So I took the opportunity with the recent rally in REITs prices to take profit in some of my REIT positions.

Especially those REITs I didn’t see myself holding long term, and where I thought valuations were a bit stretched (fuller details shared on FH Premium).

This left me with a bit of spare cash, that I was looking to redeploy into new REITs.

Keppel DC REIT is one of those REITs I have been monitoring for a while now.

I first wrote on Keppel DC REIT a couple of months back, but quite a few things have changed since – so I wanted to take a refreshed look at this data centre REIT.

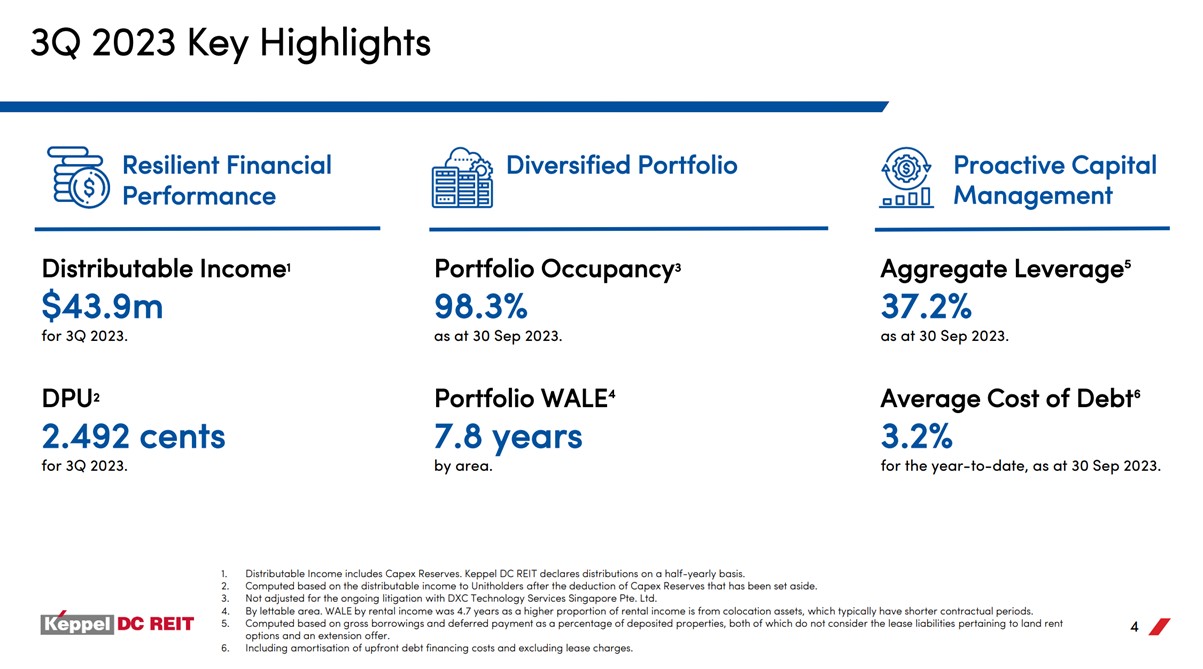

Keppel DC REIT at $1.8 pays a 5.5% dividend yield – for 54% Singapore Data centres

Keppel DC REIT trades at $1.8 today.

If you annualise the 2.492 cents quarterly DPU.

That gives you a 5.5% dividend yield.

