Blue chip stocks are shares of strong and well-established companies that lead their industries, often seen as safe and reliable investments for long-term growth. Despite their reputation, we’ve uncovered 5 Singapore Blue Chips that hasn’t quite lived up to the traditional success story – investors would have lost money if they held on to them for the last 10 years.

| Company | Ticker (SGX) | Share price – Nov 2013 | Share price – Nov 2023 | Capital loss | Dividend | Total return |

| DFI Retail Group | D01 | $9.22 | $2.23 | $-6.99 | $1.76 | -56.7% |

| Hongkong Land Holdings Limited | H78 | $5.91 | $3.35 | $-2.56 | $2.11 | -7.6% |

| City Development Limited | C09 | $9.98 | $6.21 | $-3.77 | $1.81 | -19.6% |

| Seatrium Limited | S51 | $4.44 | $0.108 | $-4.33 | $0.315 | -90.4% |

| Genting Singapore Limited | G13 | $1.47 | $0.915 | $-0.555 | $0.24 | -21.4% |

1) DFI Retail Group

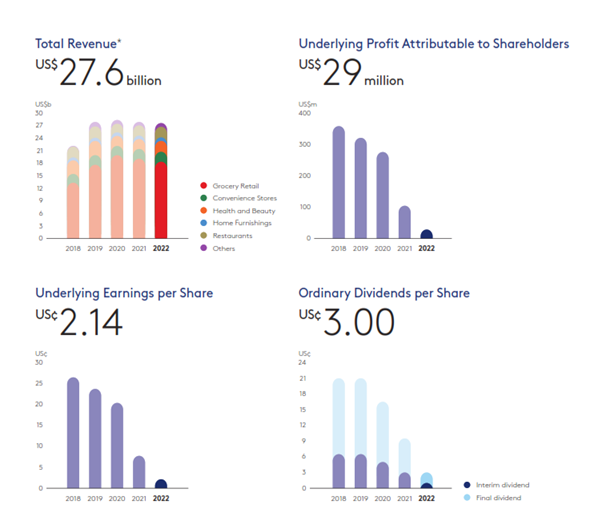

DFIRG, formerly known as Dairy Farm International has gone through several restructurings, trying to respond and reposition its various brands to changing market needs.

DFIRG first carried out a strategic review nearly six years ago, where it announced plans to grow in China, revitalise its South East Asia portfolio, and concurrently uphold the strength of its Hong Kong brands. These initiatives were all underpinned by digital innovation, an area where DFIRG acknowledged being slower than most of its competitors.

DFIRG has made several big moves such as the removal of hypermarkets, repurposing those sites, improving its supply chain with the help of technology, implementing brands such as yuu Rewards and selling its iconic Giant brand.

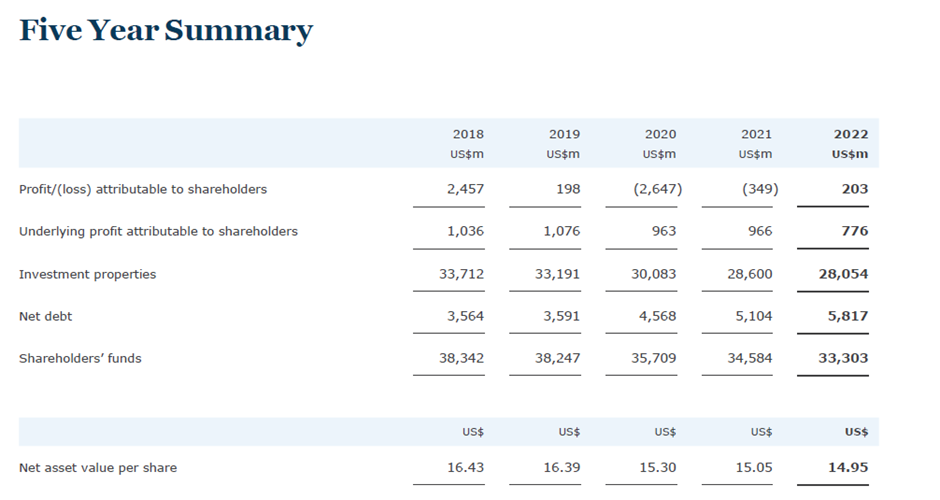

In the years since, even though DFIRG was somewhat able to maintain revenues, its slim margins became even slimmer as profits shrank by 90% and DFIRG was forced to cut dividends to a mere 3 cent per share as compared to 20.5 cents per share five years ago.

Unlike Sheng Siong who has been able to hold on to post pandemic gains with share price remaining flat since Nov 2020 when the first vaccine was announced, DFIRG has actually fallen nearly 50% since.

2) Hongkong Land

HKLand was trading at $7.40 just before the protests in Hong Kong started in March 2019, much higher than its share price in 2013. It all went down hill thereafter. A cumulative effect of the Hong Kong protests, COVID-19 pandemic, China-US political relations, the current commercial office environment as well as the high interest rate environment has caused the net asset value per share to decline by nearly 10% or $1.48.

After accounting for dividends, HKLand retaining underlying earnings of about $0.98 in the last 5 years which meant that the net asset value decline stemming from a devaluation of its investment property portfolio was nearly $2.50. This is a 15% decline.

This was mainly because of its prime Hong Kong Central office portfolio. Although the portfolio remained resilient, outperforming the broader market due to its prime CBD location and premium offering, its physical vacancy was 4.9% at the end of 2022. It used to be always nearly fully occupied.

