Warning: Photo intensive post

2023 has been very kind and generous to me. In almost all aspects of life. I really can’t complain. It’s like 1 of the most fulfilling, fun, smooth sailing years that I can remember in recent times. Worked hard, played even harder. Accumulated successes and memories, added to both knowledge and experience, grown smarter, sharper, wiser. Everything really just went well. I would’ve no issue with every year being like this for the rest of my life.

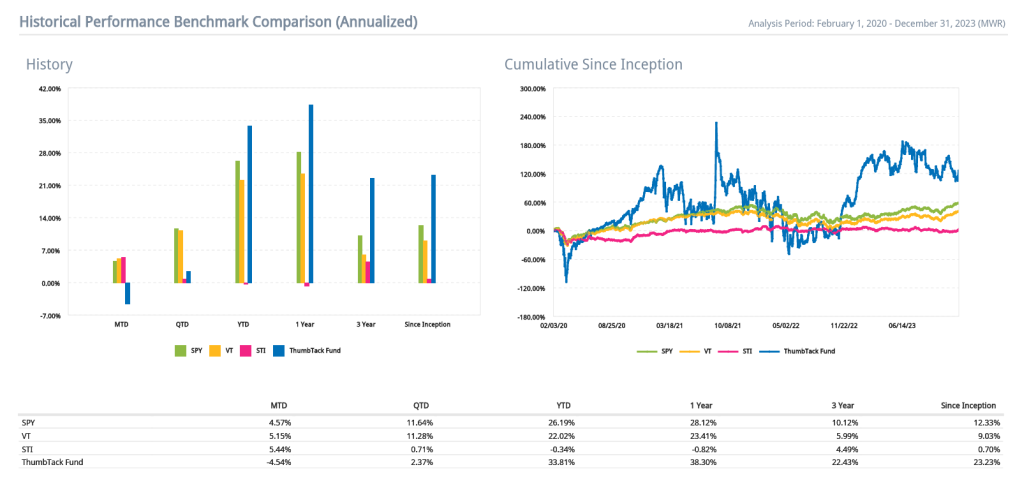

FULL YEAR 2023:

SPY: +26.19%

VT: +22.02%

STI: -0.34%

TTF: +33.81%

SINCE INCEPTION (FEB 2020), ANNUALIZED:

