Property development is a cyclical and lumpy business. The business cycle is long and critically dependent on market conditions at critical milestone.

Performance of presales or tenant take up rate before the project is completed matters. The cost of development can also take its toll as factors such as raw materials, labour costs and interest rates may not be entirely within the control of the developer.

Due to structural changes like work-from-home and ecommerce, many property developers took a hit and are now perceived as cheap and undervalued. Inflation has caused prices of raw materials and labour to increase substantially and the high interest rate environment has added to the toll on the bottom line.

Here we look at 3 Singapore listed property developers that are potentially undervalued and tell you which we think is the best buy.

3 Undervalued Singapore Property Developer Blue Chips Stocks

| SG Property Blue Chip | Ticker (SGX) | P/B | P/E (underlying) | 1 year price performance | 5 year price performance |

|---|---|---|---|---|---|

| City Development | C09 | 0.30 | 27.7 | -22% | -35% |

| Hongkong Land | H78 | 0.22 | 9.7 | -27% | -56% |

| Frasers Property | TQ5 | 0.33 | 9.4 | -6% | -53% |

1) City Development (SGX: C09)

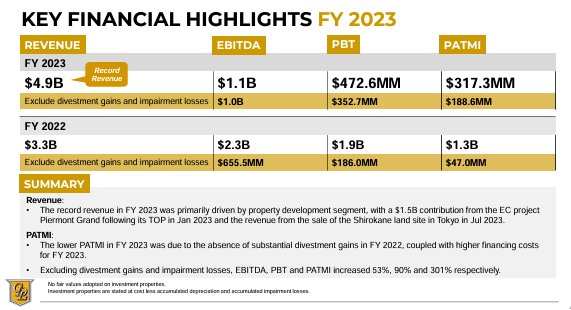

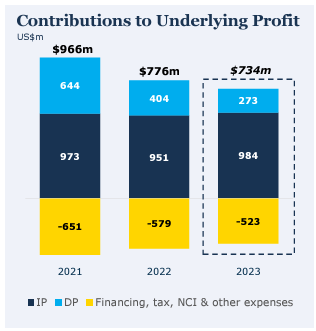

City Developments Limited (CDL) achieved record revenue of $4.9 billion in FY23 as compared to $3.3 billion a year earlier, primarily driven by the stellar performance of its property development segment in Singapore.

The investment properties and hotel operations segments also saw a 31.8% and 8.5% increase in revenue respectively for FY23. The investment properties segment grew mainly due to several new acquisitions, including St Katharine Docks in the UK and various living sector assets in our key overseas target markets.

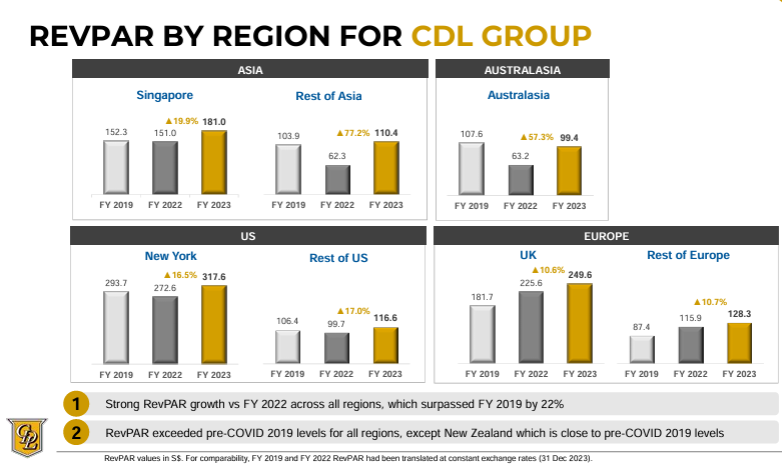

The hotel operations segment continued to increase steadily, with Revenue Per Available Room (RevPAR) growth across all regions. Key markets of Singapore and the UK reported RevPAR growth of 19.9% and 10.6% respectively, while the rest of Asia outperformed with a 77.2% improvement in RevPAR, driven by China and Taiwan hotels. Asia, Europe and the US regions exceeded 2019’s pre-pandemic RevPAR levels.

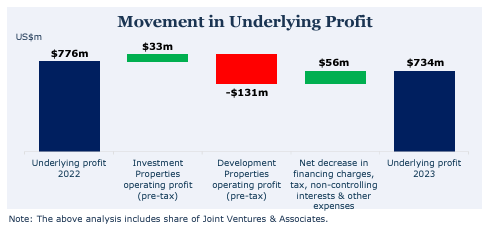

Net finance costs doubled and eroded the profits of CDL, as the average interest rate increased to 4.3% per annum for FY23 as compared to 2.4% in FY22.

Despite the higher finance cost, due to the better business performance, CDL’s PATMI (excluding divestments/impairments) stood at $188.6 million, a 301% increase from FY22.

As CDL recorded net divestment/impairment gains, revalued net asset value (RNAV) increased from $19.14 to $19.46 per share, even after dividends.

Just recently, CDL repurchased 954,000 ordinary shares at an average price of S$5.75. This represents a discount of 70% to RNAV per share of S$19.46 (Note that CDL carries its investment property and hotels under management at cost and therefore the RNAV yardstick will make CDL comparable to its peers), and represents approximately 0.11% of CDL’s issued shares (prior to the share buyback).

