For Singaporeans and PRs, the Central Provident Fund (CPF) is one of the most important financial assets.

It’s often overlooked in the hustle of our 20s and 30s.

Yet, understanding this social security system early is crucial to grow a sizeable nest egg in your golden years.

This article is written by a Financial Horse Contributor.

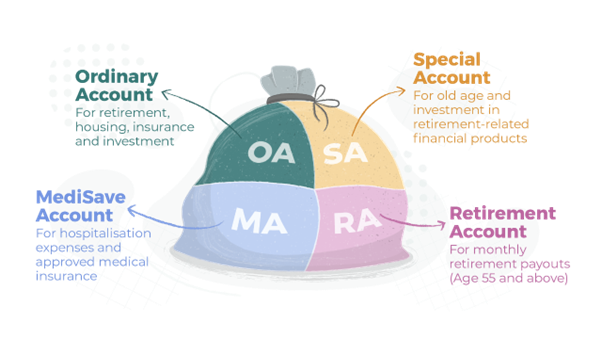

What is CPF, in a nutshell?

CPF is designed to address the fundamental pillars of retirement: (1) Home (2) Healthcare (3) Retirement income.

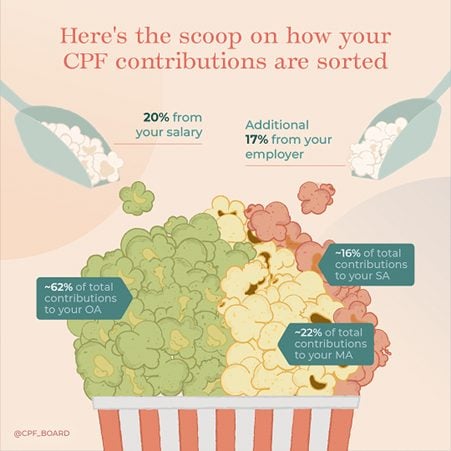

Each month, 20% of your salary is channelled into three distinct accounts tailored to fulfil these needs: the Ordinary Account (OA), MediSave Account (MA), and Special Account (SA).

When you turn 55, CPF will create an additional Retirement Account (RA). The savings in your RA is meant to provide you with payouts in retirement.

If you’re below 55, your CPF contributions are allocated as follows:

Compound Interest: Your Secret Weapon

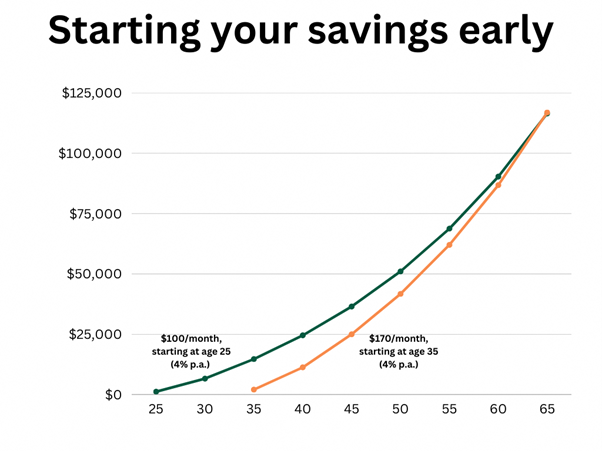

Building up your CPF as early as possible allows compound interest to do its magic.

As Albert Einstein said: “Compound interest is the eighth wonder of the world. He who understands it earns it. He who doesn’t pays it.”

Imagine setting aside just $100 per month from the age of 25, earning a modest 4% annual return. By the time you retire at 65, your savings will have snowballed into an impressive $116,000. Now, procrastinate a decade until 35, and you’ll need to save $170 per month to catch up.

Now that the importance of early action is clear, let’s dive into some practical tips to maximize your CPF potential.

Maximising your bonus interest on your first $60,000 in combined CPF balance

“Hack” your CPF early in your career.

The first $60,000 of your combined CPF balances earns an additional 1% per year. This means your OA earns 3.5% (capped at $20,000) and your SA and MA earns 5%.

You’ll want to reach the $60,000 as soon as possible to start accumulating more interest and compound that interest over a longer time.

Make voluntary cash top-ups to MA and SA

Rather than relying solely on your monthly salary for CPF contribution, consider making a cash top-up or CPF transfer to boost your balances.

The Retirement Sum Topping up Scheme allows you to add to your MA or SA account.

In 2022, 294,000 people topped up S$4.8 billion, a 60% increase from the previous year.

