 year interest rates since late October.

It is very likely that next month’s SSBs won’t be as good.

So if you’ve been meaning to buy some Singapore Savings Bonds.

This is as good a time as it gets.

3 questions I wanted to address in today’s article:

- Are Singapore Savings Bonds a good buy?

- Will next month’s Singapore Savings Bonds have higher yields? What about 2024?

- How much SSBs will you get allotted?

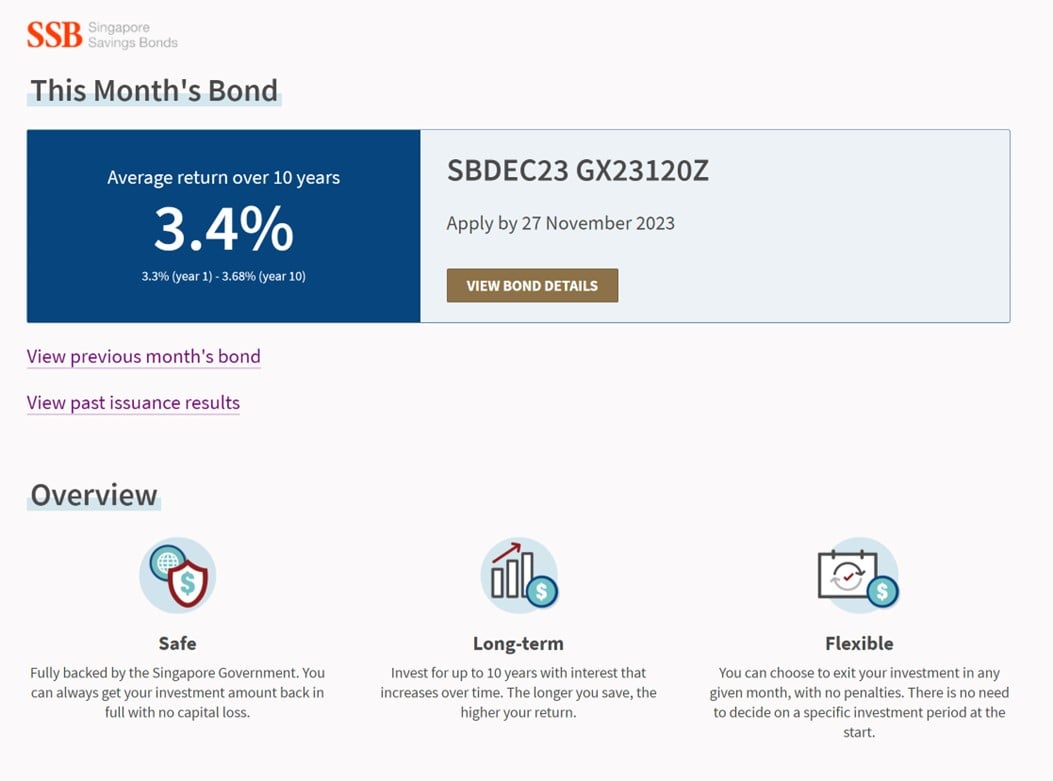

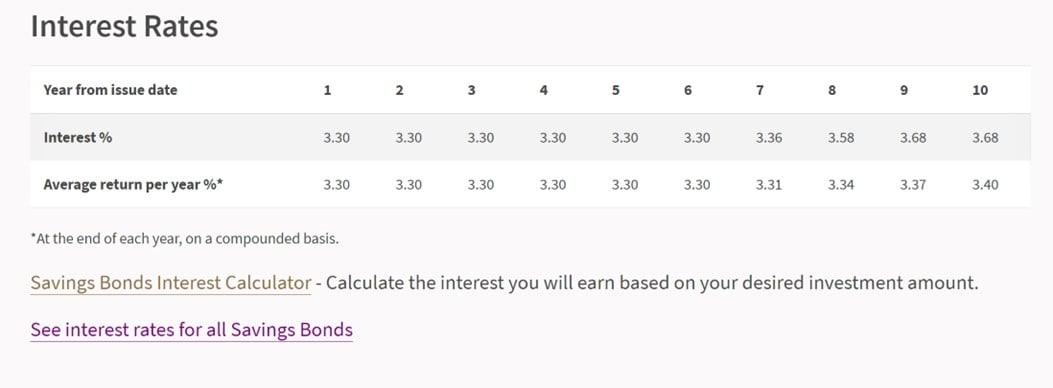

Are Singapore Savings Bonds a good buy? – Singapore Savings Bonds pay up to 3.68% yield

Yields on the latest Singapore Savings Bonds below.