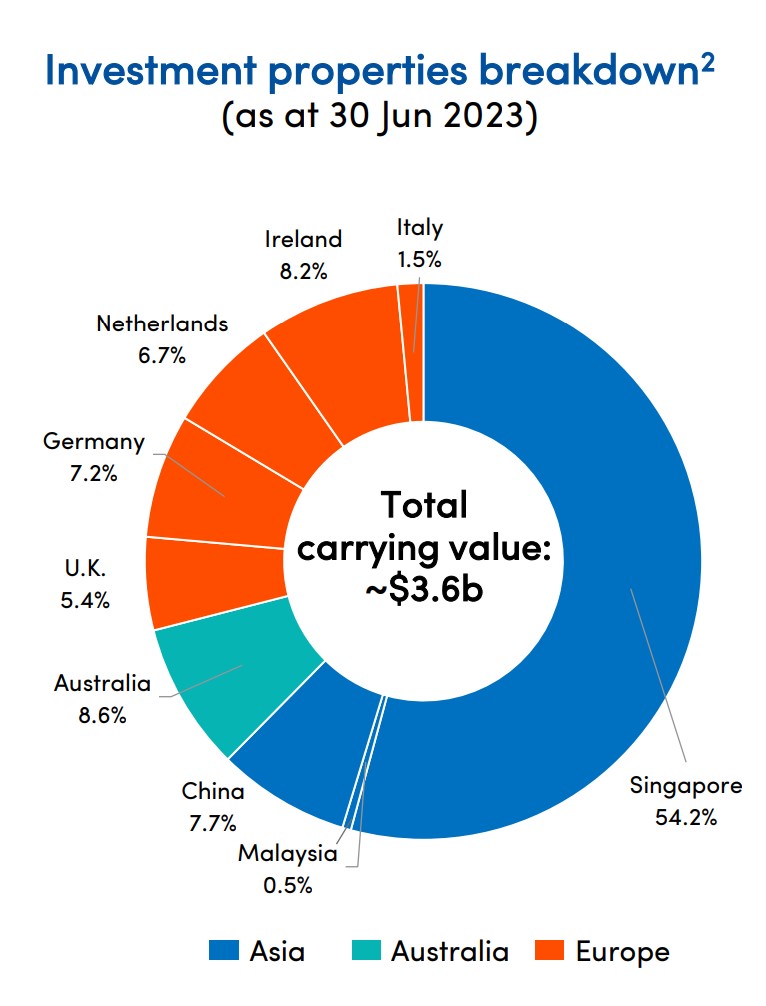

Note that this is a data centre REIT that has 54% of its asset base in Singapore, so you would expect it to trade at a “premium” valuation because of the scarcity and highly sought after nature of Singapore data centres (supply is tightly controlled by the Singapore government due to power demands).

So you can’t really compare Keppel DC REIT to something like Digital Core REIT (or even Mapletree Industrial Trust), as US data centres are a completely different beast from Singapore data centres.

Why has Keppel DC REIT’s share price been dropping?

In my original article, I shared 3 key concerns specific to Keppel DC REIT:

- Financial Difficulty of Keppel DC REIT’s big tenant

- Potential Dilutive Acquisition by Keppel DC REIT

- Institutional Sales

Has anything changed since?

Financial Difficulty of Keppel DC REIT’s big tenant

Back then, the concern over the default by one of Keppel DC REIT’s larger tenants was mainly still speculation.

However, this is not speculation anymore.

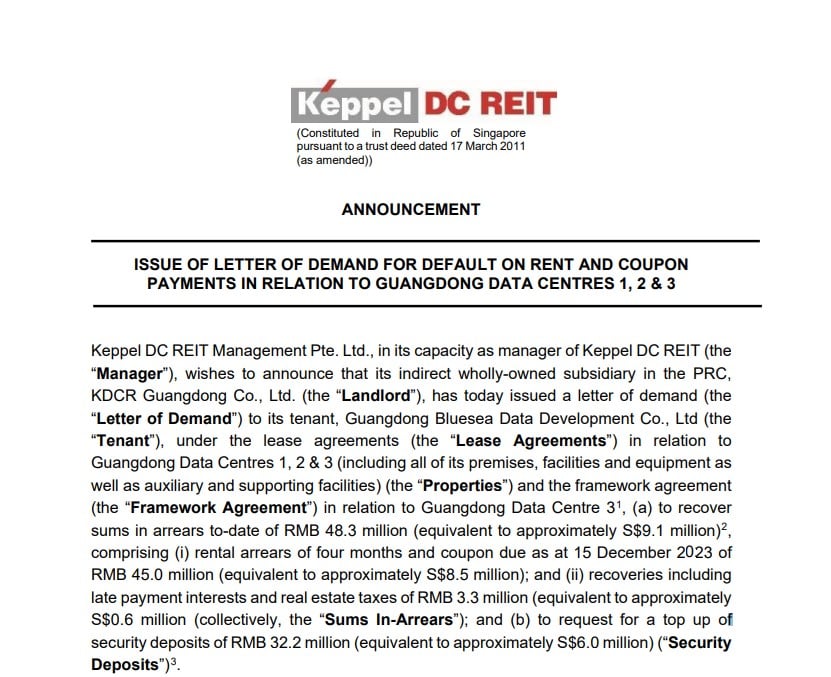

In Dec 2023, Keppel DC REIT issued the following announcement:

“The Landlord is and has been in close discussion with the Tenant and had at the request of the Tenant agreed to instalment payments and top up of security deposits. The Tenant performed its obligations in relation to such instalment payments up to October 2023, but the latest payment that was due in end November 2023 was not duly paid.”

