So a FH Premium member recently posed the question:

Hi FH,

I recall you did an article sometime ago on dividend stocks that are non-bank or reits.

Would be interesting if you could do a refresh. E.g. 100k in non-bank or reits or netlink.

Thanks

I am not a big fan of dividend stocks (excluding banks / Banks) at current valuations

Let me put it out there that I’m not a big fan of Singapore dividend stocks if you exclude the banks and REITs.

For the simple reason that I don’t think valuations are sufficiently attractive.

Looking forward into the next 12 months, there’s a good chance you’re going to see one of the following scenarios:

- Recession and Fed interest rate cuts

- Slower economic growth (but no collapse in growth) resulting in only minor Fed interest rate cuts

In Scenario 1 – earnings will be impacted, which means lower stock prices.

In Scenario 2 – interest rates will stay high for a while, which will weigh on stock prices.

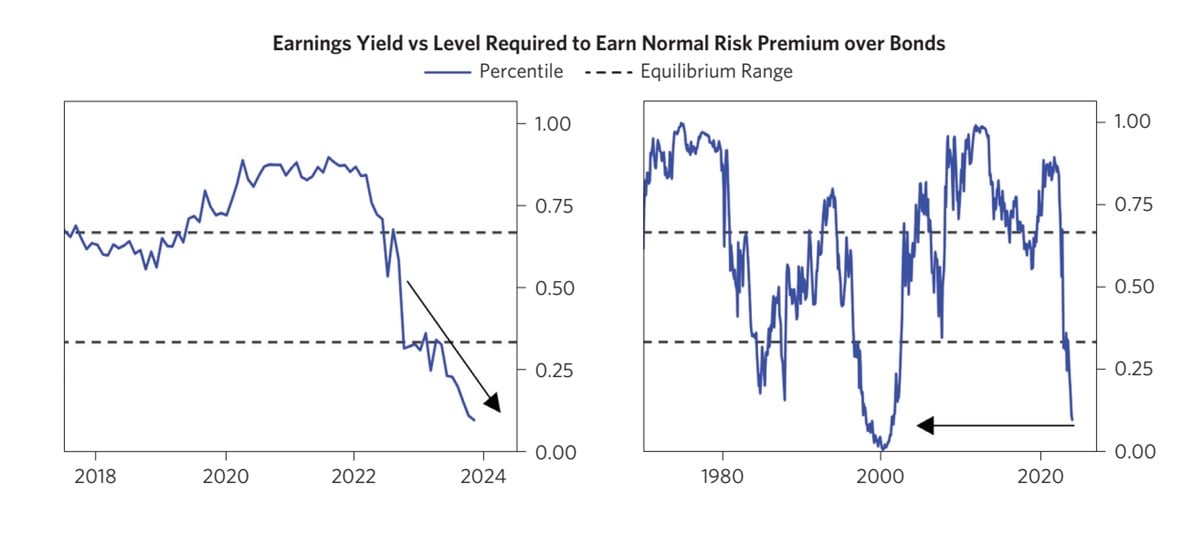

The chart below shows equity risk premium – basically how expensive stocks are relative to bonds.

By this metric, US stocks are the most “expensive” relative to bonds since 2000.

The last time US stocks were this expensive, they ended flat for the next decade.

Yes, this is US data, and yes, the analysis will change for different countries and different stocks and different industries.

But I just wanted to put it out there that most stocks are pricing in quite an optimistic 2024.

This means not a lot of upside if that (optimistic) future materialises, and potential downside if that future doesn’t materialise.

Top 3 Dividend Stocks to buy in 2024 – 5% dividend yield minimum

Back to the question at hand.

What are the top 3 dividend stocks I would buy in 2024, with the following rules:

- 5% dividend yield minimum

- No Banks, No REITs, No Netlink Trust

The fact that Netlink Trust was specifically named and excluded was pretty hilarious for me.

I guess this horse has been talking too much about a certain telecoms business trust.

But enough chatter – Top 3 Dividend Stocks I may buy in 2024, with a 5% dividend yield.

Keppel Corp – 5.1% dividend yield

Keppel Corp has done very well the past 2 years.

Since early 2022, Keppel Corp has soared almost 100% largely due to soaring energy (electricity) prices.