You’re getting:

- 3.30% for the first 6 years

- Stepping up to as high as 3.68% for the 10th year

And an average yield of 3.40% over 10 years.

3.4% risk free on Singapore Savings Bonds for 10 years is pretty nuts…

I can’t stress how crazy it is that you can get 3.4% risk free on a 10 year Singapore Savings Bond that can be redeemed any time (with no risk of loss).

For reference, I just asked to reprice my mortgage this week and the bank offered 2.95% fixed.

This means that I can literally just park my cash in Singapore Savings Bonds at 3.4% and earn the 0.45% carry for the duration of the mortgage, without worrying about refinancing risk with T-Bills.

Crazy times, that I encourage investors to take advantage of.

Is this the best Singapore Savings Bonds of all time?

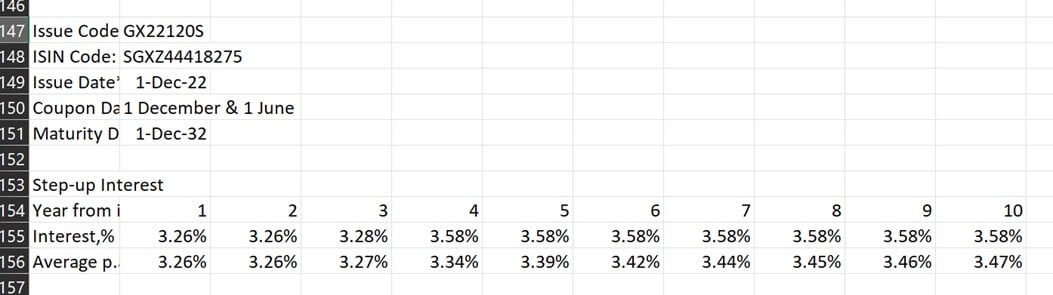

Just FYI – this is the next best Singapore Savings Bonds of all time (December 2022).

It’s debateable which is better.

The Dec 2022 SSBs have a lower 1 – 3 year interest rate (3.26%), but a higher 10 year interest rate.

Whatever the case, the Dec 2022 SSBs only saw $14,000 allotment.

This is the next opportunity if you missed out in 2022.

Next month’s Singapore Savings Bonds will have lower yields?

Singapore Savings Bonds tracks the 10 year yield of the Singapore Government Bond (average for the previous month).

However, the interest rate curve is smoothed out – so that the 1st year interest rate will never be higher than the 2nd or 3rd year interest rate.