Rental prices for Hong Kong Central have also declined substantially. It used to be US$20 psf in 2018 and is now 35% lower at $13. In comparison, rental prices in the Singapore CBD has largely stayed flat. HKLand’s underlying profit has declined nearly 25% as a consequence.

HKLand is currently trading at a price to book value of 0.23 times. While other property developers and landlords are also trading at depressed valuations, HKLand is probably at the tail end of the valuation spectrum despite being perceived as having one of the most prime office portfolios in Asia.

3) City Development

CityDev is at a decade low, even lower than during the pandemic and when it wrote off its Sincere Group acquisition which it disposed off for $1 and wrote off its investment of $1.9 billion at the end.

Its net asset value fell from $11.60 before the pandemic to $9.38 as at Dec 2020. It has since creeped up to $10.16 as at Dec 2022, still below the pre pandemic levels.

Note that City Development carries its investment properties at cost unlike many other companies who hold them at fair value. Its revalued NAV stood at $16.98, vs $16.46 in 2019 and $14.26 in 2020. In addition, it was disclosed that after including the revaluation surplus of its hotels, which comprises mainly of its Millennium and Copthorne(M&C) Hotel assets, the final revalued NAV stood at $19.14.

This means that CDL has built back stronger after its Sincere Group investment. CDL is now trading at a price to book value of about 0.32 times, not far off from HKLand’s valuation.

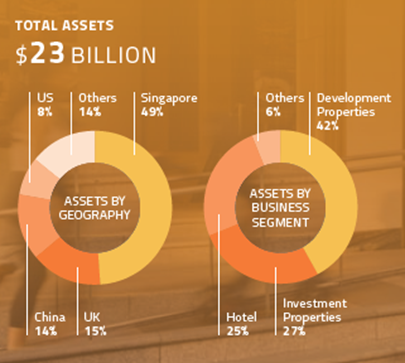

CityDev has a sizeable portfolio of properties in China and the UK which has seen its valuation decline due to supply/demand factors, the interest rate environment and weakening exchange rates.

Now that it is focusing its efforts on building a strong development pipeline. CityDev has been very active in the Singapore residential property market, launching several successful condominiums with very strong sales performances, outperforming its peers. It is also growing its global living sector portfolio both through acquisitions and development.

CityDev has a sizeable recovery play in its hospitality portfolio totalling 25% of its asset portfolio and mainly comprises the M&C and M Social brand. It also holds a 27.21% stake in CDL Hospitality Trust which has 20 properties managed by various brands.

4) Seatrium

Seatrium, formerly known as Sembcorp Marine has the worst total return of the list of companies here with a total loss of more than 90%. It also went through a merger with Keppel’s Offshore and Marine’s division in an attempt to combine capabilities, bulk up its global presence and seize economies of scale to compete. At the same time it was facing a probe from the regulators over alleged corruptions in Brazil.

After years of low capital spending by end customers, the industry finally revived and Seatrium now has a sizeable net order book which currently stands at $17.7 billion after including contract wins of S$4.3 billion to date.

The order book mix comprises approximately 40% renewables and cleaner/green solutions with deliveries till 2030 in line with the marine and offshore industry’s commitment towards decarbonisation and low-carbon energy solutions.

Seatrium was able to turn an operational profit but had to incur provisions for some of its projects and recorded a net loss for 1H23. It also forecasted for a net loss for FY23 as a result of these provisions. This presents the difficulty of executing a project that spans several years amid an uncertain macro environment for itself and its customers.

5) Genting Singapore

Genting Singapore was able to tide through the pandemic due to its strong net cash balance sheet as well as from government grants.

Before the pandemic, partly due to its strong cash position, investors were eagerly anticipating the prospect of Genting Singapore winning the bid for another integrated resort in Japan. Unfortunately, this possibility ended when Yokohama City decided to cancel the integrated resort bid process. Genting Singapore has also clarified that it is not presently pursuing a bid for the development of an integrated resort project in Osaka or elsewhere in Japan.

Genting Singapore has gotten back on its feet and has almost but not yet reached its pre-pandemic strength. Revenue for 2H22 was at $1.1 billion, slightly below the $1.2~$1.3 billion rangeseen in 2018 and 2019. Net profits for 2H22 was at about $230 million, significantly less than the $370~$390 million recorded in 2018 and 2019.

Genting Singapore says the capital expenditure for the upgrade and expansion of Resorts World Sentosa (RWS) will hit $6.8 billion and much of it will be completed by 2025. This is significantly higher than the $4.5 billion indicated in April 2019. Genting Singapore expects to fully fund this amount through internal resources, considering it has $3.4 billion in cash and generates a sizeable amount of cash every year.

Closing statements

All five companies mentioned here are large and well known; however, investors who have held these stocks for the past 10 years would have incurred losses.

These companies have constantly tried to keep up their competitive edge but have not been able to stem the bleeding of their share price.

This also shows that while dividend can help to numb the pain, it is not able to fully compensate for the capital loss. In many cases, much of the dividend was received in the earlier part of the decade as these companies went through gradual declines and reduced their dividend payouts over the years.

Of these five companies, we think only CityDev has shaken itself off from its mistakes and positioned itself for growth and has its net asset value recovery to back it up.

HKLand and Genting Singapore are potential recovery plays, HKLand due to its undervaluation and robust dividend payout and Genting Singapore from its expansion plans. Both these companies were also identified by Alvin as Singapore Blue Chip companies with moats earlier this year.

At this juncture, we would avoid DFIRG and Seatrium until we identify strong recovery catalyst.