A lot of you have asked me for my views on CapitaLand China Trust recently.

This CapitaLand sponsored REIT has dropped 35% this year alone.

At this price, it trades at a 9.2% dividend yield, and 40%+ discount to book.

Yes, no doubt there is China risk as the portfolio is 100% mainland China.

But at this price, is the risk-reward worth it?

Full disclosure that I hold a position in CapitaLand China Trust, so I was quite keen to take an updated look and decide if I want to average into the position.

CapitaLand China Trust trades at 2009 lows

For the record – yes I know the name of this REIT is CapitaLand China Trust (CapitaLand Retail China Trust before the name change after they bought business park / logistics assets).

You can see the price charts below.

This CapitaLand China REIT is down 45% from post-COVID highs, and 35% from Jan 2023 highs:

In fact if you pull up the chart since IPO.

You’ll realise that CapitaLand China REIT is trading at the lows last hit in 2009, right after the global financial crisis.

Crazy stuff.

CapitaLand China REIT pays a dividend yield of 9.2%

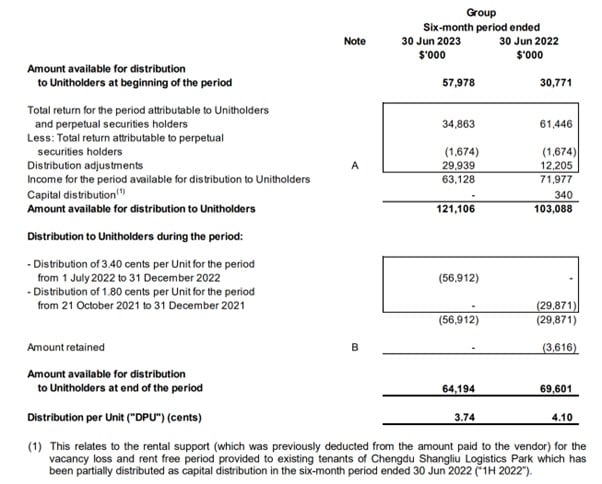

Latest half year DPU was 3.74 cents.

If we annualise that DPU using the latest 0.81 unit price.

That works out to a 9.2% annualised dividend yield for this REIT.

Not too bad really – as long as the REIT trades sideways and avoids capital loss, you’re getting paid 9%+ dividend yield just to wait for the recovery.

Operational Results are not too bad – Net Property Income is flat in RMB Terms

Looking at all the doom and gloom in the media over China today.

You would have expected to see a disaster of an earnings from CapitaLand China REIT.

But digging into the operational numbers – they’re actually not that bad.

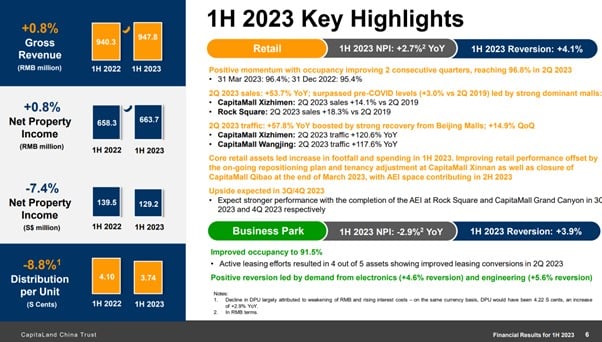

Gross Revenue and Net Property Income are both flattish (up 0.8%) in RMB terms.

Diving a bit deeper into the numbers.

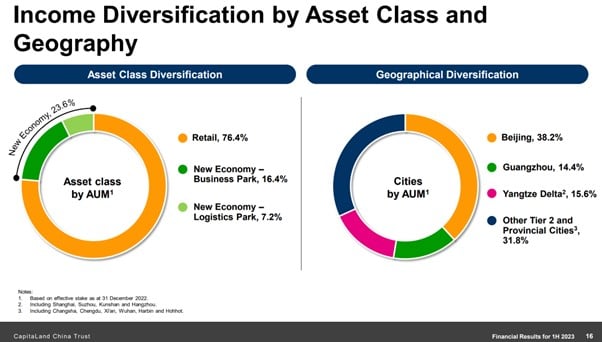

9M 2023 rental reversion for the retail portfolio (which makes up 76% of this China REIT) is +2.8%.

That’s a positive rental reversion, which is much better than what you’re seeing from ahem Hong Kong.

While retail occupancy is stable at 97.8% across the portfolio.