Long story short – the Guangzhou tenant had paid rent up to October 2023.

But the November 2023 rent was not paid.

And so Keppel DC REIT issued a letter of demand for the unpaid rent.

What is the potential impact to the REIT if there is a true default by the tenant?

The Properties contributed approximately 8.5% of Keppel DC REIT’s Gross Revenue for the third quarter ended 30 September 2023. On a full year basis, if the rent, coupon, and recoveries in relation to the Properties as at 31 December 2023 cannot be recovered, it is estimated that there will be a negative impact on Keppel DC REIT’s FY2023 distribution per unit (“DPU”) of approximately 0.655 cents, an amount representing 6.4% of Keppel DC REIT’s FY2022 DPU

A whopping 6.4% DPU impact.

If realised, this could cut the 5.5% dividend yield down to low 5%.

This is big, and you can understand why the market reacted in this way.

More information on the tenant in question – Neo Telemedia:

Neo Telemedia, the master lessee of KDC REIT’s data centres made a net loss in 1HFY2023 for the six months ended June… Neo Telemedia reported a loss of HK$123.7 million or a loss per share of 1.3 HK cents for the six months to June 30. This compared with a net profit of HK$40 million in 1HFY2022. Interestingly, Neo Telemedia recorded both positive operating cash flow and free cash flow.

However, on the bank loans and debt front, Neo Telemedia has some HK$842.7 million of loans (of which HK$548 million are bank loans) categorised as current liabilities, which are generally payable within a year.

According to the financial report for 1HFY203, Neo Telemedia states that HK$500.4 million of loans were guaranteed by property, plant and equipment (PPE) with net book value of HK$161.9 million. Neo Telemedia has HK$14 million in cash and its net assets stood at HK$836 million.

So generally speaking the picture doesn’t look good – the tenant looks to be in real trouble.

Sure, you could argue that Keppel DC REIT will eventually find a replacement tenant, and China exposure is only 7.7% of the REIT.

But there would still be lost rental during the transition period to the new tenant.

And all the uncertainty would hang over the REIT in the short term, pressuring share price.

Not a good development for Keppel DC REIT.