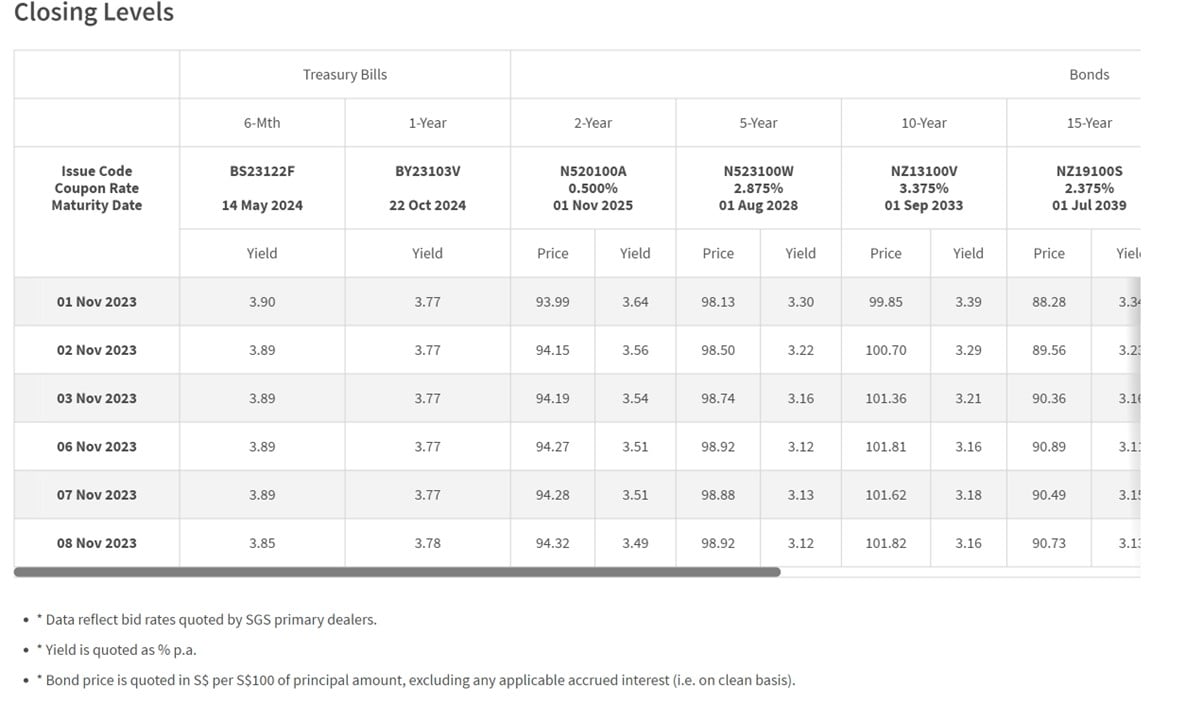

This is a big problem right now where the 1 year yield (3.78%) is higher than the 10 year yield (3.16%).

So long story short – the key factor that determines how attractive the yields on the Singapore Savings Bonds is the 10 year interest rate.

And since late October.

10 year interest rates have plunged.

From 3.5% a few weeks back, to 3.1% this week:

Why did 10 year interest rates plunge?

I wrote a full article on Patreon to explain this dynamic.

Essentially – the US Treasury announced in late October that they would be issuing less long-term debt than the market was expecting, and shifting that issuance to short term debt.

Much of the rise in long term interest rates of late was due to market fears over too much Treasury supply.

With that risk out of the way, and with jobs data showing a slowdown in the labour market.

US 10 year interest rates plunged from 5% to 4.5%:

So… next month’s Singapore Savings Bonds won’t have such high yields?

All this is just a fancy way saying:

That unless something material changes that causes the Singapore 10 year yield to jump in the next 2 -3 weeks, next month’s Singapore Savings Bonds *probably* will have lower yields than this month.

So if you were on the fence and not sure whether to wait for higher yields before buying SSBs.

This might seal the deal for you.

Will Singapore Savings Bonds have even higher yields in 2024? Or is this the highest yields this cycle?

I suppose the next question – will SSB yields go even higher in 2024?

Now in 2022 I was fairly confident in calling that 2022 was NOT the peak in interest rates.

To me the economy was too strong, and inflation too sticky, that the economic cycle had more time to play out.

And that higher interest rates lay in 2023.

But ask me the same question today, and I think it’s just a complete sea change.

Today, I think the risks for economic growth (and interest rates) are tilted to the downside in 2024.

So will SSB yields will go even higher in 2024?

I mean it’s not impossible, but I’m not going to hold my breath on this one.

Why take the risk? Bird in hand and all…

But why take the risk?

Yes, maybe Singapore Savings Bonds yields go even higher in 2024.

But Singapore Savings Bonds can be redeemed any time, with no risk of capital loss.

Worst case if yields go higher next year, you can just redeem them and buy next year.

And you know that this month’s SSBs are some of the best in the history of SSBs.

Why not just buy now to get your allotment, and decide what to do with it later?

Opportunity cost of buying Singapore Savings Bonds vs T-Bills?

The only “opportunity cost” is the lower short term yields.

But Singapore Savings Bonds yield 3.3% first year, and latest 6-month T-Bills yield 3.75%.

That’s a spread of only 0.45%, the lowest it has been all cycle.

What are the alternatives out there – for investors looking for yield?

Let’s sum up the alternatives out there right now:

|

Instrument |

Risk Level |

Yield |

|

6-month T-Bills |

No risk |

3.75% |

|

10 year Singapore Bond |

No risk |

3.17% |

|

REITs (CICT or Ascendas REIT) |

Low – Medium |

5.8% |

|

US 2 year T-Bills |

No risk (USD FX risk) |

4.97% |

|

US 10 year Treasuries |

No risk (USD FX risk) |

4.58% |

Now Items 3 – 5 are a bit more complex because they carry risk of capital loss if you don’t know what you’re doing.

