I’ve been getting a lot of questions about Mapletree Logistics Trust of late.

This is a $7 billion market cap logistics REIT sponsored by Mapletree.

So safe to say it is very popular among retail investors, as the Mapletree name gives it perceived “stability”.

Yet from its 2021 highs, Mapletree Logistics Trust has dropped 33%.

At current price of 1.41 – it’s back at the lows last hit in March 2020, which is pretty unbelievable stuff.

Annualised dividend yield is 6.4%.

Is this REIT a screaming buy?

Or a value trap?

Dividend Yield of Mapletree Logistics Trust

Unlike many other REITs which are reporting negative DPU down 10 – 15%.

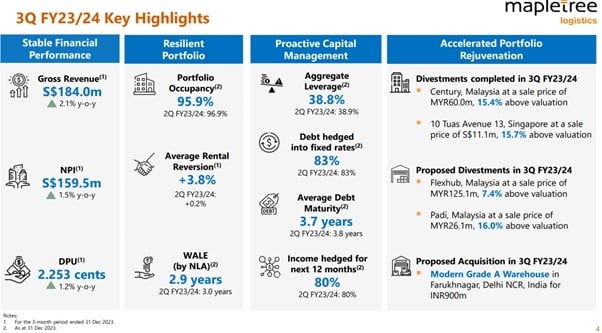

Mapletree Logistics Trust is actually reporting a 1.2% year on year increase in DPU.

This is actually very good (in this climate of higher interest rates).

Annualising the latest DPU gives you a 6.35% dividend yield for this REIT.

Price / Book of Mapletree Logistics Trust

NAV is $1.40.

So at current price of $1.41 you’re basically buying in at book value.

What are you buying at this price for this REIT?

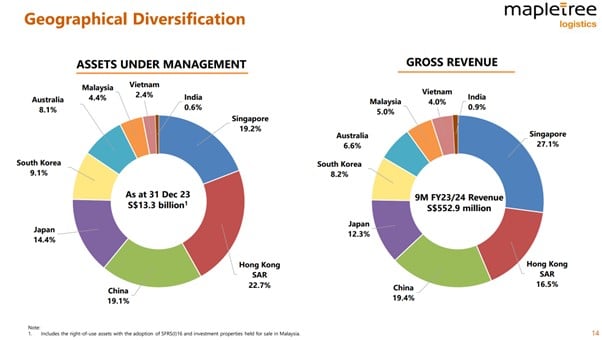

$13.3 billion worth of logistics real estate located across Asia.

The top 5 markets ranked by size:

- Hong Kong (22.7%)

- Singapore (19.2%)

- China (19.1%)

- Japan (14.4%)

- South Korea (9.1%)

Cumulatively these 5 countries make up 84.5% of the REITs property portfolio:

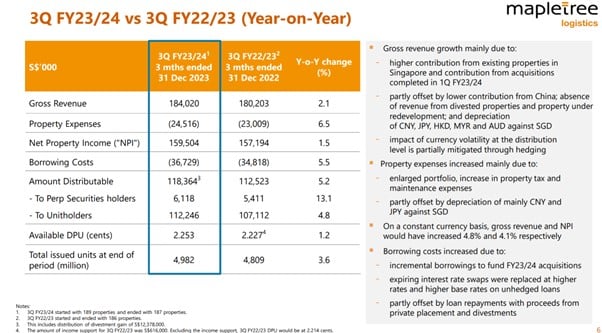

For what it’s worth, the financial results are good too.

Gross revenue is up 2.1% year on year.

Rental reversion up 3.8%.

38.8% leverage, with 80% of income for next 12 months hedged.

What’s to explain the big decline in share price for this REIT?

What I don’t like about Mapletree Logistics Trust

Let’s jump straight into the good stuff.

What I don’t like about this Mapletree Logistics REIT.

3 big points:

- A lot of China Exposure

- A lot of overseas real estate – not easy to evaluate the quality of the property portfolio

- A lot of debt

Problem 1 – A lot of China exposure

Relook the chart above.

And you’ll find that almost 42% of the REIT is China exposure – Hong Kong and China.

International Investors are not a big fan of China these days

In case you’ve been hiding under a rock for the past year, foreign investors cannot drop China exposure fast enough these days.

Whether due to poor performance, or due to US ties (fear of sanctions), or investments mandates that prevent them from investing in China – not many investors want to touch CHina.

Mapletree Pan Asia Commercial Trust has 50% of its asset base in best-in-class Singapore real estate (Vivocity and Mapletree Business City).