What I like about this dividend stock?

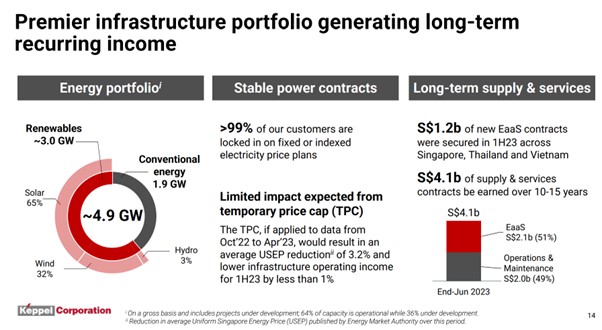

As one of the biggest electricity retailers in Singapore.

Keppel has benefitted well from the higher electricity prices.

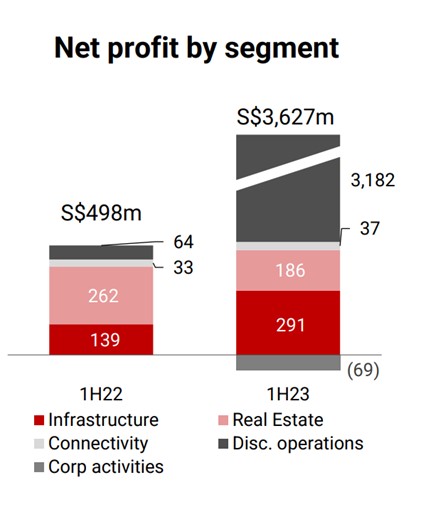

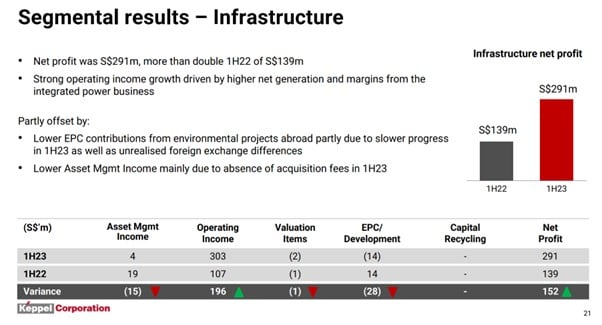

Net profit for the Infrastructure segment has close to doubled (from $139 million to $291 million).

Keppel (together with Sembcorp) is quite well positioned to benefit from the structural shift to green energy.

And if indeed this is a more inflationary decade, then Keppel with their infrastructure and energy portfolio is well placed to benefit.

Just like CapitaLand Investment, Keppel is also adopting an asset light strategy to become a fund manager / operating platform.

They want to manage and operate infrastructure / real estate assets, while collecting those juicy management fees (boosting return on equity).

At today’s price, you’re getting about 5.1% dividend yield (even higher if you include the one off distributions in specie of Keppel REIT and Sembcorp Marine)

So that’s the good stuff.

What worries me about this dividend stock?

That said.

Keppel’s earnings looks fantastic because of the big jump in electricity prices.

It’s hard to see the same jump in electricity prices going forward (near term, with inflation starting to moderate, and the government actively taking steps to reduce volatility in electricity prices.

If electricity prices start to dip going forward, then actually the performance from the other 2 segments has not been amazing.

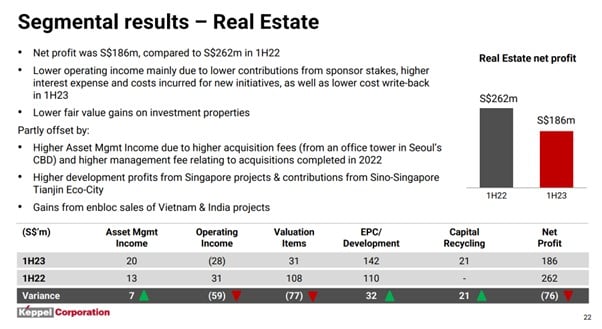

Here’s the real estate segment, net profit has dropped 30% from 2022.

And with high interest rates, and China’s deleveraging playing out, it doesn’t look like real estate will rebound so soon.

