As promised, I wanted to share some updated thoughts on the events this week.

This week was an absolutely massive week from a macro perspective.

The 5 crucial events were:

- Federal Reserve’s FOMC (Wed)

- Treasury Quarterly Refunding Announcement (QRA) (Wed)

- FAANG Earnings (Wed – Fri)

- Fears over US Commercial Real Estate Loans (Wed/Thurs)

- US Jobs report (Fri) – very strong jobs report reduces likelihood of March rate cuts (although cuts still coming in 2H 2024)

I explain each of the 5 in further detail below, so feel free to jump straight to the discussion.

But at a high level, this is how I saw the 5 factors playing out this week.

How did this week play out for bonds/REITs (interest rates)?

The way it played out this week for bonds, was that:

Wednesday/Thusday – even though (1) and (2) were bearish, market focussed heavily on (4), in the belief that (4) would lead to rapid easing in monetary policy.

This is why US interest rates dropped despite all the bearish news.

Friday – this changed after the monster US Jobs report. After the jobs report, market recognised rate cuts in March are unrealistic, hence the huge jump in US interest rates.

How did this week play out for stocks?

For stocks it appears to be primarily driven by earnings.

It dipped on Wed after the poor earnings from Google, and the bearish news from the Fed/Treasury/NYCB generally.

But the stronger earnings on Thurs/Friday drove equity prices up.

What drives REIT prices vs stock prices in 2024?

At a high level, this may be instructive for what might drive REIT and stock prices this year.

Interest rates (and Bond / REIT prices) will be driven by the Fed’s ability to cut interest rates in an election year. Which itself depends on US inflation, which is itself driven by the US labour market, and the general strength of the US economy.

Equity prices though will be driven primarily by earnings. Given that the peak in interest rates is likely behind us, the headwind from monetary policy is removed. The key differentiator going forward for equities might be earnings.

AI the only story in equities?

And for now, the overwhelming story in equities looks to be AI.

Even after a bad earnings report for AMD this week, the stock barely even skipped a step as investors looked through to all the potential AI demand to come.

Are we getting into bubble territory for AI?

Well I made the mistake of selling NVIDIA too early in 2023, a mistake I was keen not to repeat with AMD.

But with my AMD position now ballooning to close to 10% of my portfolio size, I do wonder how long can AI stocks continue to go up parabolically.

Let’s see.

I set out the fuller analysis on each of the 5 factors below (updated with news up to Friday), for your reference.

This is a FH Premium article first released on Thursday this week. I am releasing it to all (with some updates) in the hopes that it may help you in your decision making process.

If you find articles like these helpful, do sign up for FH Premium for more premium macro articles like this.

You can also get access to my personal stock / REIT watchlist (with price targets), and my full personal portfolio.

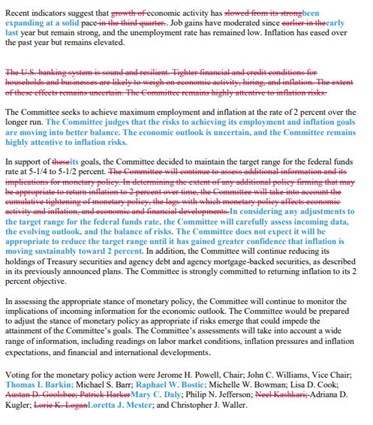

Federal Reserve’s FOMC

To sum up Jerome Powell’s press conference in 2 points:

- All but confirmed that rate cuts will begin in 2024

- However pushed back on the probability of March rate cuts – “Based on the meeting today… I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting to identify March as the time to do that. But that’s to be seen,”

How to interpret this?

The problem with the Fed’s prematurely announcing their “Pivot” in Dec 2023 was that the market was very quick to price that in.

And we’ve discussed before how the market pricing this in will have impacts on economic growth, and consequently inflation.

It’s kind of a lesson why central bankers don’t “leak” news of what they plan to do.

Because once they do so, the market frontruns them, which is counter productive.