And yet the 30%+ exposure to Hong Kong / China has wrecked its performance and share price.

The fact that Mapletree Logistics Trust has 42% exposure to Hong Kong / China and yet been left alone by the market for this long has been pretty surprising to me.

My views on China?

I’ve shared my views on China in the past, which fundamentally remains the same.

China is going through a period of structural deleveraging, to transition the economy away from real estate into advanced manufacturing and domestic consumption.

This is not something that takes place in months, it will take years.

Short of massive stimulus from Beijing, I would expect China’s economy to stay slow for a while as they navigate this transition.

This could translate into a lot of pain for China real estate near term.

We won’t see a big meltdown like Lehman of course as this is China.

But it might be a painful grind down similar to Japan in the 1990s (although I recognise Japan’s real estate bubble was more extreme).

Now to be clear – I’m not saying China real estate is uninvestible, just saying that you need to price this in properly.

And my concern with Mapletree Logistics Trust for much of this cycle was that the market was not properly pricing in the China exposure.

Problem 2 – A lot of overseas real estate – not easy to evaluate the quality of the property portfolio

Let’s take a closer look at the property portfolio.

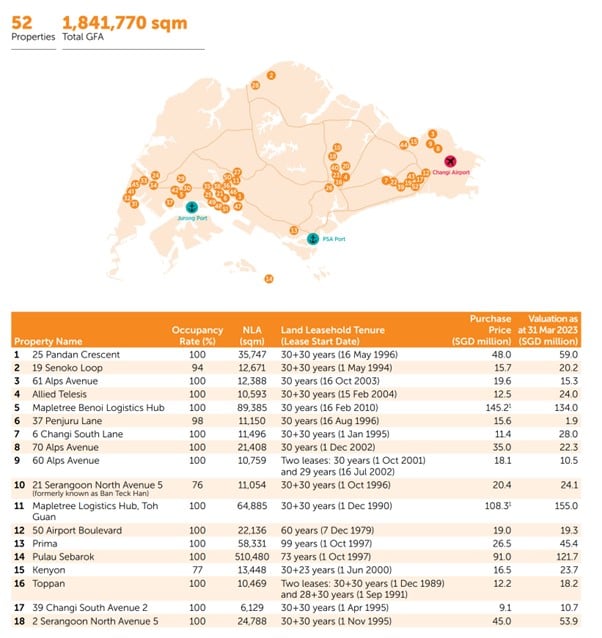

Singapore Portfolio of Mapletree Logistics Trust

The Singapore portfolio, is what you would expect of an industrial REIT.

If this REIT were 100% Singapore properties, trading at these valuations – I would buy it in a heartbeat.

But unfortunately Singapore is only 19.2% of the portfolio – we have to look at the other countries as well.

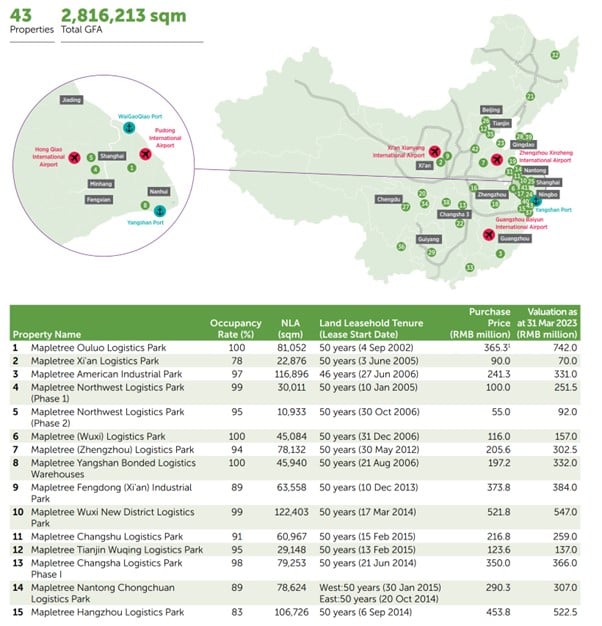

China Portfolio of Mapletree Logistics Trust

How to evaluate logistics properties?

There are 3 big things you look for when evaluating logistics properties:

- Location – is it near population centres, transportation hubs etc

- Facilities – how advanced are the equipment, building specifications etc

- Competition – is there a lot of competition in the region

Now if this were the Singapore portfolio I could answer some of these questions.

But throw me the REIT’s China or Hong Kong portfolio, and I simply have no clue.