The main comparison is vs Items 1 and 2.

Singapore Savings Bonds compared vs T-Bills?

The main risk 6-month T-Bills carry is refinancing risk.

Yes the 3.75% yield is higher than SSBs at 3.3% – but you really don’t know where interest rates will be in 6 – 12 months time.

This is huge, and I think investors are underestimating this.

It’s only a 0.45% spread, and you lock in yields for up to 10 years, and remove all the refinancing risk.

Given how risks to economic growth and interest rates are tilted to the downside the next 12 months.

I think it’s at least worth considering moving some cash into Singapore Savings Bonds.

Singapore Savings Bonds compared vs 10 year SGS Bonds?

The main risk 10 year SGS Bonds carry – is the fact that these bonds only mature 10 years later.

10 years is a very long time.

If you decide you want the money before 10 years, the only way out is to sell the bonds on the open market.

Where the price depends on where interest rates are.

I would say 10 year SGS Bonds are good if you want to make a bet on interest rates going down.

But if you are just looking to collect the yield it’s more tricky because your exit price is intrinsically tied to where interest rates are.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Singapore Savings Bonds lock in decent yield for 10 years, with no risk of capital loss

So the Singapore Savings Bonds is kind of a cash-bond hybrid.

A bond in that it allows you to lock in decent interest rates for the next 10 years.

But also cash in that (unlike long duration bonds), there is zero risk of capital loss even if you exit before maturity.

If interest rates go up, you can just redeem the SSBs any time and get your full principal back with no accrued interest.

For investors who want to lock in yields, and don’t want to bet on interest rate movements, I think SSBs are a good option.

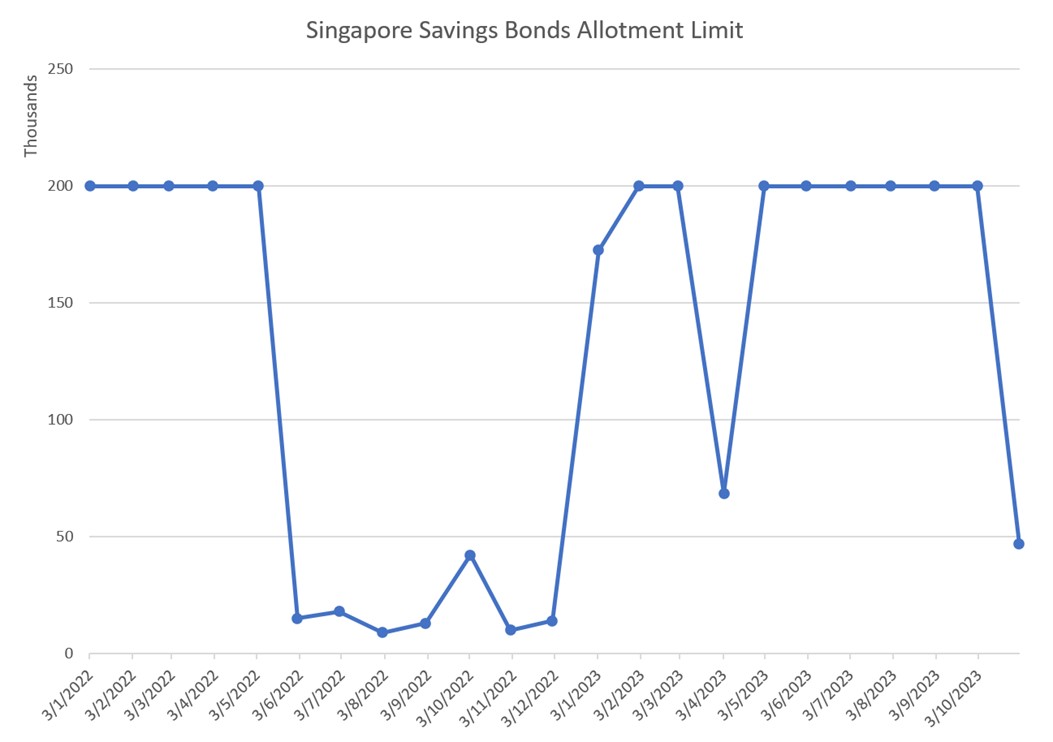

Will you get full allotment for SSBs?

