At the start of the year, I would usually report how much I spent in the past year. In this post, I will share my spending in 2023.

I learned from somewhere that we would usually allocate our income with this framing:

- Spending for today – These are our current expenses.

- Spending in the past – These are the repayments on the debts we owe.

- Spending in the future – These will be our savings and investments. They are meant to fulfil a life goal in the future, which will require some money.

You can decide how much to spend for today, the past and the future.

There is a tradeoff to saving up money to spend in the future, and we should all recognize that. Unfortunately, some fail to recognize the tradeoff, and they struggle with living life with money.

Reviewing our spending is a way for us to be more conscious about our spending.

Just yesterday, my Singapore Financial Independence Telegram (Join here) discussed a critical and poor take on FIRE. Someone who interacted with more people who retired provided us with the datapoint that most people who retired nearer to the age of 35 have closer to $5 million.

Upon clarification, the biggest reason is not that their recurring spending is always high but that more surprises require more money.

We would eventually agree more that the problem is less of the investments or income side but the variability in spending line items and variability in each line item over time.

Enough of explaining the why of spending breakdown. Let us get down to this and we come back to the conversation later.

My Past Annual Income Spending Breakdown

Updating my spending has become a customary update on an annual basis. Not everyone may be interested. However, if you have that little voice inside wondering why the spending is this way, you might want to take a look at what I blabber about in the last few years:

- 2014: $23,798/yr – A review of my past year’s expenses

- 2015: $22,150/yr – How our family’s $22,150 annual expenses mean for our financial security and financial independence

- 2016: $26,238/yr – My Annual Expense Report – $26,238/yr and its link to Financial Security and Independence

- 2017: $21,723/yr – Annual Expense Report 2017 – $21,723

- 2018: $19,655/yr – Annual Expenses and Financial Security Musings

- 2019: $23,186/yr – Spending Report for the Year

- 2020: $22,464/yr – How I spent $22,464 in 2020

- 2021: $27,680/yr – Annual Expenses Report 2021

- 2022: $39,187/yr – Annual Spending in 2022

In the first 3.5 years, the expenses comprised three adults’ spending. The expenses were spent on two adults for the next 4.5 years. The current spend (not included in the list above) is the spending of one person (me).

I am Changing How I Classify My Spending

At the start of the year, I decided to change how I classify my spending during budgeting. I have stuck with the same spending classification for years.

I want to change because the meaning of each spending to me might be different and reclassifying them would allow me to mentally connect with them better.

This is how the existing classification look like before the change:

- Mandatory Expenses

- Mortgage

- Household

- Family Medical

- Family Survival Groceries

- Transport

- Insurance

- Internet, Cable, Handphone

- Medical

- Tax

- Rich Life Expenses

- Rich food/entertainment

- Gifts

- Hobbies

The spending is split by spending that are more inflexible (mandatory) and flexible (rich life). As I am paying and supporting my parents, much of the spending is rather inflexible and dominates most of the categories. Most of the mandatory spending is family-based, except for some work-related (tax), and transport.