I have not visited any of these properties in my life, it is incredibly hard for me to comment on the quality of Mapletree Logistics Trust’s overseas portfolio.

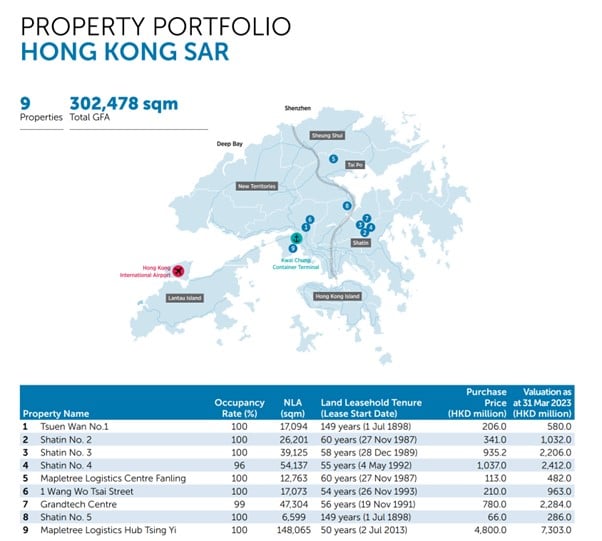

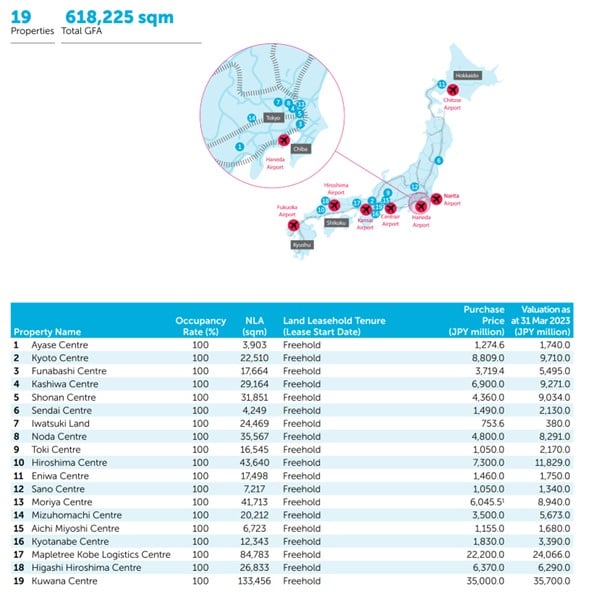

Hong Kong/Japan Portfolio of Mapletree Logistics Trust

I’ve also extracted the maps of the Hong Kong and Japan portfolios below.

Fundamentally, we have the same problem with China in that it is very tough as a Singapore investor to assess the quality of the real estate held by the REIT.

What can a REIT investor do – Buy or avoid Mapletree Logistics Trust?

Which means that as an investor you have 2 choices:

- Trust the numbers you’re seeing in the financial results, trust the manager, and be comfortable with a cursory desktop diligence of the assets

- Skip the REIT

To be clear – I am not saying that Mapletree Logistics Trust’s property portfolio is bad.

I am just saying that it is incredibly tough for me, as a retail investor sitting in Singapore who has never visited any of these foreign assets, to make a judgment on this.

If you’re just happy with the former, then for what it’s worth a tabletop analysis looks decent, as the operational metrics look good.

But call me old fashioned.

I’ve found that real estate is a local business – and I don’t like investing in real estate I’m not familiar with.