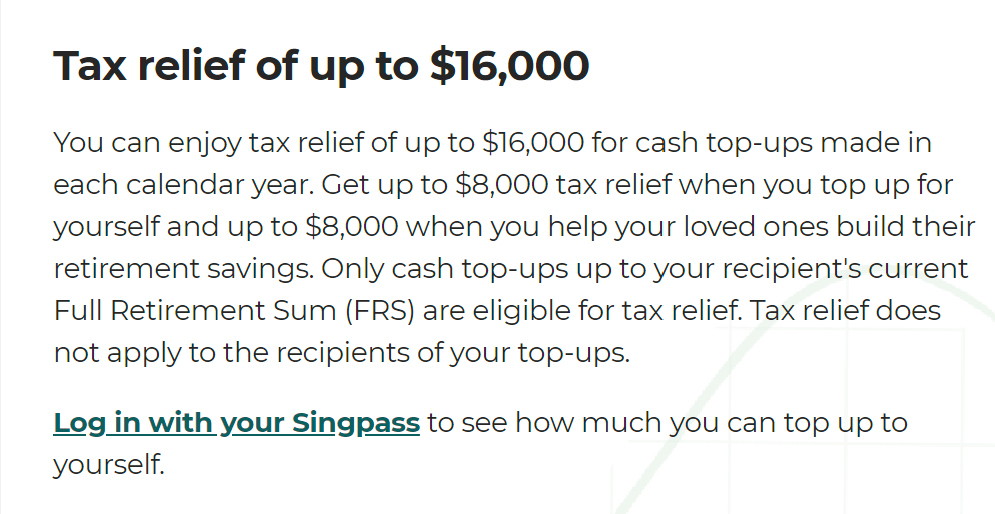

Apart from taking advantage of the 4% interest rate (or 5% if you haven’t hit $60,000), another extra benefit of CPF top-ups is tax savings. You enjoy an equivalent amount of tax relief for cash top-ups made in a calendar year of $8,000 to your CPF MA or SA account.

For example, if you earn $80,000 a year and top up the full $8,000, you would have saved $560 ($8,000 x 7%). The higher your tax bracket, the greater the potential savings. You can also make a cash top-up to your loved ones.

Keep in mind, though, that this comes with a trade-off in liquidity because transfers are irreversible.

Between SA and MA, the latter offers more flexibility, allowing you to cover hospitalization, outpatient treatments, insurance premiums, and vaccinations.

If topping up a lump sum feels too hefty, consider spreading top-ups throughout the year to improve your liquidity.

