Singapore’s property market has risen 30% in 5 years, dodging the downturns seen in other major cities, prompting major curbs such as the raising of stamp duty rates to cool the overheated market.

Singapore Citizens buying their second residential property now have to pay an additional buyer stamp duty (ABSD) of 20% of the selling price in taxes. Foreigners have to pay 60% in ABSD, doubled from 30% previously making Singapore the highest globally for stamp duty on foreigners.

In contrast, cities such as Hong Kong has slashed housing taxes in order to revive its ailing property sector.

Despite the increased taxes, residential prices including prime residentials in Singapore have remained strong, supported by a robust domestic market and an inflow of high-net-worth individuals setting up companies and family offices.

The strong Singapore dollar acts as a testament to Singapore’s attractiveness as a safe haven for investments for everyone, including the ultra-high-net worth individuals and further attracts overseas fund flow into Singapore’s property market.

Views from one bank

Morgan Stanley, a US investment bank is calling time on an unprecedented real estate boom in Singapore after home prices rose more than expected in 3Q23.

The bank says that based on their analysis of leading indicators including housing vacancies and sales, home prices will likely decline 3% in 2024, and the downturn may persist for as many as two years.

Higher borrowing costs, higher stamp duties deterring investors and foreign buyers will cause housing demand to decline. It is expected that fewer people will upgrade from public housing and investors will pull back.

At the same time, the Urban Redevelopment Authority of Singapore is putting up more land for sale than they have in a decade.

What does the data say?

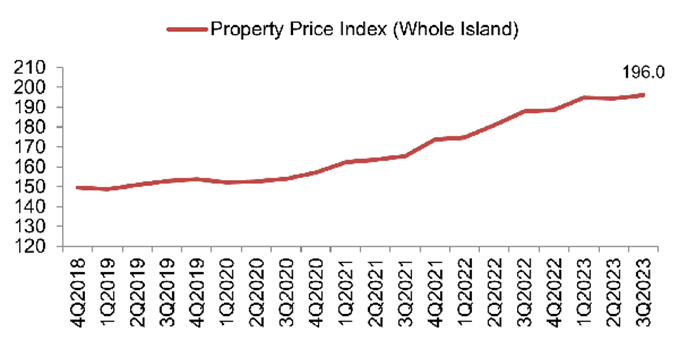

Property prices

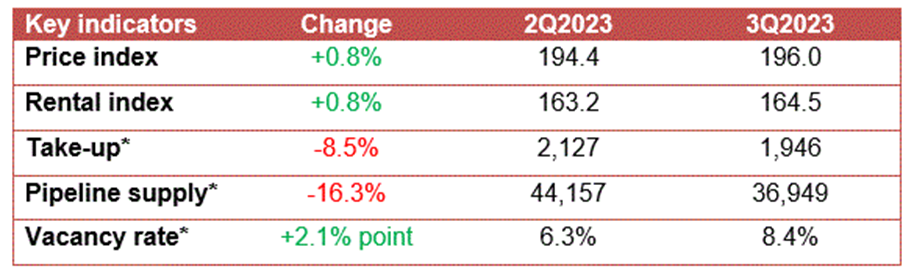

Based on the price index, overall private housing prices increased marginally by 0.8% in 3Q23, following a 0.2% decline 2Q23.

Rental market

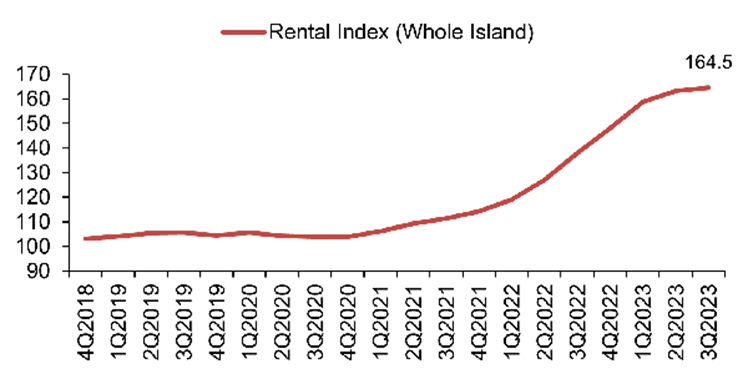

Private residential property rentals rose at a slower pace of 0.8% in 3Q23, compared to the 2.8% increase in 2Q23. For the fourth consecutive quarter, the increase in rental moderated, and this was the smallest quarter-on-quarter gain since 4Q20.

Rentals of non-landed properties slowed to 0.2% in 3Q23, from the 2.3% increase in 2Q23.

Rental momentum eased across all market segments.

Rentals of non-landed properties in CCR decreased by 1.7% in 3Q23, compared with the 2.0% increase in 2Q23.

Rentals in RCR increased by 1.9% in 3Q23, compared with the 2.0% increase in 2Q23.

The increase in rentals in OCR moderated to 1.3% in 3Q23, compared with the 2.9% increase in 2Q23.