SPY: +12.33%

VT: +9.03%

STI: +0.70%

TTF: +23.23%

Note: Returns are MWRs, all figures in USD

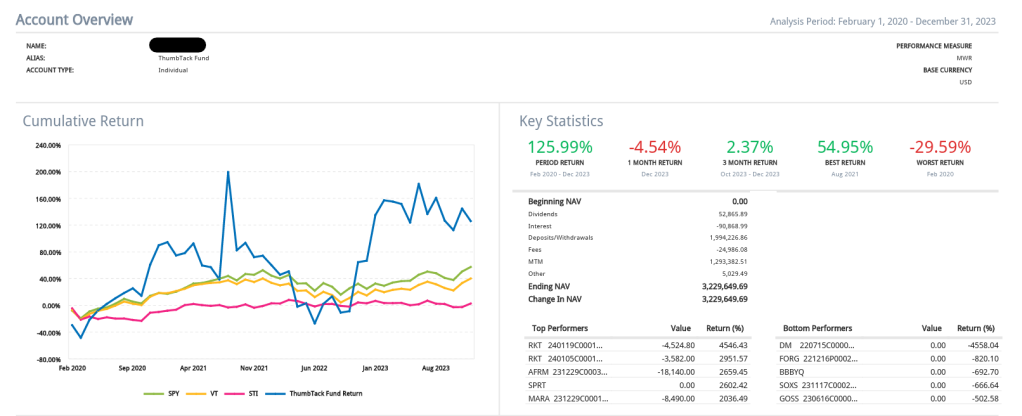

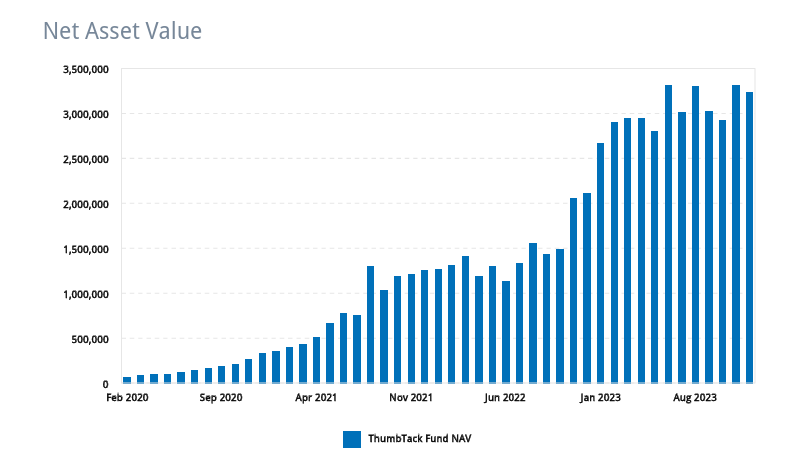

TTF’s NAV: USD 3,229,649.69

Deposits/Withdrawals: USD 1,994,226.86

Net capital gains since inception: USD 1,235,422.83

For reference, the last fund report:

Since TTF was incorporated in Feb 2020, this means that TTF has enjoyed a nett gain of USD 1,235,422.83 over a period of 46 months of investment activity, which works out to be USD 26,857.02 every month, or approximately SGD 35.5k per month from Feb 2020 to date.

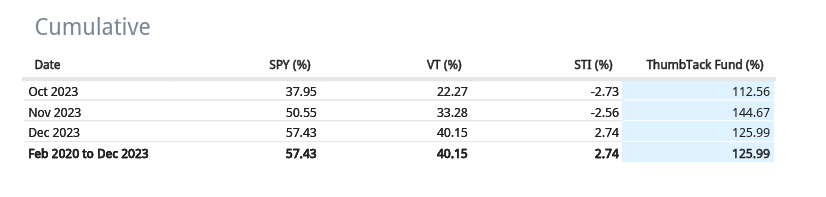

Cumulative ROI (Feb 2020 to Dec 2023):

SPY: +57.43%

VT: +40.15%

STI: +2.74%

TTF: +125.99%

TTF has generated double digit money weighted returns every year since inception:

2020: +89.83% (https://thumbtackinvestor.wordpress.com/2021/01/02/thumbtack-fund-report-6-rose-of-jericho-2020/)

2021: +24.91% (https://thumbtackinvestor.wordpress.com/2022/01/07/thumbtack-fund-report-10-hello-2022/)

2022: +11.94% (https://thumbtackinvestor.wordpress.com/2023/01/02/thumbtack-fund-report-13-hello-2023/)

2023: +33.81%

In the corresponding report at the end of 2022 (https://thumbtackinvestor.wordpress.com/2023/01/02/thumbtack-fund-report-13-hello-2023/), I wrote that I had 2 objectives for 2023:

Well, in 2023, TTF has accomplished both lofty targets.

So it’s time to raise the bar further. The new 2 targets for TTF in 2024 are:

- Generate an annualized return above the current annualized 4yr average of +23.23%. That’d further increase my long term CAGR.

- Increase AUM for TTF to USD 4.5mil

2023 has been a fantastic year partly cos TTF just simply zoomed into a huge lead right off the bat and never looked back for the entire year. There wasn’t a single day where TTF’s returns fell below S&P, although as you can see in the chart, towards the end of the year, S&P started rallying hard. I hope 2024 starts the same way.

I continue to execute my “all weather” strategy, by aiming to match or outperform or even slightly underperform the S&P in good years, but remain in the green in the bad years. By doing so, the alpha compounded over time should be quite amazing.

Another major reason why 2023 was such a great year for me was that TTI Junior did really well in school, winning the equivalent of soccer’s Ballon d’Or by topping both Maths and Science in school, and coming out overall within the top 5.

妹妹 also did well, but since there’s only 1 medal up for grabs for primary 2, that’s what she got.

I also wrapped up the year by taking almost the entire Dec off, spending about a week each in Finland, Sweden and Estonia.