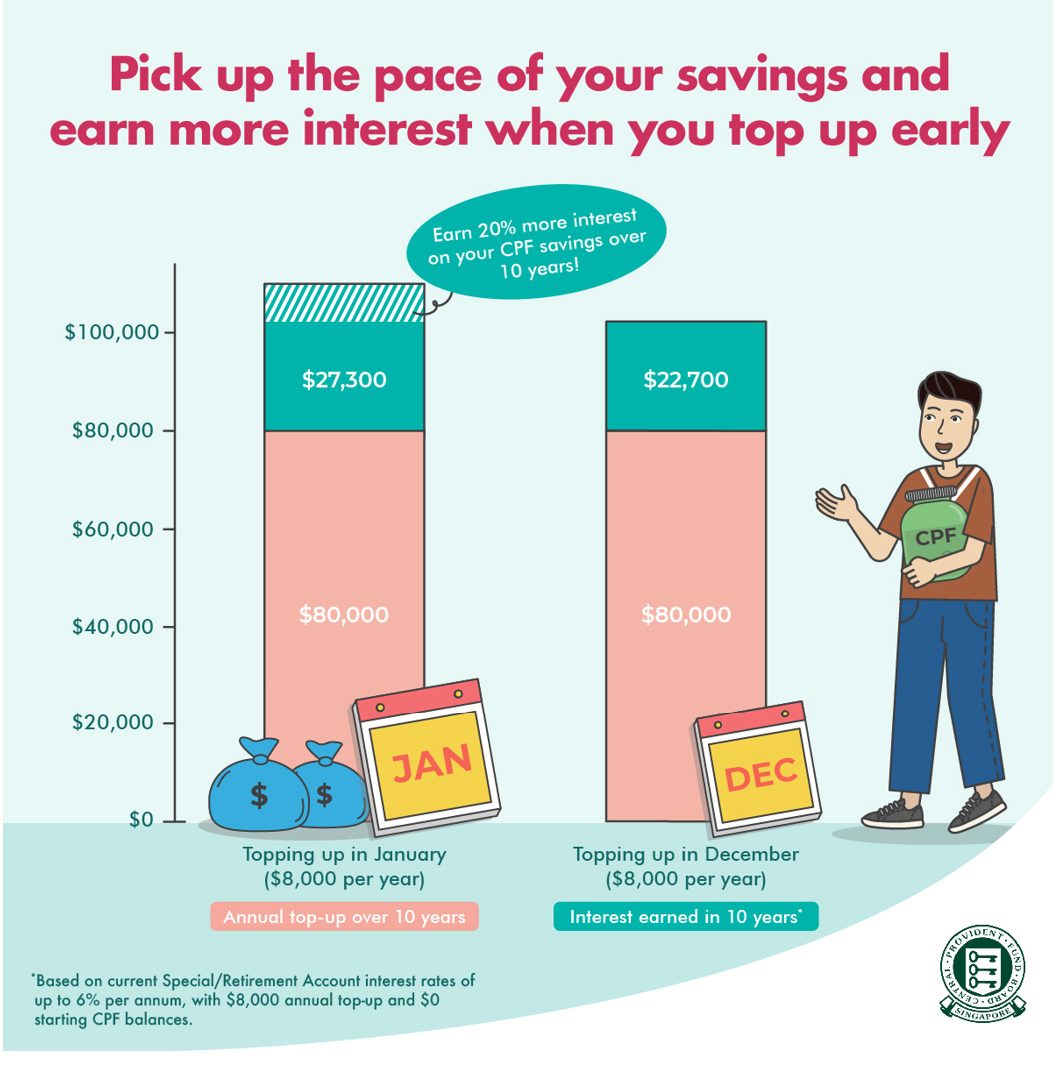

Bonus tip: make a CPF top-up in January

Making a top-up in January is an easy way to boost your interest.

By making a top-up first thing in the new year instead of later, you could earn up to 20% more interest on your CPF savings in 10 years.

Using CPF to Navigate Homeownership

As you aim for that first home in your 20s or 30s, your monthly CPF OA contributions can help you save up for the down payment.

This helps you free up liquidity to use your cash savings for expenses like your wedding, renovations, or buying furniture.

It’s a balance between using your OA and cash, taking into consideration the attractive interest rates earn on your OA.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

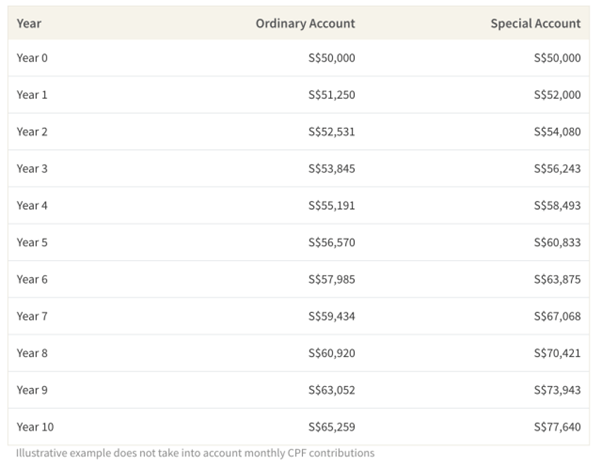

Transfer your OA savings to SA for higher interest

Assuming you already have a home and budgeted for it, transferring your excess OA savings to SA is another way to maximise your interest.

The 1.5% higher interest SA account offers over OA makes a huge difference over a long period.

Imagine you deposited $50,000 each in an OA and SA account. Leave both untouched for 10 years. In the end, the OA account will grow to $65,259. The SA account will grow to $77,640 – a $12,381 difference! This is compound interest at work.

While juicing your yields is attractive, remember that these transfers are irreversible. So it’s important to ensure your home financing situation is secure before committing to stashing away money you can’t touch until retirement.

Invest your OA savings under CPFIS

Another option of making your CPF money work harder is to invest it.

The CPF Investing Scheme (CPFIS) lets you invest CPF savings in various financial products, like Investment-Linked Products (ILP), unit trusts & ETFs, and bonds.

As your CPF forms your retirement nest egg, you’re limited to relatively conservative products to mitigate a huge loss.

And so, if you choose to invest, make sure you’re only using discretionary funds you can set aside for the long term, and not any essential funds.

Lawrence Tan from the Institute for Financial Literacy, notes: “You want to invest your beer money, not your milk powder money.”

In the podcast, Lawrence also suggests asking yourself these questions:

- Should you invest or retire your debt?

- Let’s say you have a housing loan costing you 5% interest. If you choose to invest your free cash, then you need to be confident to earn a return higher than that.

- Otherwise, you should prioritise retiring a portion of your debt to get a 5% “yield” on the interest payments you’re saving.

- Do you have the psychological and emotional resilience to weather the ups and downs of market volatility?

- If you have a lower risk tolerance, you might be better off leaving your money in OA to earn the guaranteed 2.5% interest. After all, you’re not guaranteed to outperform.

- In 2021, one in six CPFIS-OA members failed to earn more than 2.5% p.a. with their investment.

|

Financial Year |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

Percentage of CPFIS-OA members with profits more than 2.5% p.a. |

27% |

78% |

74% |

38% |

46% |

75% |

83% |

CPF Nomination

Along with making a Lasting Power of Attorney and an Advanced Care Plan, making a CPF nomination is part of legacy planning.

The CPF nomination ensures your CPF savings will be distributed to a beneficiary of your choosing.

Without a CPF Nomination, CPF savings will be transferred to the Public Trustee for distribution in accordance with the intestacy or Muslim inheritance laws of Singapore.

Start early to reap rewards

Mastering CPF early will pay huge dividends in your later years.

With the magic of compound interest, a modest monthly payment, cash top-up, and investment gains will snowball into significant savings with time.

Mortgage Refinancing Tool

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Start trading with your OCBC Online Equities Account here!