As some of you will know, I’ve been pretty neutral / bearish on the banks for most of 2023.

In most of 2023 I was pretty bearish on the banks due to a combination of (1) interest rate cut expectations, and (2) uncertainty over economic growth.

For good reason too, because here’s DBS share price for the past 2 years.

Share price has pretty much gone nowhere.

But after the events of the past 2 months, I am starting to change my mind on the banks.

To the point where I may actually pick up a position in the Singapore banks in 2024.

I’ve been mulling over this for a while, so I wanted to use this article to share updated views.

DBS 2 year price chart for reference:

What has changed?

To put it simply – the Treasury “Pivot” by Janet Yellen in late Oct, followed by the Fed “Pivot” by Jerome Powell in Dec.

I’ve shared the fuller thought process with FH Premium subscribers.

But the long and short is that both policy makers have indicated a switch in their focus.

Instead of prioritising the fight against inflation, they are now prioritising preventing an economic slowdown.

And because this “pivot” has come so early, there is a risk that this may result in a resurgence in economic growth (and inflation).

You may argue that the Feds have yet to actually cut interest rates.

But the actions have already had a very direct impact on Treasury yields – plunging from 5.0% to 4.0%:

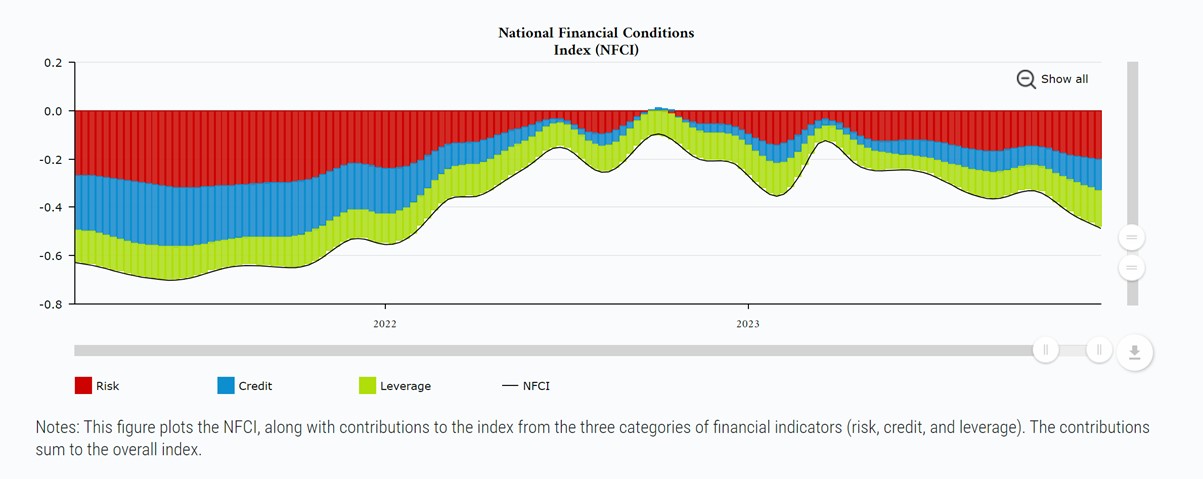

While financial conditions have loosened significantly in Q4 2023:

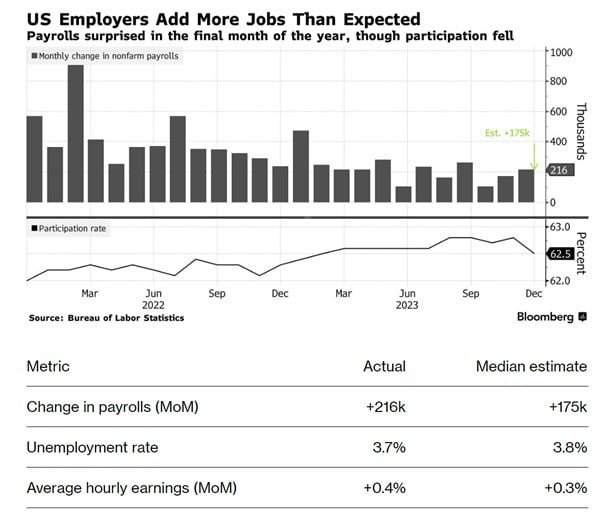

In fact some of the latest employment and manufacturing data is showing a pickup in growth in Q4 2023.