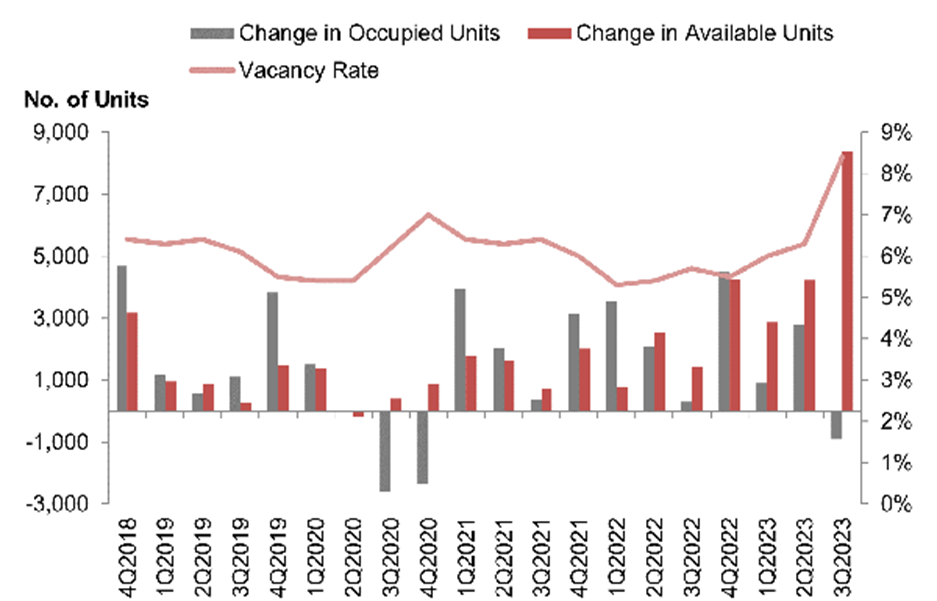

Increased inventory and vacancy

The vacancy rate of completed private residential units (excluding ECs) increased to 8.4% as at 3Q23, from 6.3% in 2Q23 due to a combination of an increased inventory of completed units as well as lower number of occupied units.

Slow and steady wins the race?

The Singapore government has had a consistent stance, wanting a sustainable property market that is not subjected to severe bubbles or crashes as well as affordable housing for the masses.

To meet this goal, the government has taken measures to tighten and relax policies as and when required in a bid to shape and control property prices.

Because of these measures, some have taken the view that the current prices are from a fundamentally driven market, that prices are robust and that the current levels are not due to speculation or irrational demand.

Despite these cooling measures, property prices have been on a strong upward trajectory, increasing by 30% over the last 5 years, leading to the current state of the market. Many are calling for the end of the bull market and some have even called for a crash.

What is needed for the next bull market to happen?

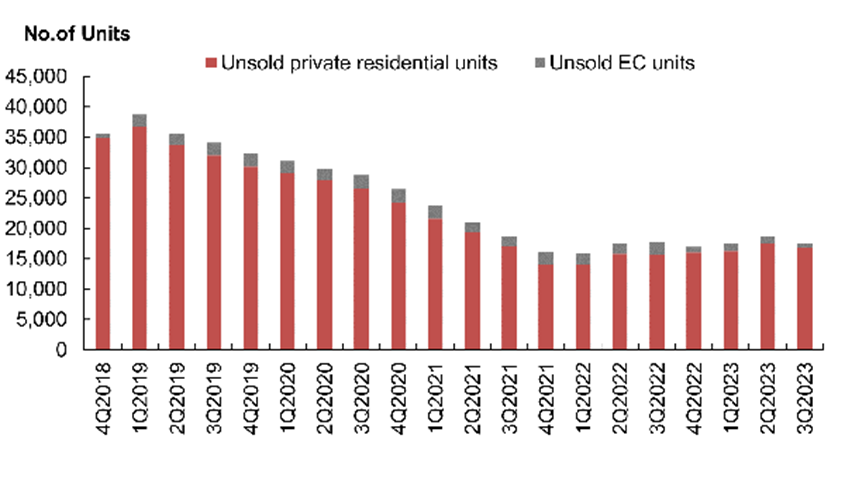

1) Low inventory and strong demand

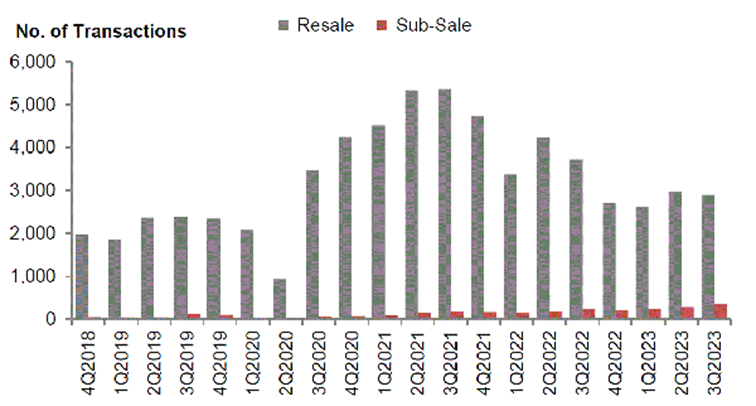

Current levels of inventory are quite low as compared to the recent 5 years as shown in the chart above. Looking at the chart below, transactions have also slowed as compared to the peak demand 2 years ago which fuelled the current bull run. There needs to be time for new demand to emerge.