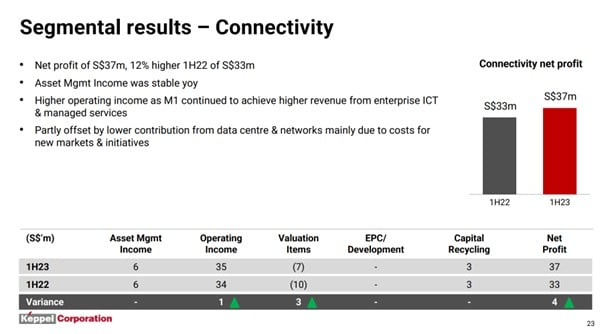

Here’s the connectivity (Telco) business.

Net profit is flattish, but at $37 million not really meaningful to the bottom line.

The 2 big heavy hitters are the infrastructure and real estate business.

DBS Research shares the same concerns as me, and I extract below:

Singapore Power business under the spotlight. Infrastructure segment, in particular the Integrated Power Operations, was the star performer in 1H23, offsetting the weakness in the Real Estate segment. There were concerns on the profitability of Singapore power earnings in 3Q23, in view of the decline in Uniform Singapore Energy Price (USEP, -35% y-o-y; -44% relative to 1H23 average) following government measures to reduce electricity price volatility.

Real Estate in China remains challenging though, we are seeing light at the end of tunnel. Home sales rose 55% y-o-y to 2,620 units in 9M23, driven largely by China and India, which both saw nearly doubling of home sales to 1,460 and 1,030 units respectively. It successfully sold two plot of lands at Tianjin Eco-city, one of which recorded S$14m profit in 1H23 and the other plot is expected to fetch a similar profit in 2H23.

Valuations wise I don’t think Keppel is super attractive given that cyclical risk is tilted to the downside here.

But I’ve been very impressed with some of the moves made by Keppel the past 2 – 3 years.

And this is definitely a dividend stock on my watchlist.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

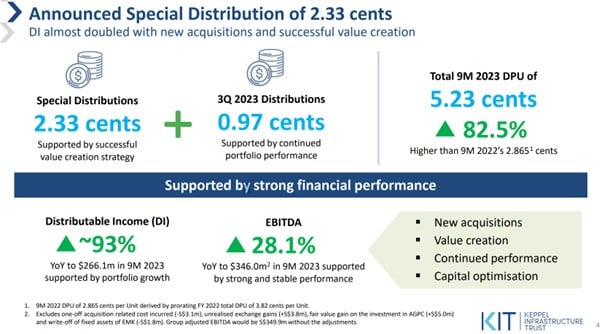

Keppel Infrastructure Trust – 8% dividend yield (excluding special distribution)

Yes, I know that Keppel Infrastructure Trust is not a “stock”, and technically a business trust.

But if you look at the operating assets held by KIT, this is much more of an operating entity than your usual REIT.

What I like about this dividend stock?

If you count the special distribution, you’re looking at a mind blowing 14.5% trailing dividend yield.

Dividend yield (excluding special distribution) is about 8%, not too shabby too.

I did a deep dive into Keppel Infrastructure Trust earlier this year, so do check it out if you are keen (full disclosure that I hold a position in KIT).

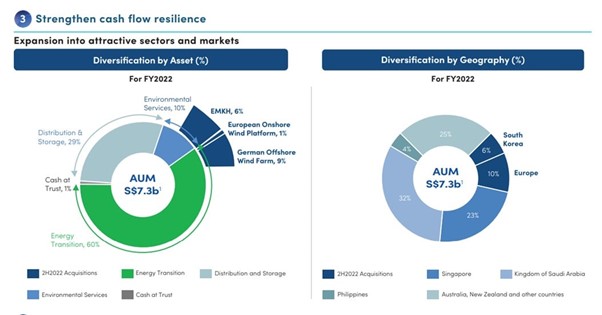

Broadly the assets are split:

- 23% Singapore

- 32% Saudi Arabia

- 25% Australia

- The rest scattered across Europe, Korea and Philippines.

And they have a mix of energy, distribution/storage and environmental assets.

Just like Keppel above, these assets are well positioned to benefit from a transition to green energy, and in a more inflationary world.

Most of the portfolio has inflation protection in being able to pass on higher costs.