My previous macro views

A month ago, I wrote an article that Banks are worrying at this point in the cycle because:

- Interest Rate cuts going forward

- Slowing Economy

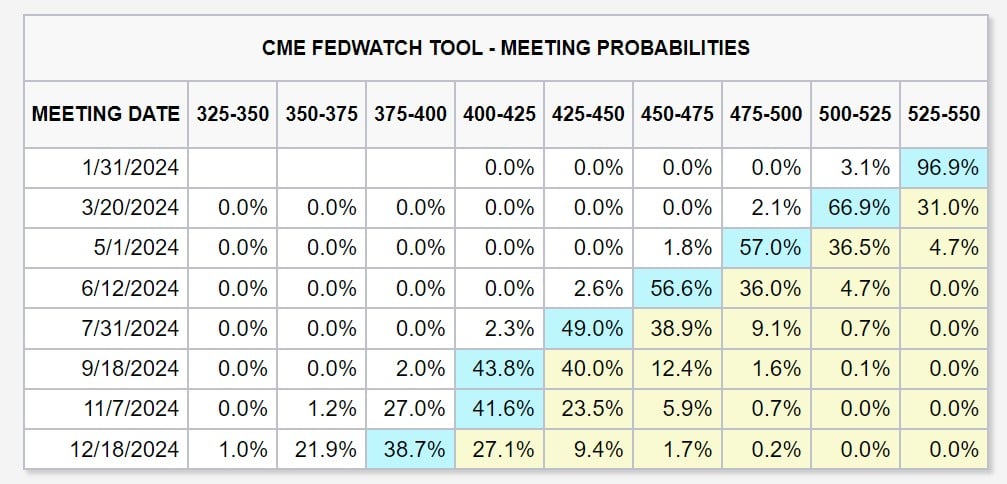

No doubt (1) is still in play, with the market pricing in 6 interest rate cuts in 2024:

But in my view, the risk of (2) has changed materially after the early pivot from policy makers.

Which don’t forget – 2024 is a US election year, and a lot of recent signals are suggesting they may ease policy further heading into the elections.

What are the possible macro outcomes?

The 3 possible macro outcomes at this point are summarised below.

Scenario 1 and 2 were the main outcomes before this, but the early pivot from policy makers has raised the possibility of a new Scenario 3.

- Scenario 1 – Hard landing (economic recession, rapid Fed rate cuts)

- Scenario 2 – Slow Grind Down (economy avoids a recession but stays slow, minimal Fed rate cuts)

- *New* Scenario 3 – No landing (economic growth reaccelerates due to rapid loosening in financial conditions post pivot, further juiced by rate cuts / easy monetary policy heading into elections)

What has changed?

With the recent events.

I would say the possibility of Scenario 1 has gone down.

The possibility of Scenario 2 has gone up.

But you now have to consider a possibility of a third Scenario 3.

How would banks (or other asset classes) perform in each of the 3 Scenarios?

I’ve gamed out the various outcomes below:

|

|

Scenario 1 – Hard Landing (recession, rapid rate cuts) |

Scenario 2 -Soft landing (no recession, mild fed cuts) |

Scenario 3 -No landing (economic growth reaccelerates) |

|

Banks |

Bad |

Flat |

Good |

|

Commodities |

Bad |

Flat |

Very good |

|

Industrials |

Bad |

Flat |

Good |

|

REITs |

Depends (rate cuts are good – but rental impact is unclear) |

Flat |

Depends (rental will stay strong, but amount of rate cuts is not clear) |

As you can see, as a bank investor you are mainly worried about a Scenario 1 – Hard landing outcome.

If the probability of Scenario 1 has gone down, and the probabilities of Scenario 2 / 3 has gone up.

Then your expected return of holding the banks has gone up.

After all, this is a scenario where economic growth remains resilient, and we don’t see massive interest rate cuts.

In that scenario banks could do well because (1) no big loan defaults, (2) interest rates while cut, stay high, (3) loan growth picks up.

So that’s the big picture macro view, and probabilities I assign to each outcome.

But.. there are 2 parts to each trade

But there’s 2 parts to each trade.

The first – what is the probability you are right?