Potential Dilutive Acquisition by Keppel DC REIT

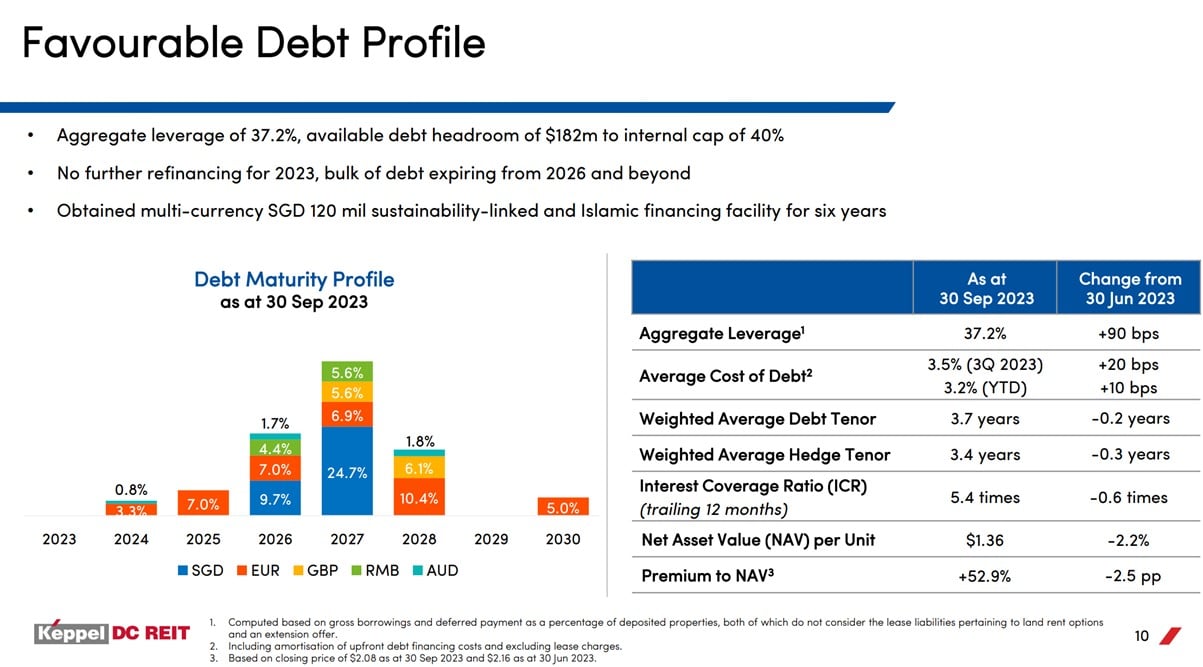

Keppel DC REIT is running 37.2% leverage.

That’s an acceptable level, and I would only start getting worried if it goes to 40% and beyond.

But if Keppel DC REIT were to do an acquisition, they will need to fund it either via debt or equity.

This would mean either (a) bring gearing up to dangerous levels, or (b) a dilutive equity fundraise.

So if Keppel DC REIT were to do an acquisition in this market, I would be pretty worried about the market price reaction.

So far at least, Keppel DC REIT hasn’t announced any acquisition, and let’s hope it stays that way.

What about the macro climate of higher interest rates?

To be fair to Keppel DC REIT – almost every REIT in the market is facing this exact same dilemma today.

They can’t do an acquisition because debt is expensive, and they can’t raise equity because share price is depressed.

Everyone is just trying to hold on and hope interest rates come down to bring relief.

But when will relief come?

What is the interest rate outlook for 2024/2025?

It’s probably worth taking some time out to discuss the interest rate outlook going forward.

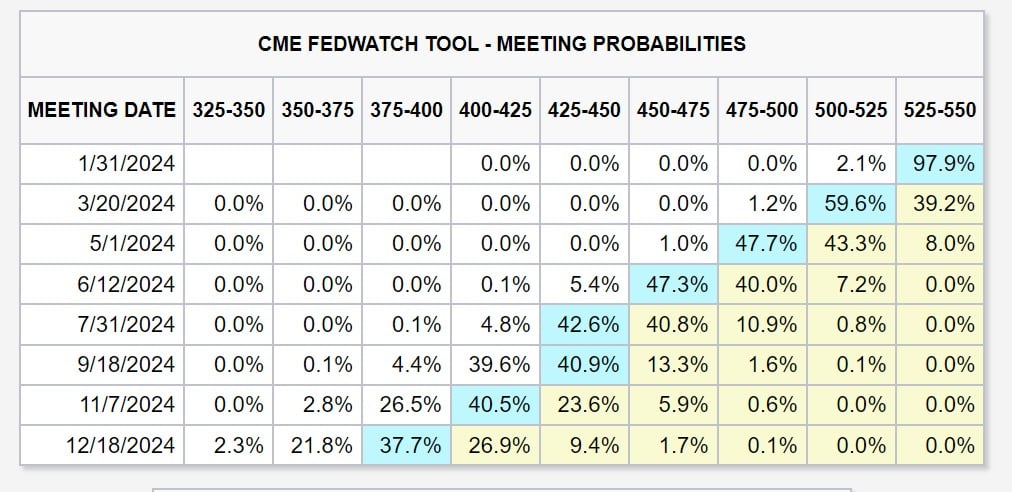

After the Fed “Pivot” in Dec 2023, the market rapidly moved to price in 6 interest rate cuts in 2024.

This led to a huge rally in assets across the board.

But it’s a bit of a chicken and egg.

Because if market prices in easing financial conditions too early.

That would allow economic growth to pick up, and inflation to pick up – which prevents the Feds from cutting interest rates to the extent the market expects.

And that’s exactly what Fed speakers have been trying to communicate.

After the speech from Fed member Waller this week, the market started to wake up to this reality.

Probability of a March interest rate cut has come down, but the market is still pricing in 6 interest rate cuts in 2024:

My personal view on interest rate outlook?

As you would have seen by now.

This interest cycle is proving to be anything but conventional.

And market pricing (on interest rates) has proved to be consistently wrong for much of the past 24 months.

So if the market is pricing in 6 interest rate cuts in 2024, I think there’s a good chance this is going to be wrong as well.

Think about it this way – if the economy stays strong, is there really a need for the Feds to cut interest rates 6 times this year?

