PayPal (PYPL 2.90%) is one of the pioneers of e-commerce, helping to revolutionize how money flows through digital channels. However, over the past several years a number of new services have emerged, giving incumbents a run for their money.

While PayPal is still a leading fintech service for both consumers and merchants, rising competition and a lack of innovation have caused investors to sour on the stock. As PayPal currently sits at a crossroads, some investors might be wondering if it's time to move on.

One analyst on Wall Street isn't convinced that PayPal's best days are behind it. Moshe Katri of Wedbush Securities recently maintained his price target of $85 on PayPal stock, implying a rise of roughly 45% from current trading levels. Let's dig into why Katri remains bullish on PayPal, and assess whether now is a time to scoop up shares at a discount.

Lots of users, and lots of cash

PayPal ended 2023 with 426 million active accounts on its platform. While this was modestly lower than in the previous year, management cleared the air during fourth-quarter earnings by explaining that unengaged accounts in non-core markets comprised the bulk of the churn.

Nevertheless, PayPal's active user base remains highly engaged. Given that PayPal derives the majority of its revenue from fees attached to these payments, it's crucial that the company not only expand its user base, but keep these accounts. Given that total payment volume (TPV) increased 13% in 2023 and eclipsed $1.5 trillion, it's clear that PayPal plays a critical role in the world of e-commerce.

Another positive aspect of PayPal's business is its ability to generate sustained free cash flow. The company reported $4.2 billion of free cash flow in 2023, and forecast $5 billion in 2024 during the Q4 earnings call.

With more than $17 billion of cash and equivalents on the balance sheet, PayPal's financial profile looks quite strong. Let's dig into the company's valuation to get a better sense of just how far the stock has fallen.

Image source: Getty Images.

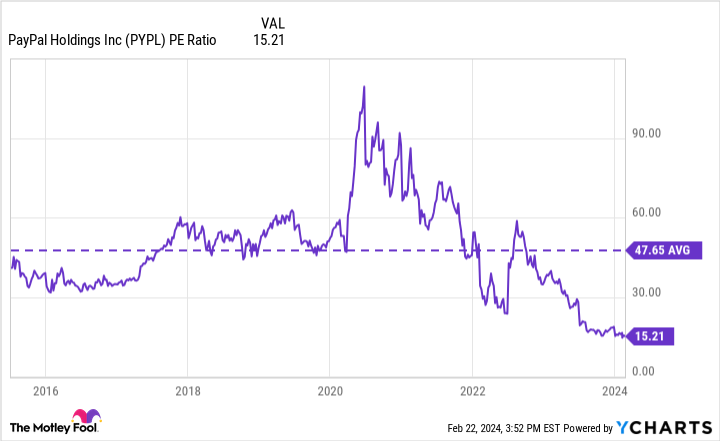

PayPal stock is historically cheap

PYPL PE Ratio data by YCharts

The chart above illustrates that PayPal's current price-to-earnings (P/E) ratio of 15.2 is roughly two-thirds lower than its long-term average since becoming a public company.

It's important to keep in mind that during the peak of the COVID-19 pandemic, PayPal's business experienced unprecedented demand as people flocked to online shopping. However, even in a post-pandemic environment, it seems that PayPal's valuation has dropped off a cliff as opposed to simply normalizing.

It's time to execute

Earlier this year, PayPal Chief Executive Officer Alex Chriss showcased a number of new products and services that PayPal will be implementing. Many of these features will rely heavily on artificial intelligence (AI) and are aimed at better monetizing many of PayPal's acquired properties, such as peer-to-peer payments app Venmo.

On the surface, these enhancements were a much-needed upgrade to PayPal's platform. However, the jury is still out on whether these new products will yield the intended return on investment. Even though PayPal clearly has demonstrated that it can acquire a critical mass of users who are engaged on the platform, it's not totally clear if the company can bolster engagement through these new products.

To me, PayPal has a unique business given its penetration across both merchants and customers. However, I think PayPal hasn't done the best job stitching these two sides together. In some ways, it feels as if PayPal is more of a bespoke digital payments platform as opposed to a true ecosystem -- which I think it has the potential to become.

It's encouraging to see management aggressively deploying capital into new areas for growth. But the precipitous decline in the stock could be a sign that many investors have doubts about PayPal's prospects. With the fintech landscape intensifying quickly, I don't think management has been granted much leeway to prove that its new AI-powered services will change things.

Given that many of the company's innovations are new to market, investors should expect some lag time before they catch on at scale. For now, a prudent approach could be to monitor PayPal's progress throughout the year, and use dollar-cost averaging as you see fit should PayPal's long-term outlook meet your risk criteria.