So what we saw from Powell yesterday was him trying to undo some of that damage from Dec.

To say that a March 2024 rate cut is not as likely as the market is pricing in (to prevent market from getting too bullish), while also confirming rate cuts in 2024 (to prevent market from getting too bearish).

That said – Given the market was pricing in a rate cut in March, this should be interpreted as short term bearish.

Update – Interestingly, Jerome Powell will be appearing on CBS News’s 60 Minutes this Sunday to discuss inflation risks, expected rate cuts and the banking system, among other topics. You would expect the only reason why Jerome Powell agreed to do this interview is because he thinks the inflation fight is under control, and he wants to talk about how good a job the Fed had done.

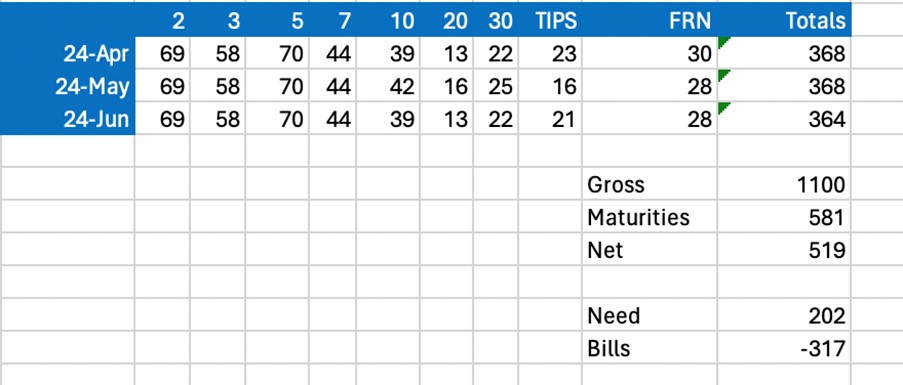

Treasury Quarterly Refunding Announcement (QRA)

Let me first explain what exactly was announced, then we’ll discuss the implications.

The Treasury QRA sets out how the US government will fund their budget for the next quarter.

How much short term T-Bills do they issue, vs long term government bonds.

What they announced yesterday, was that for the next quarter, they would:

- Issue lesser T-Bills – $317 billion less than previous quarter

- Issue more long term government bonds – $519 billion total ($170 billion more than previous quarter)

Why does this matter?

This matters because while there is a lot of demand for short term T-Bills, there is much lesser demand for long term government bills.

The dynamics is similar to Singapore.

If you’re getting 5% yield on risk free 6 month US T-Bills, there is a boat load of demand.

If you’re getting 3.8% yield on a US Treasury that you have to hold for 10 years, and you have no clue what the US budget deficit or inflation will look like over the next 10 years, that makes you a lot more nervous.

What the Treasury did in late Oct 2023 was to issue less long term bonds, and more short term T-Bills.

Less supply means higher bond prices and lower yields – hence the huge rally in US10Y yields from 5.0% to 4.0% after the QRA announcement (in Oct 2023).

What was announced by the QRA yesterday in some way reverses the October announcement.

By issuing less T-Bills and more government bonds, this would place upward pressure on long term US interest rates going forward.

And by issuing less T-Bills, it would mean a slower rate of drain on the reverse repo – which means no change to Quantatitive Tightening for now.

Long story short – this means less money printing in the short term and therefore short term bearish (although you could argue this is setting us up for the big money printing in 2H 2024 heading into the US elections).

What else?

So both the news from the Fed and the Treasury was bearish last night, and undoing some of the “Pivot” in late 2023 (should have caused interest rates to go up, and stocks down).

Why then did US interest rates drop so sharply last night?

It came down to the last 2 factors:

- FAANG Earnings

- New York Community Bancorp – the bank that bought out failed Signature bank last year

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

FAANG Earnings

This one was a mixed bag.

Google’s earnings were not great, which led to a weak market on Wed.

Then Meta, Microsoft, and Amazon delievered a strong set of earnings (especially Meta with the new dividend and share buyback), driving the stock recovery.