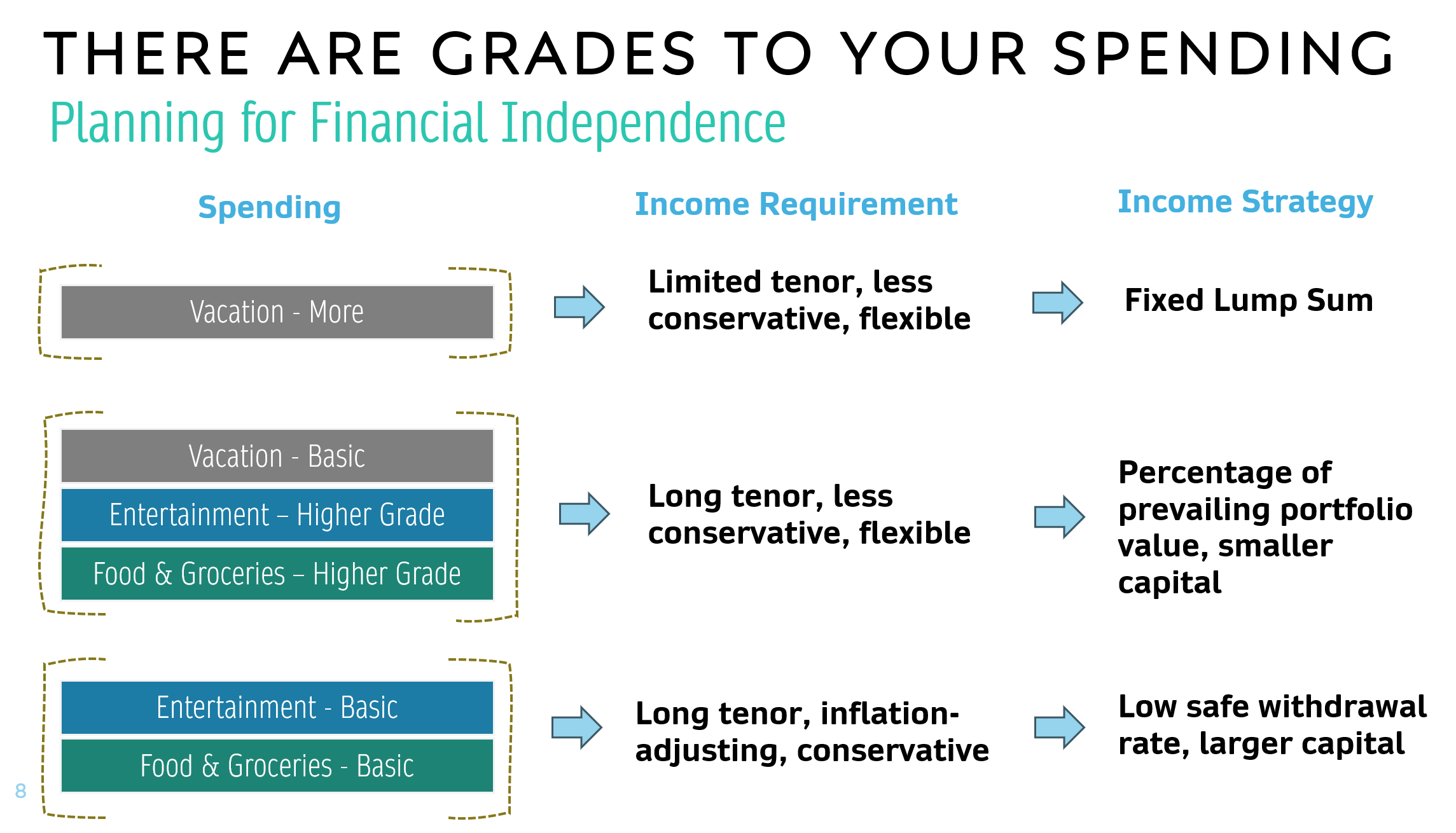

After my dad passed away this year, I reflected for a moment and decided to re-align the categories based on:

- My most essential spending (You can read about them in each article). Most inflexible and needs to be most conservative.

- My basic spending. Often inflexible but the timing of spending can be flexible. Mostly conservative.

- Spending if I work.

- Spending that would come from portfolio sources.

- Flexible spending. Can be adjusted, scale up or down depending on market conditions.

Each spending set has unique characteristics, such as how flexible the income needs to be, inflation adjustment, and how long they need to last. I plan to have individual portfolio to address each unique spending set in the following illustrated manner:

The above is more like an example, not how I want to plan out.

By adjusting the spending category, if I plan for $360 max for the essential food, was that a sound number if we take a look at how much I spend monthly?

I want to have an easier time to review so this realignment helps.

Ok let us take a look at 2023’s annual spending.