The final point to think about is allotment.

In 2H 2022, demand for SSBs was very hot, and you were looking at only $10,000 – $15,000 allotment.

In the most recent auction, SSBs were very hot again – and only saw $47,000 allotment.

Will Singapore Savings Bonds Allotment Limit drop further the next auctions?

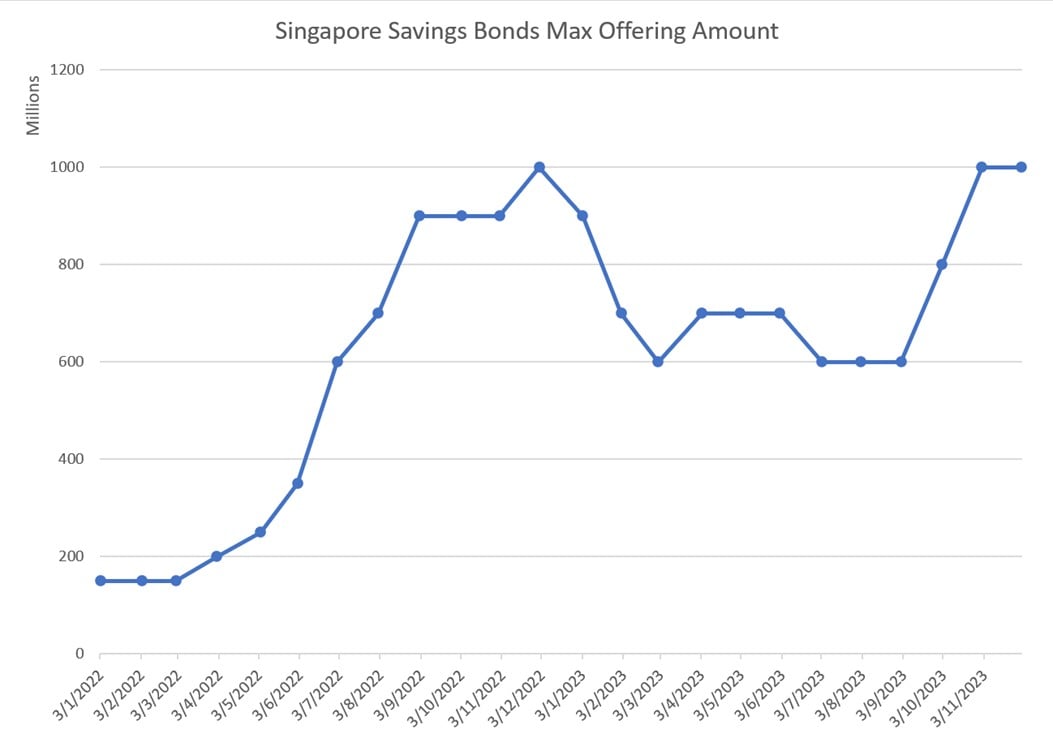

Looking at the numbers.

The amount of SSBs available for sale this month is $1 billion – no change from last month supply wise.