Fears over US Commercial Real Estate Loans (Wed/Thurs)

New York Community Bancorp – the bank that bought out failed Signature bank last year

But perhaps more interesting was the unknown unknown.

Here’s the reporting from FT:

NYCB had been seen as one of the winners of the 2023 crisis that sank Signature, Silicon Valley Bank and First Republic. The suburban New York-based institution last March acquired most of Signature’s deposits and just over a third of its assets including nearly $13bn in loans, in a deal arranged by the Federal Deposit Insurance Corp.

Investors at the time propelled NYCB shares higher.

Those gains were completely erased after NYCB reported its fourth-quarter results on Wednesday. The regional bank lost $260mn in the final three months of 2023, down from a gain of $164mn in the same quarter a year before. The bank blamed in particular a rise in expected loan losses, many of which emanated from loans tied to office buildings, bank executives said.

If you recall, New York Community Bancorp was the bank that bought out failed Signature bank last year, in what everyone thought was a great deal.

Last night changed all that, as NYCB:

- Took a $552 million loan loss provision due to troubled real estate loans (raising fears over the state of the real estate loan situation in US)

- Slashing the dividend by almost 70%

Japan’s Aozora Bank

Literally the next day – Japan’s Aozora Bank announced taking a huge hit on its US Commercial Real Estate exposure.

This was despite announcing back in November that they didn’t need additional reserves.

In fact they cut the value of some of their CRE loans by up to 50%!

Share price just imploded after that – down 34% this week.

Just how bad is the US Commercial Real Estate market?

Had it just been NYCB, you could have said it was a one-off.

But 2 banks reporting big losses on US commercial real estate exposure in a row?

It raises the question of how broad this exposure is, and who else is “swimming naked”.

Interestingly the Fed Statement this week deleted the paragraph discussing “The US banking system is sound and resilient”.

Coincidence, or something deeper?

Taken together with the weak FAANG earnings, it raises questions over the strength of the US economy, and whether the Feds would cut fast enough to prevent the slowdown.

Whatever the case, the market seems to have placed greater emphasis on this point (4) for now.

After all, a real estate crisis affecting the US banking sector.

That’s just going to be an excuse for more money printing right?

Hence bond yields down.