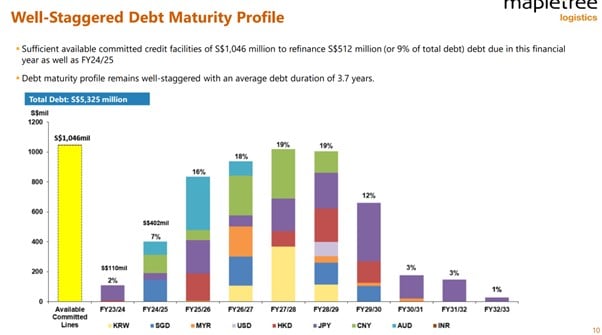

Problem 3 – Mapletree Logistics Trust holds a lot of debt

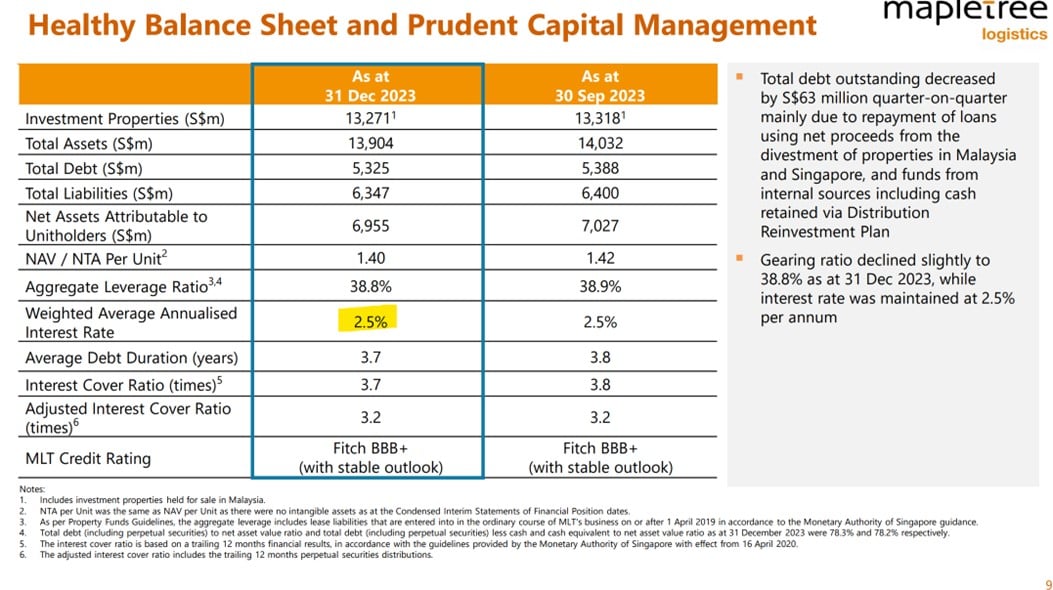

This REIT has $580 milllion in perpetuals.

$5.3 billion in debt.

Add that up and it’s $5.9 billion effective debt.

Working out to an effective gearing ratio of 44.6% (including perpetuals).

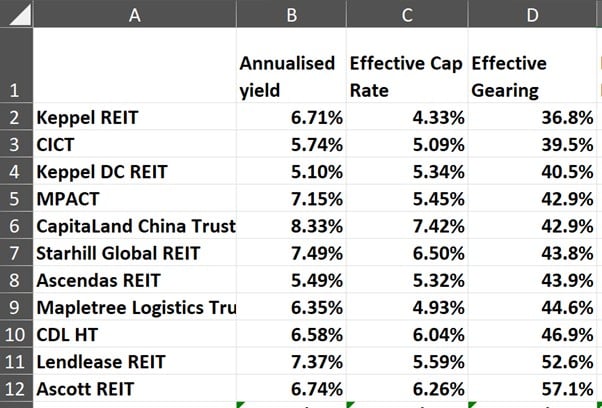

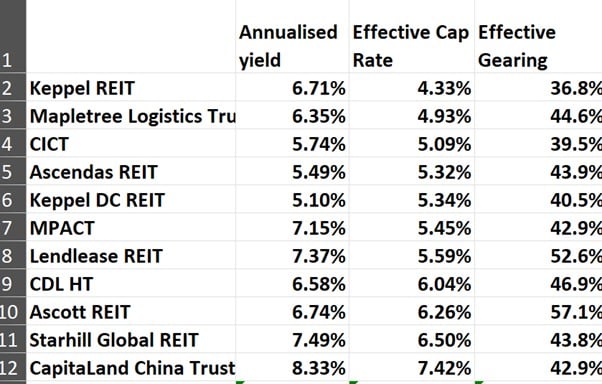

I tabulated the effective gearing (including perpetuals) of a bunch of REITs on my watchlist below (see full REIT watchlist on FH Premium).

Mapletree Logistics Trust at 44.6% is on the higher end of this range – though not fully in the 50%+ danger zone like Lendlease REIT.

Yet the REIT continues to spend a lot of money

Despite the high effective gearing though.

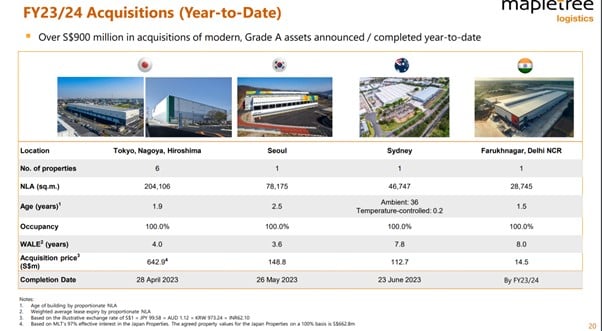

Mapletree Logistics Trust has still been generous with its acquisition.