After deploying S$2.4b in acquisitions & investments in FY23, CDL is also planning to switch to asset recycling mode, targeting S$1b of divestments in FY24, partly to further optimize its portfolio and keep gearing at comfortable levels.

2) HongKong Land (SGX: H78)

HongKong Land (HKL) saw declines in revenue of about -18% to $2.24 billion and underlying profit of -5% to $0.73 billion in FY23. A slight improvement from the Investment Properties segment could not adequately offset lower development profits on the Chinese mainland which are inherently lumpy in nature and also due to the current weak Chinese market sentiment.

The improved performance in the investment properties arose from its luxury retail and Singapore office portfolios, offsetting continued reduced contribution from the Hong Kong office portfolio.

Total contributions from Development Properties were impacted by challenging market conditions on the Chinese mainland, which led to lower sales and reduced profit margins. In addition, the decision was taken to impair a small number of residential projects, although this was broadly offset by net gains from the acquisition of two equity stakes in existing joint-venture projects for considerations below development cost.

HKL recorded its fifth year of revaluation losses to its investment properties amounting to around $7.5 billion, pulling the value of its prime investment properties down to $26.7 billion from nearly $34 billion at the highs.

Consequently, the NAV per share at FY23 fell to $14.49, compared with $14.95 at FY22 and $16.43 in FY18.

HKL expects market conditions in the core markets of Hong Kong and the Chinese mainland to remain challenging in FY24. The management reports that “while the resilience of our Investment Properties business provides continues to provide HKL with a solid base of recurring earnings, trading performance of the Hong Kong Central portfolio is expected to be lower, due to negative office rental reversions.”

An improvement in Development Properties earnings is anticipated, however, based on planned project completions on the Chinese mainland and in South Asia.

As HKL’s investment portfolio is substantial and the main income driver, efforts in its property development segment will struggle to offset any weakness in its investment portfolio.

3) Frasers Property (SGX: TQ5)

Fraser Property (FPL) recently announced key organizational changes aimed at simplifying the structure and to align with the company strategy.

FPL had a mere $12 billion in AUM in 2013 and have nearly tripled it within 10 years.

The company is now moving from the previous growth and consolidation stages into a resilience phase where it intends to deepen its capability in each asset class and continue to invest into sectoral structural trends.

FPL has about 80% of its FY23 revenue and profits arising from the developed markets shaping the risk profile of FPL as such.

The remaining 20% in emerging markets is mainly attributable to Thailand, a country in which its major shareholders have extremely deep expertise. FPL’s major shareholders also happen to be the largest property developer and landlord in Thailand, control vast businesses such as Thai Beverage and own controlling stakes in retail businesses such as the Thai hypermarket operator Big C. This substantially changes the risk profile as Thailand is their home ground and they are not a foreign investor.

Similar to other property conglomerates, the sub segments FPL has invested into is in line with secular trends.

In FY23, FPL recorded a 1.8% increase to revenue and 5.1% increase in profit before interest and tax (PBIT). However, its attributable profit fell substantially due to its first revaluation loss after at least 5 consecutive years of gains. As its underlying PBIT improved, FPL increased its dividend payout by 50% to 4.5 cents per share.

FPL actually recorded a total of $3 billion in fair value gain, however, its NAV stood at $2.46 in 2017 and is now at $2.52 after falling $0.12 from FY22, in part due to a $0.03 dividend and mainly contributed by foreign currency translation losses over the years.

The Singapore Dollar (SGD) has seen continued strength against foreign currencies such as the Australian Dollar, Euro Dollar, Chinese Yuan, Thai Baht and Vietnamese Dong. FPL prepares its financial statements in SGD and therefore records translation losses when these overseas assets are translated on its financials into the SGD.

Naturally, FPL has cash flow hedges in place for the portion of income that is required to be remitted, but otherwise, just like its peers, it would not hedge income that are meant for local use and would naturally see the value diminish when converted to SGD.

FPL is multi faceted in that it is not only in residential development but it also has a very substantial pipeline of development in industrial and logistics in countries such as Vietnam, Australia and Germany.

It also has a REIT platform in place with three REITS of which two, Frasers Centrepoint Trust (SGX:J69U) and Frasers Logistics & Commercial Trust (SGX:BUOU) are part of the core Straits Times Index.

Best Singapore Property Developer Stock to buy now?

Our best buy today is City Development (CDL). This is because we think that CDL would be the fastest to return a positive share price return to investors. Most segments ranging from property development to hotel and living sector assets are actually performing well. CDL itself is a victim of global trends affecting its office portfolio and financing costs. CDL is also just beginning a share buyback program which would likely lead to positive returns in the immediate term.

Hongkong Land (HKL) is either for the contrarian investor or someone with great political foresight, given that the company has undergone 5 years of revaluation losses, mainly arising from its Hong Kong investment portfolio. It is not to say that HKL is poorly managed. In fact, HKL has a substantial valuable land bank across Asia and is continuously building on its property development segment. It also has a low net gearing of 17%, putting it as one of the developers with the strongest balance sheet amongst its peers.

Frasers Property (FPL) was in the news recently for refuting speculations that the company’s majority owners could sell the company or some of its assets, as part of a strategic review which was speculated to be in its initial stages, and was part of shareholders’ efforts to raise capital, in order to reduce the debt accumulated across the past few years from acquisitions. At this point, any possible capital transaction is unknown and is uncertain whether it will become an upside for investors.