Whereas if the economy weakens rapidly, yes the Feds will cut more than 6 times – but how would risk assets perform if the economy is weakening rapidly?

So my concern here is that market pricing may be slightly too optimistic, and odds are we will either see more/less interest rate cuts than priced in.

My money for now might be on less, but I will be guided by the economic data for this one, as are the Feds.

Institutional Sales of Keppel DC REIT

The final point is heavy institutional sales of Keppel DC REIT

You can see how Keppel DC REIT sold off in very high volume in late Oct and Dec, after news of the tenant bankruptcy came to light.

Sell-offs on high volume are never a good sign.

And technicals wise – the REIT has been in a downtrend since July 2023.

So all this is quite bearish in the short term.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

What about higher electricity costs?

Some of you have asked whether Keppel DC REIT would be affected by higher electricity costs.

The general rule for data centres is that:

Electricity expenses of data centres are largely pass-through in nature. The electricity expenses of colocation data centres are borne by tenants. Tenants of the long-lease data centres (fully-fitted as well as shell and core ones that provide income stability) negotiate the electricity expenses — including any increases due to commodity prices — with electricity providers directly.

So the REIT shouldn’t be so exposed to electricity prices, but of course high electricity prices likely mean high inflation which has impacts on interest rates. So the factors are somewhat interlinked.

What about AI Tailwind? Higher demand for data centres?

We all know the bull story for AI by now.

AI is going to transform the world, and it is going to drive massive data centre demand.

Therefore data centres should benefit?

The reality though, is a bit more nuanced, for 2 key reasons:

- AI data centres have different technical requirements from normal data centres

- AI research (for now) is mainly confined to US/China

AI data centres have different technical requirements from normal data centres

Without going into all the technicalities.

AI data centres consumer much more power than normal data centres.

This requires data centres that are able to handle much higher power draw, and more efficient cooling systems.

So it’s not as simple as taking an existing data centre and throwing in AI chips.

Significant upgrading costs are required to retrofit a normal data centre for AI.

So it’s not so clear if Keppel DC REIT’s data centres are “AI Ready”.

AI research (for now) is mainly confined to US/China

For now, AI data centre demand in mainly confined to US and China.

Yes, this has benefitted data centres in the US and China.

And you may argue REITs with US data centres like Digital Core REIT or Mapletree Industrial Trust stand to benefit.

But Keppel DC REIT’s assets are primarily located in Singapore.

Does Singapore have the same AI tailwinds as the US or China?

Not so clear.

What about rental growth for Keppel DC REIT?

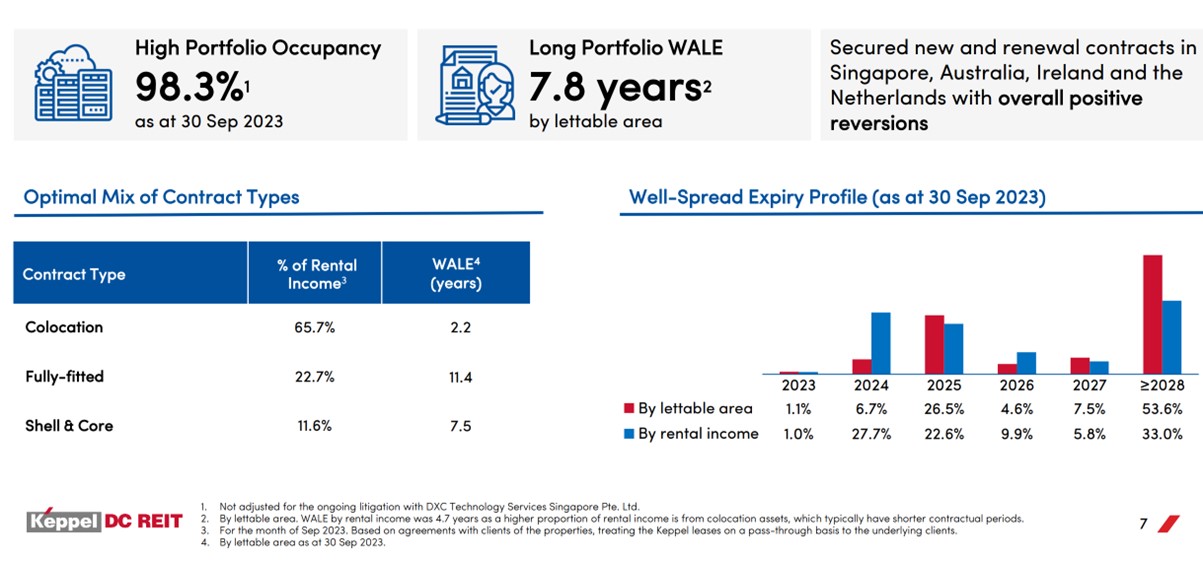

Net property income growth is 3.3%, which is not too bad.