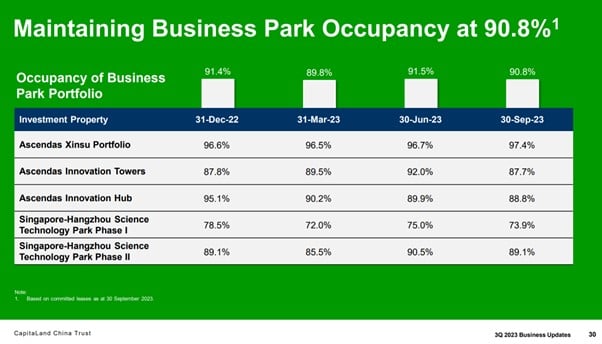

Business park assets too have a 9M 2023 rental reversion of 2.9%.

Occupancy is not doing so great at 90.8% though.

But generally speaking across the board you’re looking at pretty decent operating numbers.

These numbers are much better than what I’m seeing out of Hong Kong, and yet people seem much more eager to buy the dip in Hong Kong.

Big drop in DPU is due to stronger SGD vs RMB

That said.

Gross Revenue and Net Property Income (NPI) are flat in RMB terms.

But NPI in SGD terms – it is down 7.4%.

And DPU in SGD terms – down 8.8%.

Unfortunately, the decent operating performance of the China properties are being dragged down by RMB depreciation against SGD (FX)

SGD strength vs RMB (Forex)

SGD strengthened from 4.6 in early 2022 to 5.34 today.

That’s a 16% move in the currency pair, which is absolutely monstrous in the world of FX.

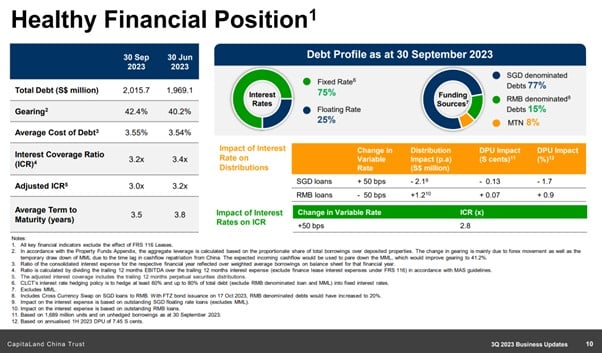

77% of debt is SGD denominated – hit doubly hard by the RMB depreciation

The other problem with CapitaLand China REIT, is that 77% of their debt is SGD debt.

This means that when the SGD strengthens against the RMB, the REIT is hit on 2 fronts.

First, the rental income earned in RMB works out to be less when converted into SGD for dividends.

Same rental income, but less dividends for SGD investors.

Secondly, the value of the debt in SGD increases relative to the value of the properties denominated in RMB.

Same property value, but more debt in RMB terms.

You may ask why CapitaLand China REIT made this “mistake” of borrowing in SGD instead of RMB.

For example most REITs holding German assets would borrow in Euro to provide natural hedging and avoiding exactly this problem (where currency depreciation increases your debt load).

Well the answer is not so straightforward.

It’s because over the past few years, RMB cost of borrowing has been much higher than SGD.

So CapitaLand China REIT could access a cheaper cost of debt by borrowing in SGD instead of RMB – which they utilised to their full advantage.

Unfortunately, this worked against them once RMB started to depreciate – a classic mistake that real estate investors experience once the cycle turns.

But… has RMB depreciation vs USD peaked? That could supercharge this REIT’s returns

That said, this dynamic could easily reverse if RMB starts to strengthen from here.

If RMB strengthens, that will supercharge CapitaLand China REIT as the dynamic reverses:

- Same RMB rental income works out to higher SGD dividend

- Same SGD debt works out to less in RMB terms

Which begs the question – has RMB depreciation peaked?

A big chunk of the RMB depreciation the past 1 – 2 years was due to the fact that China was easing monetary policy while the West was tightening.

China’s economy was weak and they had to cut interest rates in 2022 – 2023.

While the West was fighting inflation and had to raise interest rates over the same period.

This mismatch in monetary policy led to weakness in RMB.

But going forward the next 1 – 2 years.

The Western economy may start to weaken and they may start to cut interest rates.

While China’s economy may mount a recovery.

Look at the charts below of RMB against USD, and you get an idea of what I’m trying to say.

Is the worst of the RMB depreciation behind us?

Higher Borrowing Costs

The second reason for the big drop in DPU is of course higher financing costs.

Finance costs jumped 25% from 2022 to 2023, the same dynamic you see with every other REIT.