2023 Spending – $29,554

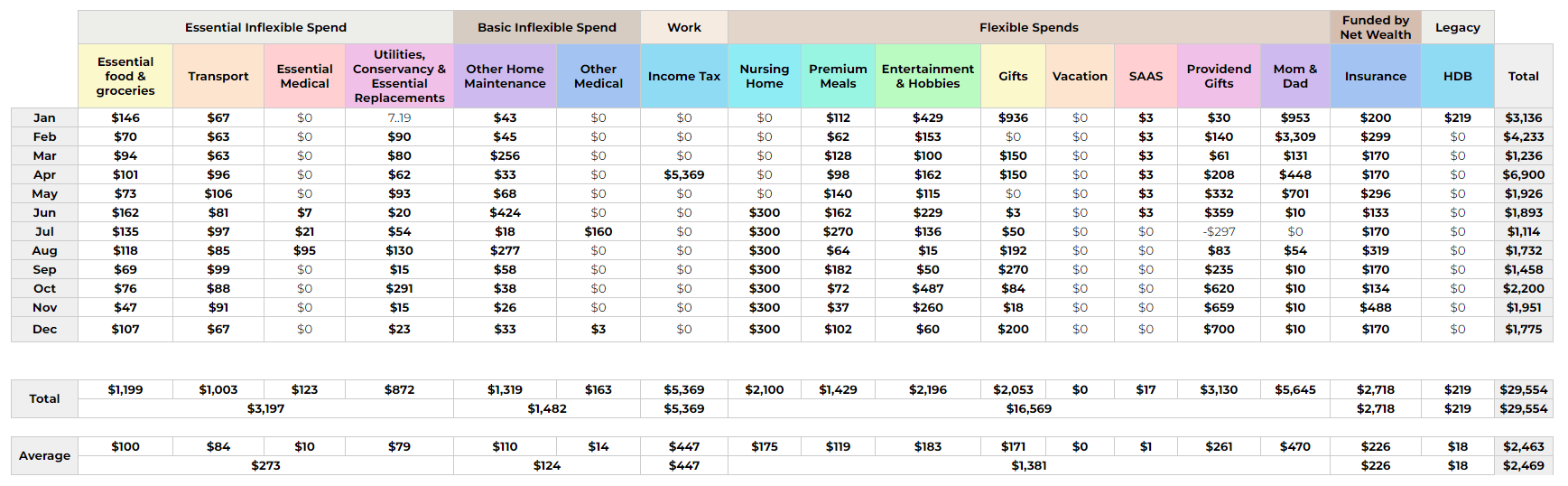

Here is how my spending looks with the new breakdown:

I spent $29,554 in 2023. This is lower than in 2022, when I spent $39,187.

You can see the monthly spending as well as the total and average at the bottom.

I spent less in 2023, mostly because in 2022, I had a caregiver and spent more than usual because my dad was sick. Majority of the spending in 2023 was in the Flexible Spends, which are the spending that are more good-to-have. I can cut down on good-to-have spending if I wish to.

Let us take a look at different groups of spending in greater detail.

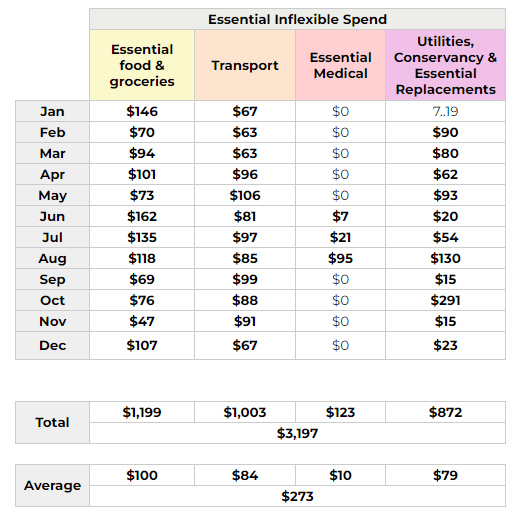

Essential Inflexible Spend – $3,197

The transport cost should average to $90 or $100 monthly. The essential medical is for medical aids that I need to have, not those long-term supplements to maintain longevity. Utilities, conservancy and essential replacements are low because in a few months the conservancy cost is half a month or $39 less. I also didn’t replaced much of either laptop, mobile phone or fridge.

Actually, I did spend $456 on a PC. In hindsight, I should have accounted for the PC under Utilities, conservancy and Essential Replacements, but I put it under flexible categories. If we add this computer, the spend here would be $3.6k instead of $3.2k.

My food cost looks absurdly low and this is because I have some food vouchers during the year. In my F.I. plan I budgeted for $360-$380 monthly but due to these vouchers, my spending for the year never came to that. This year, I won’t have this luck anymore.

The food spending should be closer to $360-$380 monthly this year.