The second – how much do you make when you are right, and how much do you lose when you are wrong?

The discussion above was for question 1.

Let’s now discuss question 2.

How much do you make when you are right, vs how much you lose when you are wrong?

Now I discussed how the 3 local bank stocks stack up against each other in a previous article.

To sum up briefly, all 3 banks are pretty much the same, but with different flavours.

Or in Singlish – “same same, but different”.

DBS (with POSB) is the Temasek linked entity and the biggest bank, with (arguably) the best execution.

UOB is the smallest bank, with strong emphasis on South East Asia.

OCBC is somewhere in the middle, but with higher exposure to China because of their acquisition of Wing Hang bank.

|

|

OCBC |

DBS |

UOB |

|

Price (as at 10 Jan 24) |

12.76 |

32.32 |

28.00 |

|

Market Cap ($ billion) |

57.5 |

84.3 |

47.4 |

|

Price/Book |

1.11 |

1.48 |

1.04 |

|

Dividend Yield (annualising latest yields) |

6.2% |

5.9% |

6.0% |

Why OCBC Bank vs DBS Bank vs UOB Bank?

Given what I know today, and based on today’s pricing.

If I were to add a bank position in 2024 – OCBC might be my preferred choice.

Valuations at 1.1x book are not demanding.

And with their commitment to pay out 50% of profits in dividend, you’re looking at about 6.2% annualised dividend yield.

Assuming interest rates are not cut drastically, and we avoid a big economic slowdown, I can see this dividend yield being somewhat sustainable.

No doubt OCBC has a fair bit of exposure to Greater China via their Wing Hang bank acquisition:

|

Loan Book |

OCBC |

DBS |

UOB |

|

Singapore |

41% |

46% |

48% |

|

Greater China |

25% |

29% |

17% |

|

South East Asia |

14% |

8% |

21% |

|

Rest of World |

20% |

17% |

14% |

So I might actually mix in some DBS Bank stock, if I were to do it again today.

Of the 3 banks, DBS has arguably the best execution with a 17% ROE, which is why the market has rewarded them with the highest valuation.

|

|

OCBC |

DBS |

UOB |

|

Quarterly revenue growth (yoy) |

27.7% |

37.1% |

23.8% |

|

Return on Equity (ttm) |

12.8% |

17.0% |

12.4% |

|

Non-Performing Loans |

1.1% |

1.1% |

1.6% |

How much do you make when you are right, vs how much you lose when you are wrong?

But let’s keep it simple.

Assuming I buy OCBC in 2024.

How much do I make if I am right?

And how much do I make if I am wrong?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What is the upside for OCBC Bank? Looking at the 2018/2019 rate cut cycle

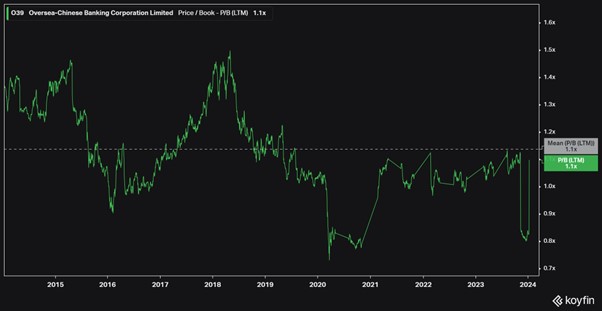

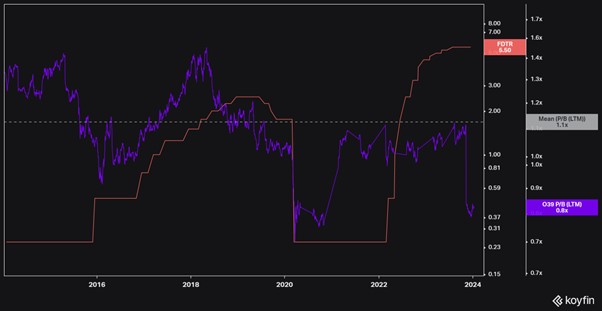

10 year Price/Book for OCBC Bank is set out below.

Now I overlaid this against the 2019 interest rate cut cycle below.

Based on this, OCBC’s share price peaked about 12 months before the first interest rate cut.