Landing in Helsinki

Took the Santa Express, an overnight train all the way up north to Lapland area

And arrived early in the morning in Rovaniemi, only to be greeted by -15 degrees.

Snow is so deep, the entire boot sinks into the snow, making walking a laborious and slow process.

Santa Claus village

Reindeers!

Tried, tough luck, didn’t catch any Aurora Borealis. Also, it’s a bit mind boggling to think that this whole place of ice and snow will turn into a massive lake in 6 months.

Snowmobiling through the cold arctic forests late at night is definitely 1 of the most unique experiences I’ve had.

I can never understand art. I still like to go art museums whenever I travel… I just cannot understand it. It’s worse than the markets. 99% of it is just hocus pocus, you say I say kinda stuff to me.

Perfect snowflake

I have a queer habit: Wherever I go, I always like to visit the local library. Just to see the vibes within the library. Partly for the architecture, partly to see the people in it. Cos libraries aren’t tourist destinations, so it’s just the locals in them. So visiting libraries give you an authentic, local vibe.

Rovaniemi’s Library

Cool. But not my favorite. My favorite thus far, is in Stuttgart, Germany: Stuttgart City Library

Back to Finland:

1st attempt at making a low effort snowman/snowmonster.

Heng ah, asian food is everywhere nowadays. I’m not exactly very adventurous with food.

Stockholm

Stockholm’s city library

Go Sweden, obviously must try Ikea’s swedish meatballs right?

It’s freezing and we are all wrapped up in 4 layers of clothing, but got a young pretty girl literally in mini skirt doing some photoshoot.

Christmas Market in Stockholm, Sweden

Glogg is their local version of a warmed mixture of wine together with some spices, whiskey and rum. Taste is ok but errr, not really my cuppa tea.

Arrived in Tallinn, Estonia

Little bots doing delivery

Tallinn’s Christmas Market

1 of the rare winter days where we get sunlight and the weather is so good. The photos taken on this day were simply the best! Look at this! It’s so chio.

Drone flying in the sky

Like I said, I keep paying money to go art museums, but I really don’t know what I’m looking at.

Helsinki’s University Library. A continuation of my queer hobby of collecting library visits from all over the world.

I wouldn’t mind studying with this view.

Brave folks actually going into the sauna, then jumping into the public pools. There are 2 pools: 1 is a heated one, and the other one… well, it just takes in the icy water from the sea, so it’s literally freezing.

Public saunas

After we left, there was a queue of random strangers just behind us, all waiting to take photos with our snowman. (and maybe claim credit on Instagram. If any of you see this online, it’s TTI’s family’s work ok!)

Of course, we took away our trapper’s hat and the scarf.

OK, now for the serious stuff again.

This is some of my macro view for 2024. Disclaimer first: This is not financial advice, it’s not even advice. It’s hocus pocus, just me talking about some random thoughts in my mind. I might change my views tomorrow. And even if I don’t, for the record, I don’t really invest by taking market directional bets. Meaning I don’t try to go long if I think markets are going up, or try to short the market just cos I think it’s coming down, or cos of recession, or cos Powell had a nightmare last night, or whatever man.

I do try to have a macro view, and hope it’s at least not 180 degrees completely wrong, cos it does influence some of my portfolio composition, but I repeat, I DO NOT TAKE DIRECTIONAL BETS ON THE MARKETS. So take from this, what you will.