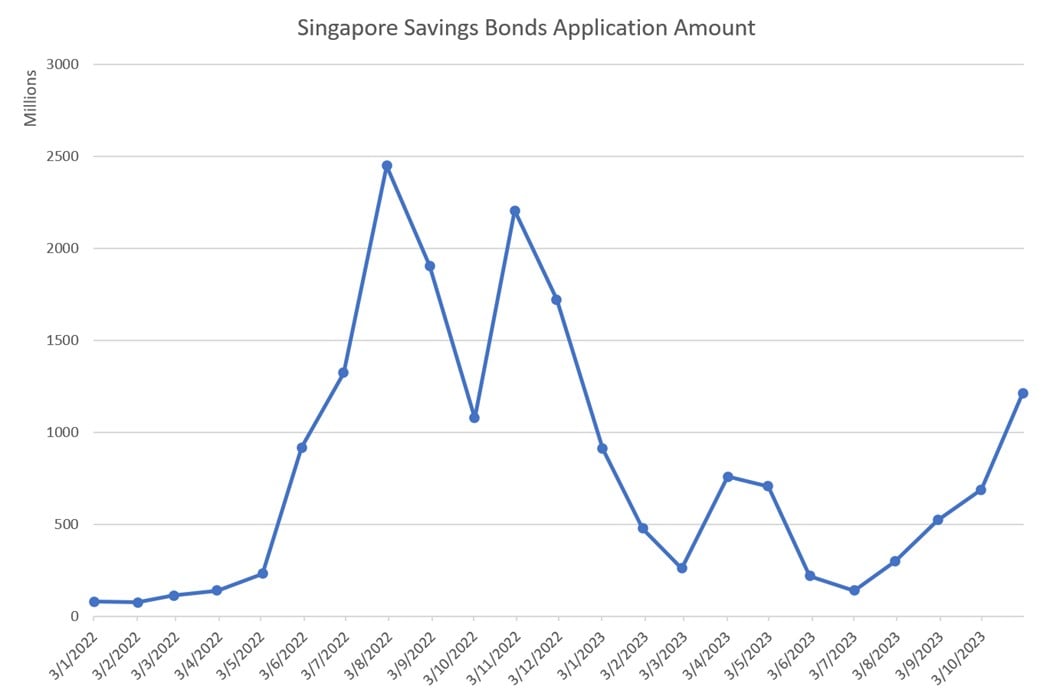

Demand has definitely gone up since the middle of the year.

But in the grander scheme of things – demand for SSBs is still well below 2022 highs.

In 2022 we saw as high as $2.4 billion demand, while for the most recent auctions we’re seeing $1.2 billion (this is a retail only product, so no institutional demand).

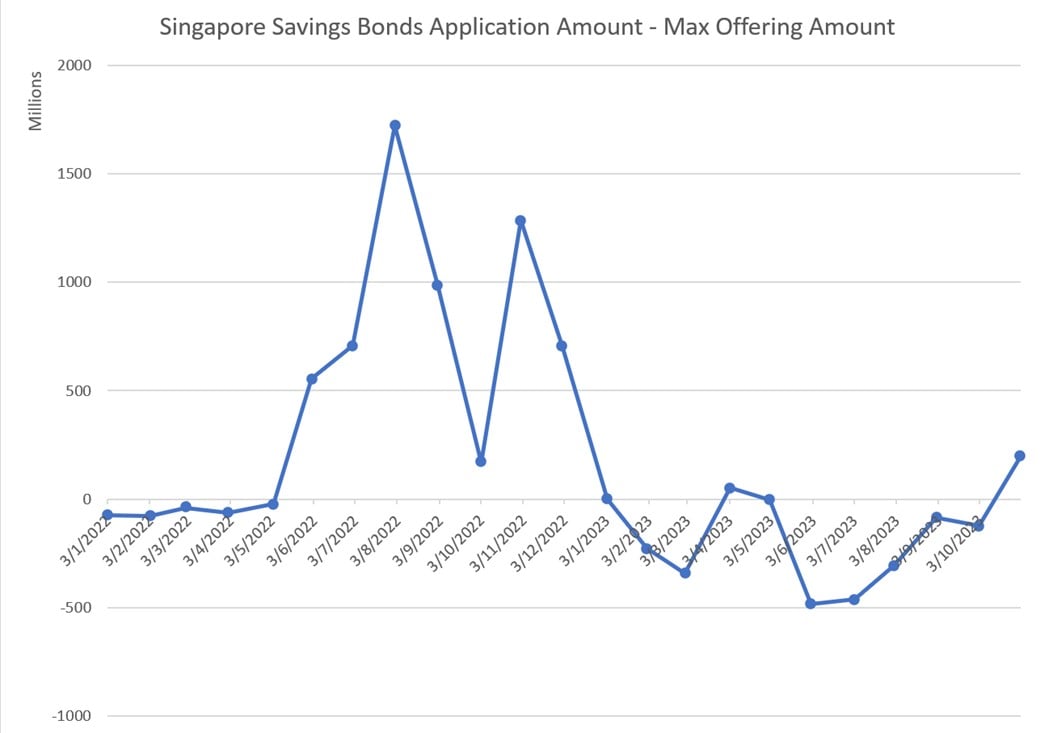

Here’s Singapore Savings Bonds application amount less the max offering amount.

This shows how much excess demand you have relative to the amount of SSBs available.

Despite the increase in demand of late, it is still much lower than 2022 highs, and only a slight excess.

I suppose investors have more options now than in 2022 – with T-Bills, Fixed Deposits, money market funds, savings accounts and so on.