And once interest rate cuts actually took place, OCBC’s share price never really recovered to its former highs:

But you may argue this cycle is different…

I know what you’re going to say.

That FH… the 2018/2019 cycle was different because that was still a secular regime of low interest rates, dominated by demand side constraints.

Before COVID came in and smashed everything to bits, and we are now living in a supply constrained world with higher structural inflation and interest rates.

Fair point.

Unfortunately we don’t have any data of how OCBC stock performs in such a world, because the last time this was actually a problem was the 1960s/1970s, and Singapore was a very different place back then.

So let’s reason from first principles.

What is the upside for OCBC Bank Stock if you are right?

- Scenario 1 – Hard landing (economic recession, rapid Fed rate cuts)

- Scenario 2 – Slow Grind Down (economy avoids a recession but stays slow, minimal Fed rate cuts)

- *New* Scenario 3 – No landing (economic growth reaccelerates due to rapid loosening in financial conditions post pivot, further juiced by rate cuts / easy monetary policy heading into elections)

In a Scenario 2 style event, I would say OCBC stays around current price levels, plus or minus a bit.

Throw in the 6% dividend, perhaps 12% total returns over 2 years.

In a Scenario 3 style event, maybe OCBC goes up to 1.2x – 1.3x book value.

That’s a 10% – 20% capital gains.

Throw in the 6% dividend, perhaps 20 – 30% total returns over 2 years.

What is the downside for OCBC Bank Stock if you are wrong?

If you are wrong and we get a hard landing?

Well it would depend on how bad the recession is.

At 1.1x book value, let’s assume a drop to between 0.8x (COVID low) – 1.0x book value.

That’s a 25% – 10% drop.

What is the alternative? What if you just park the cash in risk free investments?

If you just park the cash in T-Bills / money market funds, let’s say you get a 3.5% interest rate over the next 2 years.

That’s a 7% risk free return.

So you do need the adjust the returns above, to determine excess returns vs the risk free rate.

Plugging in all the numbers above, we get something like the below:

|

|

Scenario 1 – Hard Landing (recession, rapid rate cuts) |

Scenario 2 -Soft landing (no recession, mild fed cuts) |

Scenario 3 -No landing (economic growth reaccelerates) |

|

OCBC Excess Returns per year? |

– 12.5% to – 5% |

1.5% |

6 to 8% |

Now bear with me, because I am staying very big picture here.

You may disagree with me on the exact numbers, but big picture wise you would probably agree.

OCBC Bank stock will do great in Scenario 3, okay-ish in Scenario 2, bad in Scenario 1.

So the question I suppose – is what would you assign to the probabilities of each of the 3 Scenarios below, and it this a trade/investment you would make?

What are my views on OCBC / DBS / UOB Bank Stock?

The way I see it, after the pivot in late 2023.

The probability of Scenario 1 has gone down, the probabilities of Scenario 2 / 3 has gone up.

But in Scenario 2 you don’t necessarily make big bucks on OCBC Bank stock, vs just parking the cash in T-Bills risk free.

So you’re basically counting on a Scenario 3 here.

But if Scenario 3 does indeed play out, I can see a lot of other asset classes that may outperform banks.

Commodities for example, could do very well with reaccelerating economic growth.

And if we do get a lot of liquidity in 2024, I can see long duration (REITs, tech, crypto, gold) doing pretty well too.

I’ve already been adding exposure to some of these plays that I think can perform well in a Scenario 3, and FH Premium subscribers can see the full list of what I’ve been buying / keen to add.

|

|

Scenario 1 – Hard Landing (recession, rapid rate cuts) |

Scenario 2 -Soft landing (no recession, mild fed cuts) |

Scenario 3 -No landing (economic growth reaccelerates) |

|

Banks |

Bad |

Flat |

Good |

|

Commodities |

Bad |

Flat |

Very good |

|

Industrials |

Bad |

Flat |

Good |

|

REITs |

Depends (rate cuts are good – but rental impact is unclear) |

Flat |

Depends (rental will stay strong, but amount of rate cuts is not clear) |

Will I buy OCBC Bank Stock at 6.2% dividend yield in 2024?

Long story short – I am less bearish on the bank stocks today than I was in 2023.

In fact I can see myself picking up a position in OCBC in 2024, at the right price.