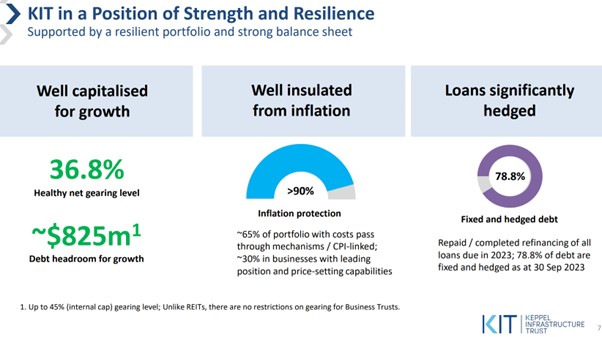

While net gearing of 36.8% is actually acceptable in a climate when most blue chip REITs are running 40% gearing.

What worries me about this dividend stock?

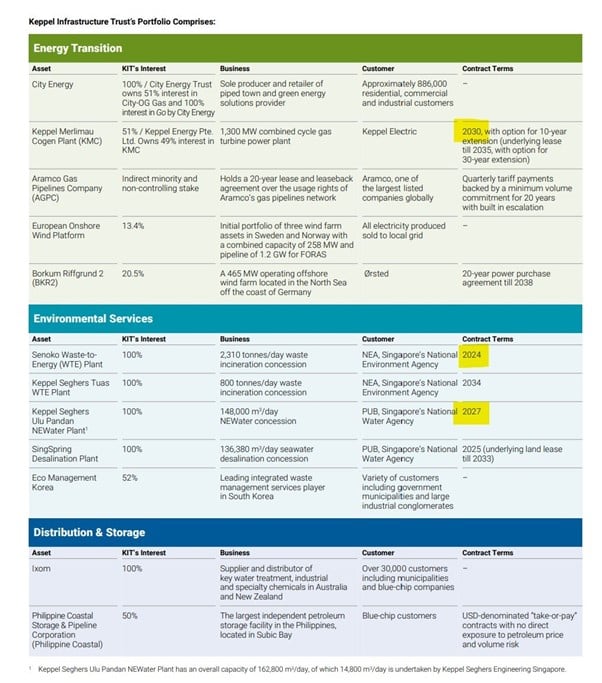

The big one – is that the concession agreements for a few of the Singapore assets will end in 2024, 2027 and 2030 respectively.

These are:

- Senoko Waste to Energy Plant (2024)

- Ulu Pandan NEWater Plant (2027)

- Keppel Merlimau Cogen Plant (2030)

That’s a lot of uncertainty over some of their prized Singapore assets.

Viewed this way, the trailing dividend is artificially high because some of it may be capital being paid out.

The other big risk is similar to that of Keppel.

What if we get a broader slowdown, and electricity / chemical prices go down?

This dividend stock has a lot of exposure to wholesale electricity / chemical prices, and may not do so well if we have a deflationary period.

Full disclosure that I hold a position in KIT.

I like this business trust, but as with all yield plays the buy in price is crucial to determine how much you make. So whether I add to my position going forward will depend very much on how the price trades, and how the global macro evolves.

FH Premium members will get my full insights on target prices, and when I buy (or sell).

ST Engineering – 4.2% dividend yield

Frankly for this last dividend stock, I was scraping the bottom of the barrel (see the honourable mention list for the other dividend stocks I considered).

I just think if you ask me to pick Singapore dividend stocks that I like today, excluding banks, REITs and Netlink trust, then the list isn’t very long.

So I had to break the rule for this last one – with ST Engineering that only pays a 4.2% dividend yield.

What I like about this dividend stock?

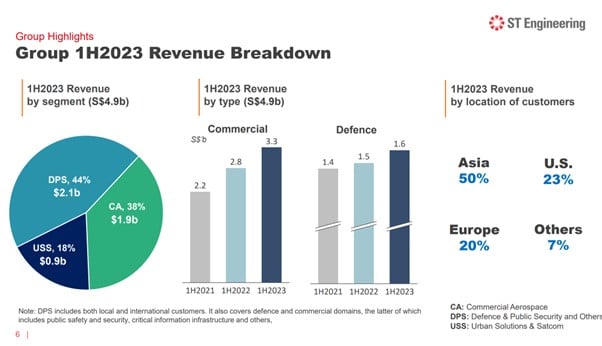

ST Engineering is split into 3 segments.