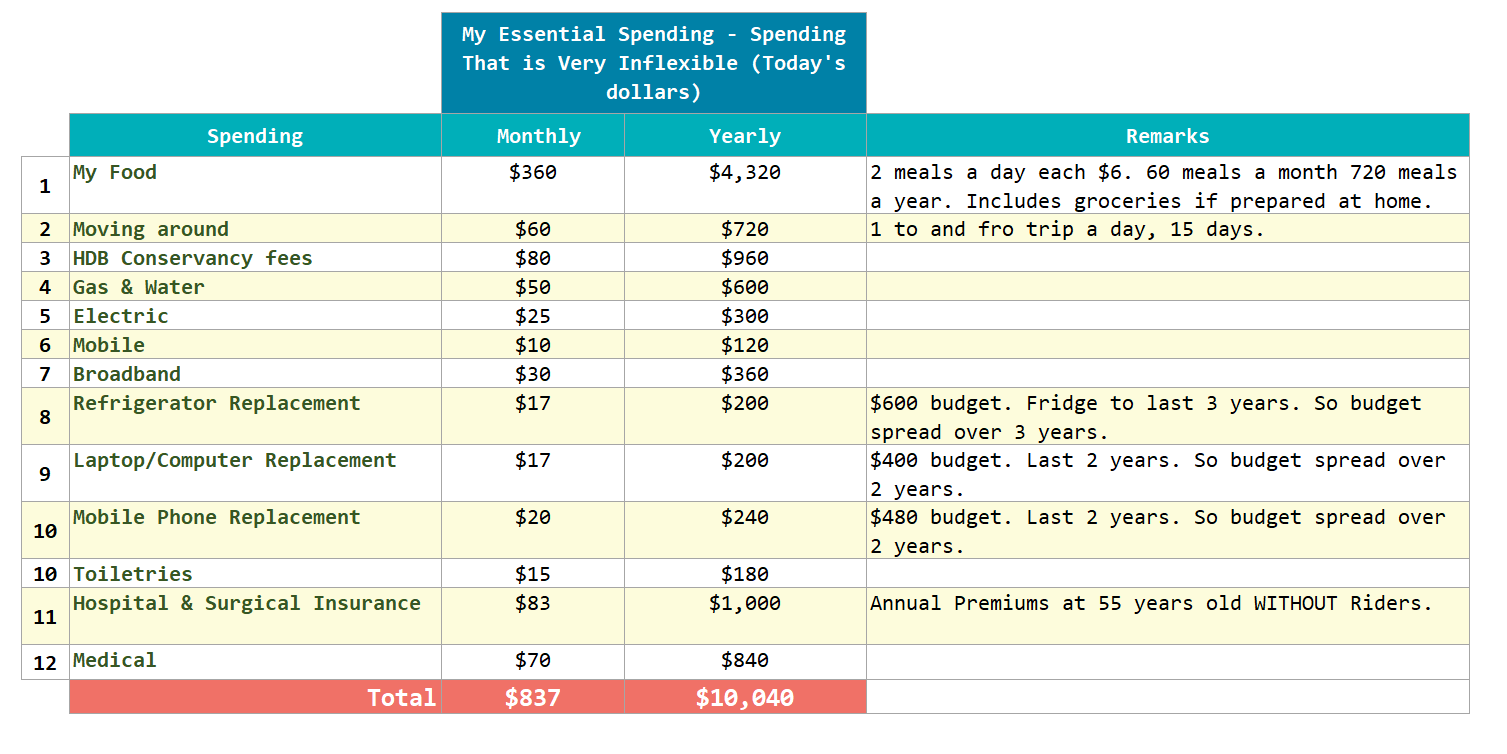

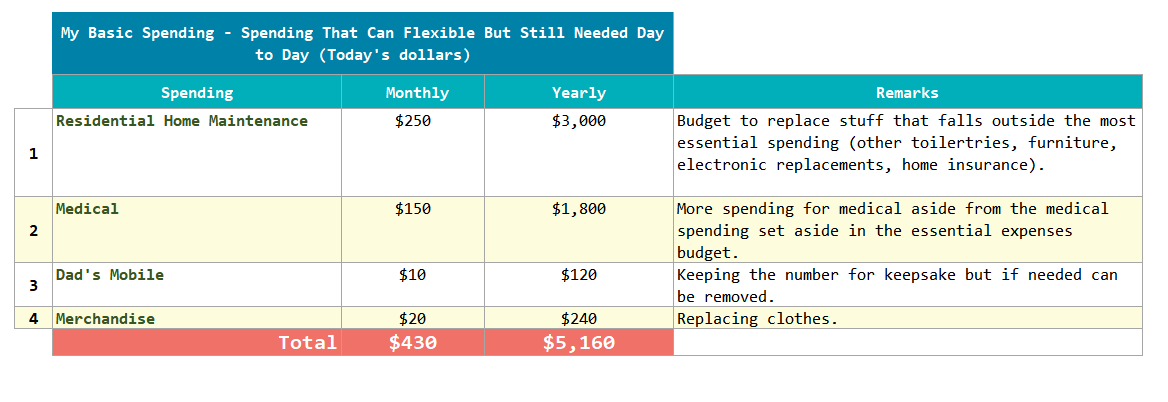

Here is how this looks against my plan in my notes:

My most essential spending is much, much less than what I plan for.