But the main problem with banks today is that unless you get a Scenario 3, I don’t think the upside is amazing.

And if you get a Scenario 3, you probably make more with other asset classes.

So yes a 6.2% dividend yield looks amazing and all, but this is a regime where you’re getting 3.74% yield risk free on T-Bills.

So that 6.2% dividend yield is only a 2.46% spread vs the risk free rate.

So it’s hard to say banks are a slam dunk investment right here.

What needs to change? To make OCBC Bank Stock a “slam dunk” investment?

Let’s say the price of the bank stocks go down, such that risk-reward improves.

Or if events point towards a higher probability of Scenario 3.

Then it’s a whole different story.

At a high level – I see this regime as fundamentally different from the past decade for the simple reason that interest rates are no longer stuck at zero, and you don’t have money printing at your backs.

In this regime, valuations matter.

I’m less bearish on the banks today than I was in 2023, but I still think I will only add at the right price.

With value stocks like banks / REITs, you really want to get your buy in valuation right, as it has a big impact on future returns.

In any case, I’ll share with FH Premium subscribers the rough target prices I would be looking for, with updates as and when I pick up a position in OCBC (or change my mind).

Closing Thoughts: Howard Marks Memo

I shared on Twitter this week the latest Memo from Howard Marks (do follow me on Twitter if you haven’t already).

The key paragraph is extracted below.

“At present, I believe the consensus is as follows:

- Inflation is moving in the right direction and will soon reach the Fed’s target of roughly 2%.

- As a consequence, additional rate increases won’t be necessary.

- As a further consequence, we’ll have a soft landing marked by a minor recession or none at all.

- Thus, the Fed will be able to take rates back down.

- This will be good for the economy and the stock market.

Before going further, I want to note that, to me, these five bullet points smack of “Goldilocks thinking”: the economy won’t be hot enough to raise inflation or cold enough to bring on an economic slowdown. I’ve seen Goldilocks thinking in play a few times over the course of my career, and it rarely holds for long. Something usually fails to operate as hoped, and the economy moves away from perfection. One important effect of Goldilocks thinking is that it creates high expectations among investors and thus room for potential disappointment (and losses). FT Unhedged recently expressed a similar view:

Yesterday’s letter suggested that we think the market’s current expectation of solid growth and six rate cuts seemed likely to be wrong in one direction or the other: either strong growth will limit the Fed to close to the three rate cuts it currently forecasts, or growth will be weak and there will be as many cuts as the market expects. In this sense, the market does look to be pricing in too much good news. (December 20, 2023)

I don’t have an opinion as to whether the consensus described above is correct. However, even granting that it is, I’ll still stick with my guess that rates will be around 2-4%, not 0-2%, over the next few years. Do you want more specificity? My guess – and that’s all it is – is that the fed funds rate will average between 3.0% and 3.5% over the next 5-10 years.”

I think that’s a fair assessment of where we are in the cycle.

Much uncertainty remains over how the short term economic growth / inflation will play out.

But structurally, it’s hard to deny that last decade’s rock bottom interest rates and non-stop QE are well behind us.

This is a decade of supply constraints.

Of structurally higher interest rates and inflation.

This is a very different investing climate, and requires more active positioning.

But perhaps most importantly, in this regime, valuations matter.

This article was written on 12 Jan 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

WeBull Account – Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Subscribe for Moneybull (the money market fund solution) and maintain for 30 days

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Waiting for scenario 1 this half of the year, we’ll soon know. After that, I think Uncle Sam pumps before the Nov election, scenario 3, everything to the moon!

Big worries for SG banks are:

1) China. I think China is where Japan was in 1989 (or possibly…where the Soviet Union was). I’d choose UOB instead, more of an EM-ex-China play.

2) Financial repression. If we get inflation later, and the Fed can’t raise rates because Federal debt is so high, they may be forced to inflate away their debt instead. Negative real rates. Money lenders and banks get screwed. Then every country (incl. SG) must follow low US interest rates to keep their currencies competitive.

Interesting comment.

On China – agree they have structural challenges ahead of them. I think they have a better chance than Japan did of navigating these challenges though. But let’s see.

On financial repression – I think with recent events the probability of a 1970s style start stop inflation has gone up. This may indeed be a decade where the world as a whole runs low / negative real rates. But let’s see.