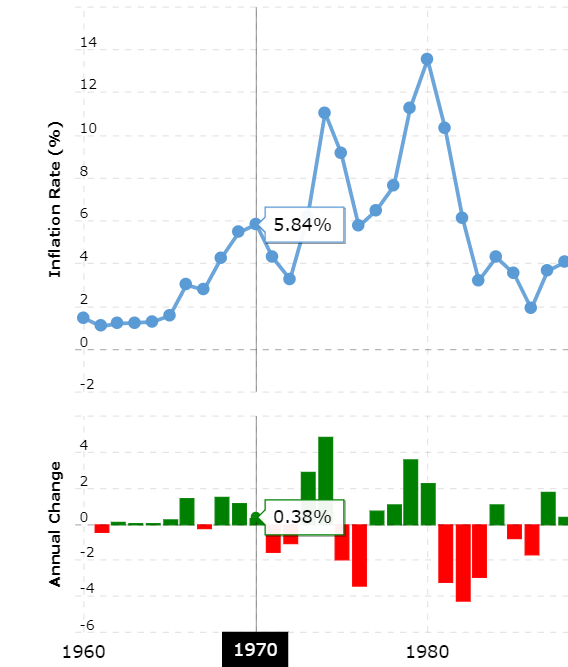

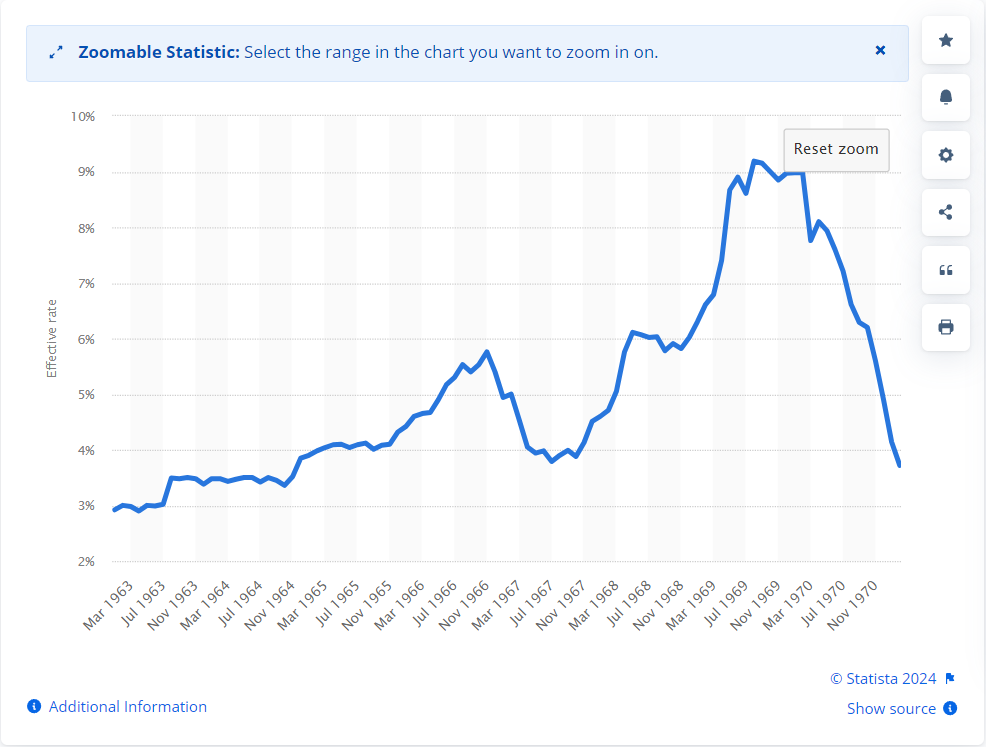

To understand the very complex relationship between the trilogy of Fed interest rates, the US markets and the US inflation rates, let me bring you guys back to the Volcker’s 1970s era.

Towards the later part of the 1960s, inflation started spiking up, hitting 5.8% by the end of 1970.

“Beginning in 1965, however, the general price level began to rise at an increasing rate. The CPI rose 23.07% from 1965 to 1970, with an annual percent increase of about 4.25%. While industrial production continued to rise and unemployment continued to fall, the economy came under severe pressure. The rapidly increasing general price level was unpopular, and eroded the incomes of the elderly and other Americans living on fixed incomes. High inflation also discouraged people from saving money, and increased the pressure on the dollar, which was already in a precarious position because of its role in the international monetary system.”

https://www.historycentral.com/sixty/Economics/Inflation.html

Predictably, the Fed raised interest rates in response to the elevated inflation, hitting a high of OVER 9%, at around the end of the century.

The rise in interest rates eventually triggered a market crash, and S&P fell from a high of around 940 in late 1968, to around the 570 mark in mid 1970. Grey shaded area indicates an official recession.