So what allotment limits will we see for the December Singapore Savings Bonds?

Putting in altogether.

I think allotment limits are probably going to drop from November’s $47,000.

Especially given the higher yields, and the knowledge that next month’s SSBs won’t be as attractive.

Exactly how much lower is not so clear though.

What will I do – Apply for Singapore Savings Bonds or skip? How much will I apply for?

Given that this is arguably the best SSBs of all time, and possibly the best for this entire interest rate hiking cycle.

I’m definitely going to be applying for the Singapore Savings Bonds this month.

How much to apply is not so clear.

Given that allotment is likely lower than last month’s $47,000.

I’ll probably submit a bid for about $50,000 to $60,000 thereabouts.

Do note that each individual above 18 can apply for the $200,000 limit.

So if you’re married with 2 kids, that’s technically $800,000 per household.

Some of you have also asked me for the average yields on the SSBs I hold.

I just checked, and the lowest SSBs I hold today yield 3%+ in the first year.

So it seems that I have been quite diligent in refreshing my SSBs to higher yields.

But do note liquidity issues for Singapore Savings Bonds

Do note that the cash is deducted from your account when you apply for Singapore Savings Bonds.

So if you are redeeming existing SSBs to buy new one, you must have the cash in your account to buy the new SSBs (as the cash from the existing SSBs won’t be in until the next month).

You also lose the “interest” on the cash the moment it is deducted.

This could be a factor to think about.

Such that if it’s clear you won’t get $200,000 allotment, there may not be a need to submit a $200,000 bid.

And submit as close to the deadline as you can, otherwise you lose the “interest” on the cash once it is deducted.

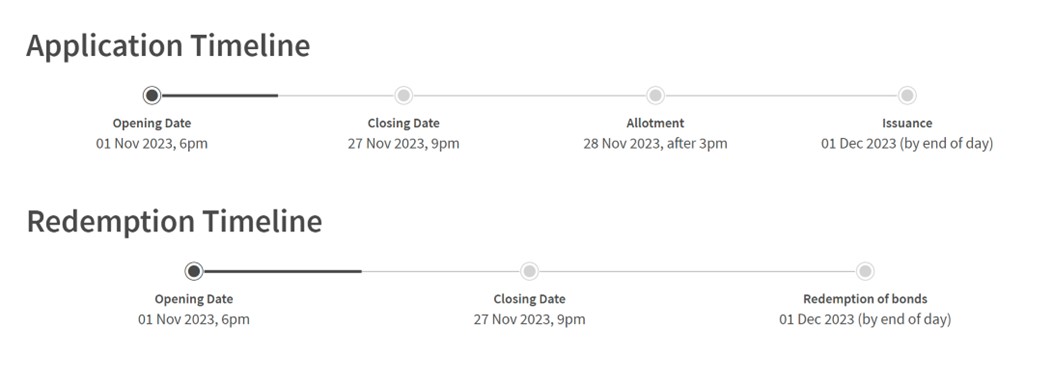

Singapore Savings Bonds Application Timeline (27 Nov 2023)

If you’re interested to apply for the Singapore Savings Bonds.

Application deadline is 9pm on Monday, 27 Nov 2023.

Same timing for both applications and redemptions of Singapore Savings Bonds.

Love to hear what you think – are you applying for this round of SSBs?

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Dunno whether you’re able to shed some light on your refinancing decision. Fixed or floating going forward?

Looking at the 2Y fixed with option to reprice after 1Y. Will try to do an article to share my fuller thought process.

Hi – can share what bank and loan amount for 2.95% fixed? Still getting quotes around mid 3% these days.

I’ll try to write an article on this to share my fuller thought process, as some others have asked as well. Will try to get it out soon.

You can try to speak to a mortgage broker as well, they will help you to find the cheapest mortgage based on your mortgage details.

Hi FH,

Can i check with you if submit 2 applications – Cash and SRS, what would be allocation be like? What would be your preference for investing SRS funds? Thank you

The allocation is on a per person basis. So there is no double dip.

SRS funds depends on your age. If you are 30 your SRS funds are locked up for a very long time, so I would invest for long term capital gains.

If you are close to retirement, then just parking SRS funds in a risk free asset like SSBs while earning the tax benefits could be a no brainer.