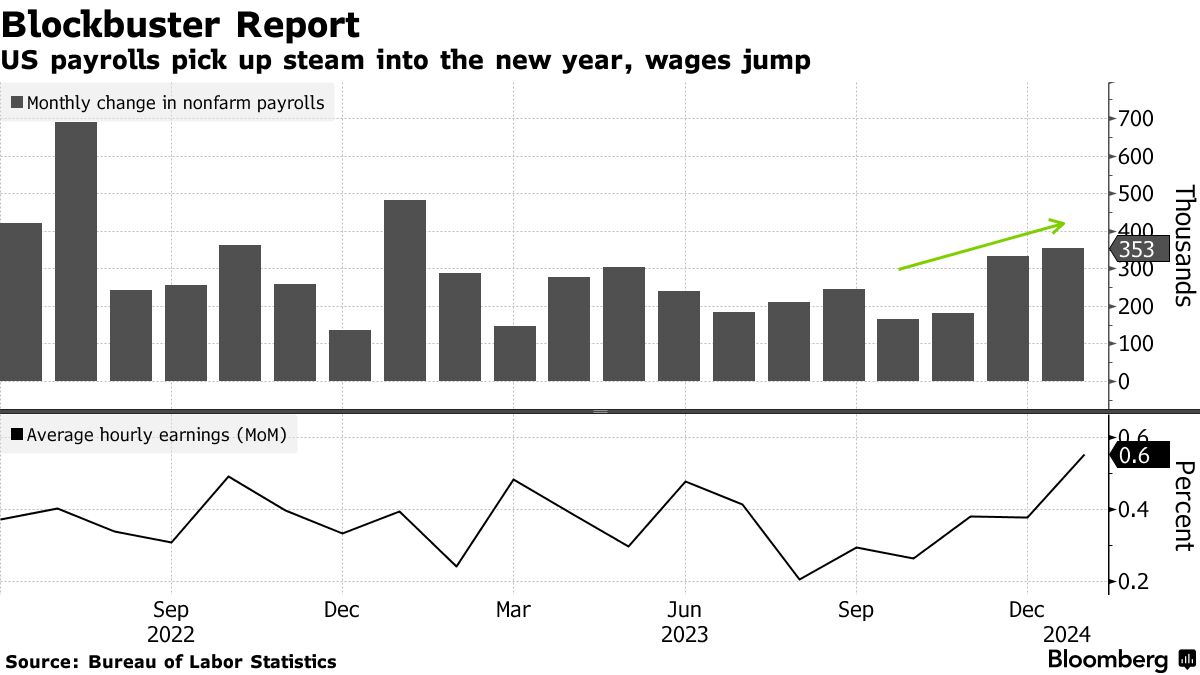

US Jobs Report (Friday)

For much of Wed/Thursday, it was the fears over US Commercial Real Estate loans that dominated the market, leading to a sharp decline on long term interest rates.

And then we had an absolute monster of a US Jobs report on Friday.

Long story short – the US January jobs report outperformed on almost every metric.

Not only that, but the 2H 2023 jobs report was revised upwards.

Given how strong the US jobs market is, a March rate cut is highly unlikely at this point – sending US interest rates sharply up following the jobs report.

Despite the rise in yields, US stocks remained strong due to good earnings results from Meta and Amazon (Meta jumped 20% on Friday alone after announcing a big sharebuyback and dividend).

What happens next? Initial reactions?

Whatever the case, this is just initial reactions, so they may evolve over time.

And I’ll likely do a follow up piece once I’ve had time to digest the information, and watch a bit of the price action.

This is a FH Premium article first released on Thursday this week. I am releasing it to all (with some updates) in the hopes that it may help you in your decision making process.

If you find articles like these helpful, do sign up for FH Premium for more premium macro articles like this.

You can also get access to my personal stock / REIT watchlist (with price targets), and my full personal portfolio.

WeBull Account – Get up to USD 3000 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 3000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund SGD2000

- Maintain until 31 March

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Hi FH,

I am sibeh confused. U been bearish on stocks in almost 2 years of posts. U recommend holding a lot of cash in T-bills. When did u buy AMD??? Why never say u bought AMD? Now say AMD up a lot, why never tell us to buy last year?

I suppose the short answer is that not all positions I take are shared on the public / free version of this site.

In investing – if you make 10 trades and make money on 6 of them, that’s already quite a good statistic. The difference between making / losing money long term, is how you size the trades, how you let your winners run while cutting losers. When to double down on a trade and when to take the loss.

Those concepts are not easy to convey in a 1500-2000 word weekly article.

Which is why I always end each article by saying those are a snapshot of my views as at x date. And I share my full personal portfolio, with weekly updates to positions, on FH Premium: https://www.fhpremium.com/

Those with access to my personal portfolio would know AMD is a position I have been running since 2020. While I made the mistake of selling NVIDIA too early, I was keen not to repeat the same mistake with AMD.

In the spirit of full disclosure – even after the Fed and Treasury Pivot, I am running elevated cash levels as valuations are not sufficiently attractive to overweight equities here. But to be clear, elevated cash does not mean zero equity exposure. There is always something to “play” in markets, as long as risk is managed well.

Not sure if this helps, but trying to share my honest thoughts here.

I’m still bag holding since rate hikes started.

SG listed US reits – MUST Kep Pacific Oak, united hampshire. All double digit returns. So tempting.

But the occupancy rates do not inspire sustainable confidence.

Meanwhile in China, evergrande crisis leads the pack.

The US office situation doesn’t look good, more pain may come before it gets better.

China real estate looks the same as well. These are structural issues that will take time to solve, not a 1 – 2 year solution.