2) Favourable Interest rate environment

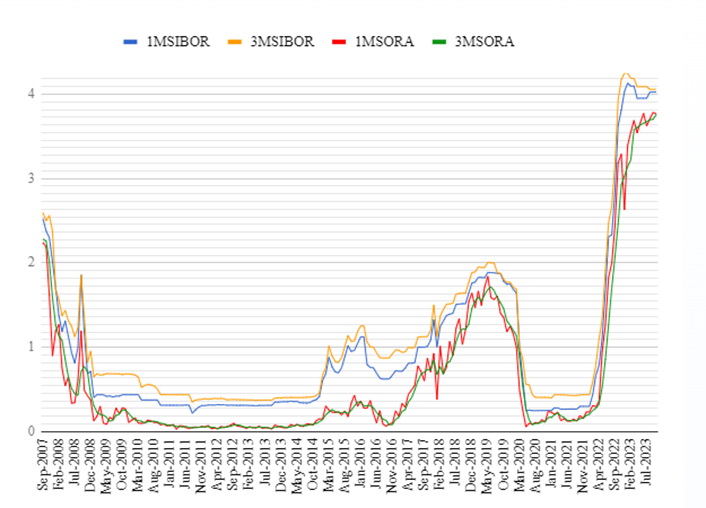

Looking at the interest rate chart which shows the interest rate from 2007 to date, it shows that we are at the highest interest rate in the last 16 years. As many investors take up loans amounting to 75% of property value, mortgages are highly sensitive to changes in interest rates.

3) Economic strength

MAS expects the global economy to grow 3.1% in 2023, down from 3.4% last year and slowing further to 2.8% growth in 2024.

For Singapore, full GDP growth for 2023 is expected to come in at the lower half of the official forecast range of 0.5% to 1.5%.

For 2024, there is still uncertainty over the strength and sustainability of the pick-up in growth, which is contingent on external final demand.

4) Policy changes

It has been years since the last time the Singapore government relaxed residential property measures. The government has shown that it will make calibrated adjustments to certain policies.

For example, in 2017 the government reduced the holding period for the seller’s stamp duty (SSD) as well as the SSD rates.

In 2022, due to higher market interest rates, the MAS raised the interest rate floor used to compute debt and mortgage servicing ratios. When interest rates eventually start to decrease, this will be the first policy that we think buyers should look out for as a catalyst.

Where is the property market really heading to?

The property cycle is much like any other cycle in that there will be an expansionary phase followed by a contractionary phase that repeats.

As we get closer to the peak, the expansion slows. Unfortunately, contractions do not start off gentle but sometimes the trough may be shallow.

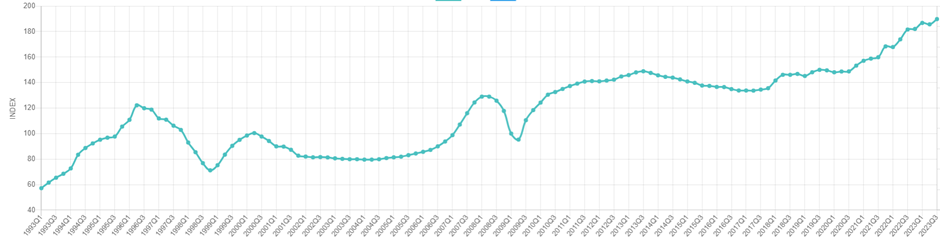

We think the government is getting better at managing price declines. Looking at the past 30 years, there has been 4 periods of substantial price decline. The most recent decline has been the mildest as shown in the table below.

| Peak (period) | Trough (period) | Peak (index) | Trough (index) | % decline |

| 2Q 1996 | 4Q 1998 | 122.2 | 72.2 | -40% |

| 2Q 2000 | 2Q 2004 | 100.4 | 79.6 | -21% |

| 2Q 2008 | 2Q 2009 | 129.0 | 95.3 | -26% |

| 3Q 2013 | 2Q 2017 | 148.9 | 133.7 | -10% |

It is not as easy to manage price increases in long periods of growth.

However as the vacancy rate is low, coupled with a high ABSD for foreigner and investors as well as a SSD penalising those who sell in less than 3 years, buyers are either purchasing for own stay or for a long holding period, which reduces speculation and volatility in the environment.

Will the Singapore Property Market crash?

As mentioned at the beginning of the article, Morgan Stanley thinks that we will see a 3% decline in 2024 and a downturn of two years. If this actually happens, comparing to the past peak to trough declines, we could just be facing a correction or a blip before a continuation of the bull run.

For the bull run to continue or a new bull run to form, we need to see as many of these factors as possible, namely low inventories, high demand, favourable interest rate environment, economic strength, and policy changes.