Thus far, this trajectory is eerily similar to what we have went through in the previous few years, and we are at the point in this story where the rates have risen to an interim high. That is, we are at the same spot as the 9% fed rates in late 1969. If we follow the same trajectory, according to history, S&P should be moving down, culminating in a recession.

Yet the US economy remains strong, unemployment numbers, officially at least, remains low. Hence the recent relief rally by the markets. More and more folks are expecting the rare “soft landing” scenario to take place.

I guess the key question is whether the US would enter into a recession in 2024, and if so, whether it’d be a hard or a soft landing. I don’t know, but I’d offer a few observations:

- The impact of elevated interest rates has a lag, and this lag can come in the form of just a few months, or even a couple of years. The Fed almost tripled the interest rates from the mid 1960s till the end of the century, and although S&P was highly volatile, the real crash/recession only occurred a few years later from 1970.

- In response to the recession, the Fed started cutting rates aggressively sometime in Feb 1970, bringing it all the way back down to where it started to begin with. The Fed’s rate cutting tends to be reactive, and they cut rates only when the economy is in recession and unemployment numbers have gone up. Would this be the same this time around? Or would Powell react with more sensitivity? I personally believe it’d be the latter, cos Powell would’ve seen and learnt from the past Fed experiences.

- The Fed continued cutting rates during the recession, even as the S&P started rebounding, and didn’t stop until they reached all the way down, back to the 3% mark. This set the stage for inflation to rebound with a vengeance (but that’s another story for another time, we are not there yet)

TLDR version: My personal opinion, and it’s not a strongly held one, is that the markets have gotten ahead of itself and rallied too hard going into the end of Q4 2023. The strong rally fed on itself, as money managers would be loathe to be caught underexposed to the markets when the year closed, and they had to open their books. In the short term, I’d be a bit more cautious about having too much long exposure. (Actually, I’ve already positioned accordingly)

In the mid to longer term, there really isn’t any visible headwinds on the horizon. At this stage, the economy is still holding up, the Fed has leeway to cut when and if they need to. Rate cuts and money printing are very strong cures for an ailing economy, and there really doesn’t seem to be an upper limit as to how much debt the US can hold. So I’m betting this would continue status quo, as it has been for the past 200 years.

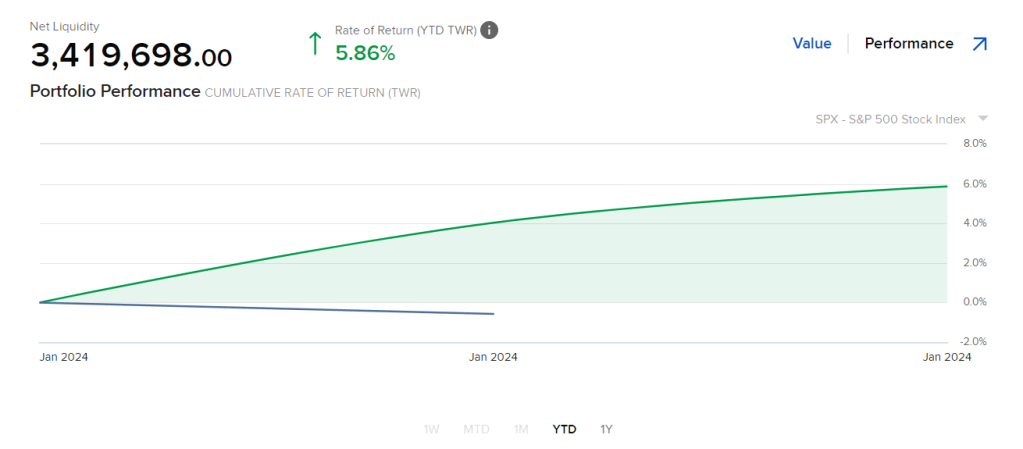

UPDATE:

Only 2 trading days into 2024, seems like I’m getting my wish of a good start to 2024:

But who knows… markets will do what the markets do, it’s the number at the end of the year that counts.

That’s all I have here.

GLTA for 2024!

One comment