But Borrowing Costs likely won’t increase much from here

CapitaLand China Trust has a 3.55% average cost of debt today.

Given that 77% of the loans are SGD denominated, that cost of debt probably isn’t going to increase materially from here given we are close to peak interest rates.

On the flip side, all that SGD borrowings can benefit from interest rate cuts going forward.

So… rental performance is flat, while macro factors may improve?

I guess what I’m trying to say.

Is despite all the doom and gloom over China, you see flattish rental income for this CapitaLand China REIT.

And the big drop in DPU is due to macro factors of RMB depreciation and higher interest rates.

Where we are in the cycle – there is a decent chance both those factors may start to reverse in the next 1 – 2 years, as Western economies weaken and they start to cut interest rates.

That’s very interesting for CapitaLand China REIT, at this point in the cycle.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

How does the market value CapitaLand China REIT? Book Value wise?

Let’s run some simple back of the napkin numbers.

CapitaLand China REIT has a $1.385 billion market cap.

It has $2.015 billion debt.

Add that together, and it means the market values the property portfolio of this REIT at $3.40 billion.

Annualised net property income is $129m x 2 = 258 million.

$258 million net property income / $3.40 billion property value = 7.5%.

In plain English – this means that at today’s price, you are buying into CapitaLand China REIT at a 7.5% blended cap rate for the China property portfolio.

Is this a reasonable valuation?

The portfolio is about 50-50 split between Tier 1 Cities (Beijing, Guangzhou) and non Tier-1 Cities.

So simplistically, you’re looking at a 5% cap rate for the Tier 1 portfolio, 10% cap rate for non-Tier 1 portfolio.

Probably not dirt cheap bargain price just yet – but I suppose it is within fair value range today given the quality of the Tier 1 portfolio.

But FH… China is risky

At this point, I know some of you are going to point out that China is “uninvestible”.

You may point out that China is going to lose the US-China great power conflict, that Xi is a dictator, that China will never escape the middle income trap, that the risk of a Taiwan war is too real.

And who knows, you may be right.

The US-China conflict is one of the defining themes of the 21st century, and I don’t profess to know exactly how it is going to play out.

US-China relations have stepped back from the brink

That said, there are some promising signs.

After things started looking really ominous earlier this year, both US and China appear to have stepped back from the brink.

I don’t think you can underestimate the importance of the recent meeting between Biden and Xi in person.

Yes, both parties have confirmed that the great power conflict will continue to play out in trade, business and technology.

But both parties have also indicated (in the clearest terms I have seen to date) that they do not want to see World War 3.

It’s truly a sign of the times that we can call this a positive development.

Is foreign capital starting to return?

At the same time, you’re also starting to see some possible green shoots of a return of foreign capital to China.

Bloomberg ran an article this week, and I extract:

“Six months after abandoning a hot China recovery trade, Taosha Wang is poised to dive back in.

Encouraged by clear growth support signals from Beijing, increased stimulus for embattled developers and attractive equity valuations, the portfolio manager for Fidelity International is scouring for opportunities again.

“We are looking to increase our exposure in a measured manner,” Wang, who helps manage the $1.5 billion Global Thematic Opportunities Fund, said in an interview. “It has become clearer to investors that economic growth is once again firmly a policy priority.”

Wang is among a growing band of global fund managers who are calling time on this year’s relentless selloff in Chinese assets, which has seen $1.6 trillion wiped off mainland stocks since early February. The excessive pessimism that hammered everything from stocks and the yuan to corporate bonds has run its course, they say, paving the way for a market turnaround as policymakers finally take firmer action to revive the economy.”

Sure, sentiment is fickle and can change on a dime.

So let’s see if this holds.

But… is CapitaLand China REIT a falling knife?

Technical Analysis on CapitaLand China REIT

Fundamentals aside.

The technical are not pretty.

CapitaLand China REIT has broken through all key supports going back to 2009.

There isn’t any support until the 0.50 level, so if you argue this REIT is a falling knife, you may well be right.

The last time it was this oversold was in 2008 during the financial crisis (this is arguably bullish, although not useful to call a turning point).

Opportunity cost of buying CapitaLand China REIT vs other Singapore REITs?

Diversification aside.

If you are serious about deploying money into REITs today, you are spoiled for choice.

Some potential alternatives are:

- Netlink Trust – 6.2% dividend yield

- Starhill Global REIT – 7.8% yield

- Lendlease REIT – 7.7% yield

- MPACT – 6.6% yield

- Keppel REIT – 6.8% yield

Take Starhill Global REIT or Lendlease REIT for example.