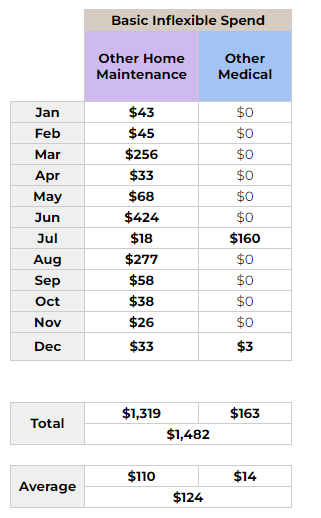

Basic Inflexible Spend – $1,482

I didn’t take much supplementation this year. There was some spending, but it was mainly reimbursed by the company. This has kept the spending low.

I decided to spend a bit on doing a Fengshui audit in June and buying some stuff in August. Those are the larger cost but there were no major breakdowns in the year thankfully.

This was part of my F.I. Plan as stated in my notes:

My basic inflexible spending is well within the limits as well. I decided to set aside $3,000 yearly, and this year, that spending came up to $1,319.

I don’t have to spend all of this. The $1,600 unused will be accumulated in this category, and if they are not spent, they would be enough for larger spending such as paint jobs or some areas of fixing.

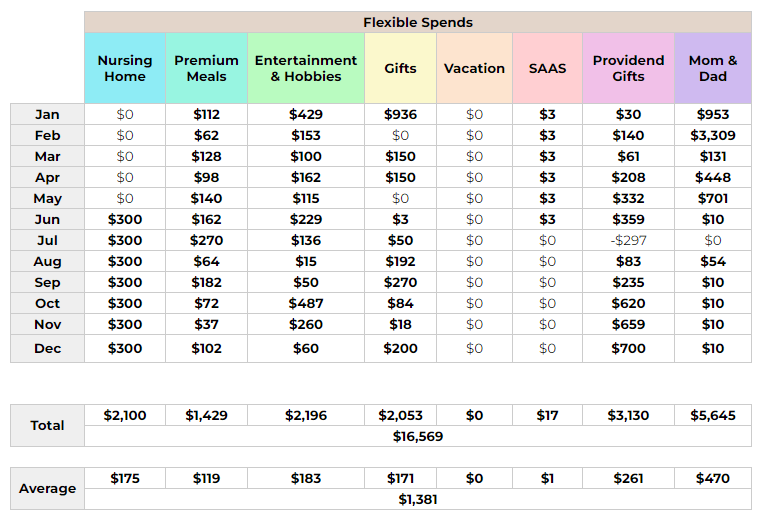

Flexible Spend – $16,569

I spend the most under the Flexible Spends. These are the spending that can be vary up and down if the performance of the portfolio, or work income is more volatile:

I received some proceeds from the white gold for my father’s funeral so net of that, there is still some outflow. There are still outstanding caregiver food and salary cost for about three months. In total, I spend $5,645 on the mom and dad stuff.

I think next year, I am expecting about $400 in total spend for the year.

In June, I decide to contribute part of the cost of housing my grandma in a nursing home and we should see this as an ongoing cost for next year as well.

I spent more this year on a lot of funny stuff under entertainment and hobbies. These are mainly small gadgets, my 4K TV as monitor, and lot of stuff that I cannot remember so well. Here are some of the stuff:

- Minisforum mini PC

- 16 GB Ram

- 8GB Ram

- HAWorth Zody

- 30 inch Dell Monitor

- Anker C2000 2k Webcam

I attended enough funerals and weddings as well as give enough birthday ang baos.

A substantial part of the spending here is also gifts to Providend staff.

I was too busy this year to even think about travelling. Perhaps next year.

I have not noted down my income strategy for my flexible spend in any of the past posts, but observing my spending this year may give me some clues.