Now you may look at the REIT’s 7.8 years WALE and argue there is little room for Keppel DC REIT to raise rents.

But it turns out the 7.8 year WALE is calculated by lettable area.

If you look at rental income instead, then 65.7% of the REIT’s leases have an average duration of 2.2 years.

This means there is quite a lot of room for the REIT to renegotiate rentals based on market rents.

What are the rental reversions you ask (rental reversion tells you how new rents compare vs old rents).

This is what was disclosed by Keppel DC REIT:

“Secured new and renewal contracts in Singapore, Australia, Ireland and the Netherlands with overall positive reversions”.

Boy… what a disclosure.

I know that there are commercial reasons for not disclosing specific rental reversions (as it may jeopardise negotiations with tenants).

But as an investor, I would really like to know if the new leases are getting signed at 10% rental increases, or 1%.

Long story short – if market rents for data centres goes up, Keppel DC REIT can benefit.

But there’s not a lot of clarity on how much rents will go up by (if at all).

What is a “fair” valuation for Keppel DC REIT?

I’ve been going on and on about how in this new regime of higher structural interest rates and inflation.

Valuations matter.

When you buy at lower valuations, you improve your probability of making money.

So what is a “fair” valuation for Keppel DC REIT?

Annualised net property income is $258 million.

Taking the current $3.2 billion market cap, and adding back the $1.5 billion debt, gives us a property valuation of $4.7 billion.

This means that at today’s price, you are buying Keppel DC REIT’s property portfolio at a 5.4% blended cap rate (in plain English, for every $100 you put in you get $5.4 in net rental income back each year).

For a REIT with 54% exposure to Singapore data centres, and 29% exposure to European data centres.

Roughly speaking – You could be looking at 4.0% cap rates for the Singapore portfolio, 7.0% cap rates for the rest of the portfolio.

Even if you assume a long term 10 year Singapore government bond yield of 3.0%.

It’s hard to say current valuations are a screaming buy / bargain basement discount.

But I suppose you do have to acknowledge that Singapore data centres are a rare and prized asset class (because of lack of supply – Singapore government tightly controls construction of new data centres due to excessive power demand).

And because of that, I would say current valuations of Keppel DC REIT may be in a “fair” range.

Why I may buy Keppel DC REIT at 5.5% dividend yield? (as a Singapore Investor in 2024)

Macro wise, there is no doubt that what lies ahead is interest rate cuts.

So macro wise, I think this is the part of the cycle where I look to increase exposure to REITs.

You can see the full list of REITs and stocks I am looking to pick up on FH Premium, which I will update this weekend given the large changes in prices these few weeks.

The debate now, is how quickly the interest rate cuts will take place.

There is a chance the market may be too aggressive on pricing, so some short term caution is warranted.

The short term picture for Keppel DC REIT isn’t pretty as well.

The potential bankruptcy of a large China tenant has the potential to hit 6.4% of their DPU, and will hang over the REIT short term.

Charts are not pretty either, and show the REIT in a downtrend, with sell-offs on high volume.

Long story short, I like Keppel DC REIT for its 54% exposure to Singapore data centres.

Unlike where it was in 2021/2022, valuations have come very much down to Earth, and are somewhere in fair value range today.

Because of that, I can well see myself picking up a position in Keppel DC REIT as 2024 plays out.

What is the exact price and timing I would buy – will depend on how markets play out.

I will provide an update on FH Premium as and when I buy a position, or if I change my mind on Keppel DC REIT.

I will be updating the Stock / REIT watchlist for FH Premium subscribers this weekend, on the Stocks / REITs I am keen to pick up (and approximate target pricing).

With the recent Fed pivot and changes in asset pricing, I think there are interesting opportunities for long term investors.

Full list on FH Premium if you are keen!

WeBull Account – Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Subscribe for Moneybull (the money market fund solution) and maintain for 30 days

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.