It’s a 1.5% lower yield, but you’re getting majority Singapore assets.

Is that a safer (and better) buy than buying CapitaLand China REIT?

Possible – it may even make sense to just buy a portfolio of REITs and diversify away single issuer risk.

Check out my fuller analysis on the REITs I like and potential price targets on FH Premium (previously Patreon).

Why I may buy CapitaLand China REIT at 9.2% yield

Full disclosure that I have a position in CapitaLand China REIT.

It’s not a big position, but a position nonetheless.

So the decision point for me is whether to average in, hold, or cut the loss.

Before this analysis I expected to not like the REIT.

But taking a closer look at the numbers surprised me.

Unlike Hong Kong assets, the operational performance for CapitaLand China REIT’s mainland China assets are very decent.

Low single digit growth in rental reversions, positive NPI (in RMB terms), and stable occupancy.

In fact the drop in DPU is due to macro factors of weaker RMB and higher SGD interest rates – both of which may reverse in the next 1 – 2 years.

If SGD weakens vs the RMB from here, and offshore interest rates go down, while rental reversions hold up, you may easily see 10%+ yields at current prices.

All while buying in at a 7.5% blended cap rate today, for a portfolio that is half Tier 1 Cities and fairly decent quality (personal view, I have visited a number of these assets before when I was in Beijing and Guangzhou).

So yeah… I could get on board with that.

I have not made up my mind whether I want to buy now or to wait, hence the title of the article.

The fundamentals are interesting, but I will use technical analysis to help guide my decisions in times like this.

As always, FH Premium members will get updates as and when I buy.

Or if the facts change, I may easily change my mind on China and sell my position in this REIT instead – updates will be shared on FH Premium.

Closing Thoughts: What is the catalyst to spark a rerating for China real estate?

Some of you may also ask what is the catalyst to spark a recovery in China real estate.

Frankly – I myself don’t see any on the horizon.

The real estate deleveraging is likely to take years to play out, during which time sentiment over China real estate may stay weak.

But on the bright side, this China REIT is sponsored by CapitaLand, and primarily financed with offshore SGD borrowings.

And paying a 9.2% annualised dividend yield.

And at 7.5% blended cap rate for the portfolio, valuations are not demanding.

You are literally getting paid to see what happens next, at fairly reasonable valuations.

As long as things don’t get any worse, you can just collect that yield, while waiting for the next phase to play out.

Whether it is RMB appreciation, US interest rate cuts you won’t know for certain, but stack the odds in your favour and let the market do the rest.

And finally, please note that these are China assets, so do position size well.

Nobody is saying to take a $1 million loan and buy a 150% leveraged long position in China assets.

As with every investment, size it such that if things go horribly wrong, you will still walk out fine.

This article was written on 1 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The real risk is into their bond. if they can’t take rollover their debt, equity will be massively diluted. It does not fit my risk appetite personally. But of course it is all about the price. At what price is becomes attractive ?

Given they raise financing offshore, and are backed by CapitaLand, dont think financing will be a problem.

Problem is more likely to be profitability – what are the rates they can borrow at, and how this affects DPU.

I do not think that raising money offshore is very relevant. What is relevant is whether someone is willing to lend them money, regardless of the location.

That’s actually easy to know current rate. Just look at one their current bond https://www.bondsupermart.com/bsm/bond-factsheet/BQ1895557

They borrowed at 2.4(coupon) but now investors ask for at least 4% (current yield) so basically, for that bond the interest payment will double and need to be deducted from future dividend payment.

But of course that is as of now, what matter is the situation at maturity time which I cannot predict. I can only see that their margin is quite limited and they might dilute equity holder in case they can’t re-finance

This is a CapitaLand backed REIT. Short of a financial crisis or China contagion, I doubt any Singapore bank would be unwilling to lend to them given the CapitaLand brand name, and given they are borrowing SGD. Question is only what is the price of the loan, as you rightly pointed out. 4% is definitely on the high side, will they be able to borrow more cheaply via bilateral loans?

I am not sure the brand name has much value in case of debt, we have seen many valuable brands going bankrupt due to their debt …

A bilateral loans? I doubt it. Why would an investor lend to CapitaLand at 3% when they can get about that rate from risk free government bond ?

I do not mean than this REIT is a bad investment, I just mean that it is priced that cheap due to the refinancing risk. If they are able to refinance, than the unit price will very likely go up north!