One of the income plans is to spend 4-5% of the prevailing value of a 60-70% equity portfolio. The question is, how much?

The flexible is very volatile because:

- The spending line items changes

- The amount that we can spend on changes

I remind myself that it is important I ensure that each spending line item can be flexible and not because I have to reluctantly reduce the spending because the portfolio is not doing well.

I should not feel guilt or shame if I have to cut down or scale up the spending.

I haven’t fully sat down to simulate this, but my past experience with flexible spending tells me that in the worse case scenario, spending can easily be cut to 50% due to the volatility of the portfolio.

I haven’t fully fleshed out how much vacation I would like to take in the year, or how much does it cost, whether I would account for that separately or not but there are a few figures:

- $30,000 a year, which means we need $30,000/0.05 = $600,000

- $40,000 a year => $800,000

Shit.

That is still a lot of money to live a rich life.

I think I should have enough for that, but logistically, tit will mean taking money out from the publish portfolio (which you can see under the current portfolio tab above) and moving it out. This feels like a chore.

We will think more about it.

The Rest of the Spending

The rest of the spending includes:

- Income Tax under Work

- Insurance Premiums under Funded by Net Wealth

- HDB mortgage under Legacy

My income tax is a function of work and blog income. If there are inflows, this is a necessary outflow. Don’t have to think about it so much except to have enough liquidity to pay for it.

I have set aside capital to pay for future insurance premiums so that won’t come from the salary. You can read about it at Cutting My F.I. Capital Needs for Insurance Premiums from $131,366 to $58,132 by Prepaying for It.

I paid off my parent’s HDB fully a month before my dad passed away. No more mortgage.

How this Year’s Spending may Change

It is quite confirmed that the essential food & groceries spending should go up. Income tax should stay the same. Utilities, Conservancy and essential replacements should stay the same as other home maintenance. We should see higher nursing home spending, entertainment & hobby spending, gifts and vacations.

The aim is for flexible spending to be closer to $40,000 to $60,000 instead of just $16,000.

The plan is that all income should not be allocated to future spending but for today.

The Importance of Spending Consciousness

I put out spending breakdowns like this, with my thoughts about it, to help you think about how you allocate your income.

You don’t have to do it my way. I am not trying to flex that I don’t spend much.

One interesting thing we learn over time is how life changed in these ten years of tracking. I provided for 3.5 people, then 3 people, then 2 people and finally 1 person. There used to be a mortgage, and now it’s no more. There used to be not much gifting, and now there is more.

I think some of your life journeys might show as much spending line item variability and variability in the amounts.

The spending definitely does not go up by 3%, 3%, 3% per year in inflation or adjust based on CPI.

What people struggle with is trying to wrap their heads around this as they plan for a traditional retirement or their financial independence.

Do we track all our spending and make sure we have an income to cover ALL of it but with at least a 30% buffer? For example, if you look at this sharing, the highest spend is $39,000 and with a 30% buffer that means I plan for $55,700 annually. Then, the question is how sturdy we want the income to be. Can we be flexible with the $55,700? If we can, we can use a higher initial safe withdrawal rate such as 4-5% as an estimate or if we want it to be more certain, a 3% would be better. The difference is either $1.4 million or $1.85 million.

But if my spending in 2024 is $75,000 a year because I want to travel more, does that mean the $1.4 -$1.8 million strategy goes to shit?

Conscious spending is not just about tracking spending. It is about

- Understanding the importance of the spending line item to your family

- Whether you can do without the spending line item if you don’t have enough money

- Do you spend on that spending line item forever, or do they come to an end?

- Are you spending on a line item because of work? What happens when you do not work?

- Does particular spending line item spark joy?

- Are you spending on this line item as a consequence of being stressed at work or with the family?

I don’t think you do not know, just that you don’t spend enough time sitting by yourself or with your spouse to reflect over this. This is your exercise and not mine.

Answering these questions will help you determine the following income characteristics:

- The tenor of the income needed.

- How conservative do you need the income to be?

- The degree of inflation adjustment.

This is basically this diagram again:

If you are conscious, I will give you a well-optimized income plan. If you are unconscious, I am going to tell you that you need $3-5 million in today’s dollars. Again, this has got nothing to do with your investment returns or the structure of your investment portfolio.

I believe the lack of clarity breeds anxiety in people’s minds when the volatility of the portfolio rises.

We revisit this in a year’s time.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024