Ranked by size, they are:

- Defence (44%)

- Commercial Aerospace (38%)

- Urban solutions (18%)

All 3 segments have done well over the past year.

Defence has been up 6%.

While both aerospace and urban solutions have done very well, with the former enjoying the post-COVID boost.

What worries me about this dividend stock?

The problem with ST Engineering, like most other dividend stocks.

Is you really don’t know if you get a cyclical downturn in 2024.

If you do, all 3 segments (other than defence) are likely to get hit.

If you don’t get a cyclical downturn, then interest rates stay high, and how much upside is there really?

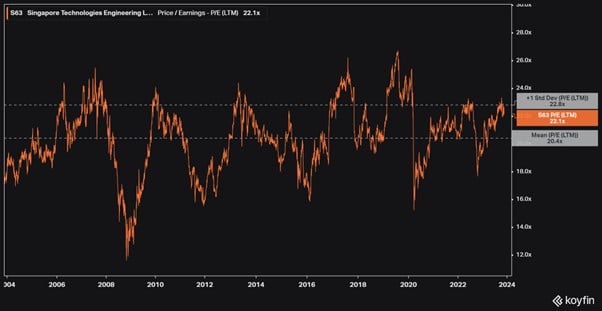

Valuations wise this dividend stock trades at 22.1x Price / Earnings.

That’s about 1 standard deviation above the 20 year average.

With all the risks in 2024, I wouldn’t exactly say that’s a screaming bargain.

And frankly, at 4.1% dividend yield, you can get a close enough yield just buying risk-free T-Bills today.

This just illustrates the point above on how equities don’t look attractively priced relative to cash/bond yields.

You don’t get a sufficient return, to compensate you for the risk of holding equities (instead of just buying risk free T-Bills / government bonds).

Honourable Mention – Other Dividend Stocks I considered

If ST Engineering doesn’t feel like a satisfying end to the list.

Then let me share some of the other names that I considered to replace it.

But for what it’s worth I thought that the other names were even worse.

Hong Kong Land – 6.6% dividend, 0.23x book value

By any metric, Hong Kong Land looks like a dirt cheap dividend stock.

6.6% dividend yield, and 0.23x book value.

But look at the properties they hold, and it’s almost overwhelmingly Hong Kong.

How will Hong Kong real estate fare the next few years?

You tell me.

Throw in a majority 53% shareholder in Jardine Matheson, and realistically there isn’t even an option of unlocking value without consent from the majority shareholder.

Many would argue this is a value trap, and frankly I might agree.

If I wanted exposure to Hong Kong real estate, there are many better plays out there with equivalent dividend yields but a superior property portfolio and more open shareholder structure (see full list on FH stock watch on FH Premium).

Comfort Delgro – 5.3% dividend yield

Speaking of value traps – here’s Comfort Delgro.

For what it’s worth, when Comfort was trading at $1 earlier this year and a 7%+ dividend yield, I thought it was a decent rebound play.

But the price has since rebounded to $1.3ish, and a 5.3% dividend yield.

I’m a lot less enthused about Comfort Delgro at this price.

Structurally I just don’t see where the growth is coming from.

The local taxi business is tough with competition from Grab, and Transcab already selling out.

The bus business has margin pressures from government and rising costs.

The overseas transport business faces strong competition and cost pressures.

I am sure others may disagree, and I am not stopping anyone from buying a position in this dividend stock.

But probably not a play for me.

Closing Thoughts: Top 3 Dividend Stocks to buy in 2024 – 5% dividend yield minimum

And there you have it!

Top 3 Dividend Stocks I would consider to buy in 2024.

Excluding Banks and REITs and Netlink Trust.

Frankly the SGX has gotten to a point where the only stuff that excites me is the Banks and REITs and the occasional business trust.

But whatever the case, as a Singapore investor I like to use SGX to buy the real world plays – the banks, the REITs etc, while paying no tax on the dividend income.

And using US (or China) markets for the sexy growth and capital gains plays.

The full list of stocks & REITs I am looking at is on FH Premium, which outlines my bull / bear case and rough target pricing.

I just updated the list last week, so do sign up if you are keen!

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.