Year to date for FY23/24, they have made $900 million in acquisitions.

While only making $207 million in divestments.

That’s a net 700m outflow of cash, in an era where cash is expensive.

These days, cash is expensive for REITs

Not sure if they got the memo, but the narrative for REITs has shifted.

These days, REIT investors don’t want to see acquisitions anymore.

They want to see divestments, paying down debt.

Money is expensive in this new paradigm, and the market will punish you if you take on too much debt to try and grow too fast.

The fact that Mapletree Logistics Trust runs quite high debt levels is itself concerning.

The fact that they continue to gear up for new acquisitions… I don’t know what to say.

The entire REIT space is just praying for interest rate cuts at this point – what if they don’t come (or come less than expected)?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

Current cost of debt is 2.5% – that’s only going to go up for the REIT

What caught my eye though – is that their current annualised interest rate is a mind boggling 2.5%.

In a climate where most other REITs have an average cost of debt of 3.5%.

Why is Mapletree Logistics Trust borrowing so cheaply?

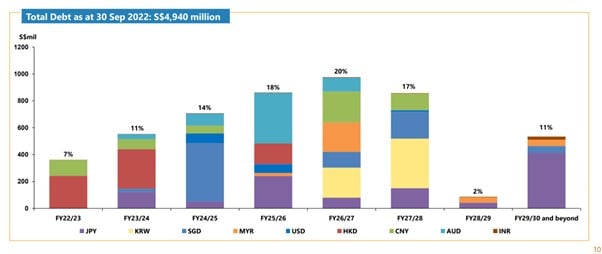

So I went back into 2022 and dug up their debt maturity profile back then.

It turns out their secret is that very little of their debt matured from 2022 – 2023, so they’re kind of still “locked-in” to low interest rates from pre-2022.

They also hold a lot of JPY denominated debt which is very cheap (JPY interest rate is 0.1%).

That said – the REIT will not be immune forever.

In the next few years there is a lot of debt to be refinanced, so the REIT will feel the pain of higher interest rates at some point.

Valuations of Mapletree Logistics Trust – are they attractive?

At the end of the day though, it all comes back to pricing.

There’s no such thing as bad real estate, only a bad price.

So let’s discuss pricing.

The problem with using book values for REITs these days is that most of the property valuations were done in an era of zero interest rates, which don’t make so much sense today.

I find that effective cap rate gives me a better apples to apples comparison when valuing REITs.

This works by taking the net property income and dividing by the value of the property (market cap + outstanding debt + any perpetuals).

If effective cap rate is 5%, that means for every $100 you pay, you get $5 in net rental income back each year after deducting expenses.

Running the numbers for Mapletree Logistics Trust – give us an effective cap rate of 4.93%.

Compared vs other REITs on my watchlist below (see full REIT watchlist on FH Premium), you can see how Mapletree Logistics Trust (by this metric) remains quite pricey.

I know there is 19% exposure to Singapore and 14% exposure to Japan which deserves a more premium valuation.

But at the same time the 42% exposure to China/HK deserves a valuation discount in my view.

Will I buy Mapletree Logistics Trust?

Full disclosure that I hold a very small position in Mapletree Logistics Trust.

I bought this position in the 2010s in the low $1 range.

I have not added to the position since.

Does that change today?

I’ve always said that while I like REITs at this point in the interest rate cycle.

I am sticking to REITs with primarily Singapore real estate.

Mapletree Logistics Trust has big exposure to Singapore, China, Hong Kong, Japan.

I expect the Singapore properties to do well.

While Japan could do well as interest rates stay close to 0%.

China, Hong Kong, is a big question mark though.

Best cast it stays flat, worst case who knows.

But with this REIT you can’t pick and choose, you have to buy it all or nothing.

So… would I buy Mapletree Logistics Trust at a 4.93% effective cap rate?

Personally I think the price is on the high side, given the amount of China/Hong Kong exposure the REIT is running today.

Not to mention that effective debt levels are very high, which limits optionality for the REIT going forward.

I could be tempted to buy if I were more familiar with the real estate portfolio.

But most of the overseas portfolio I just cannot comment on how strong they are, which makes it hard for me to decide whether to be a buyer or not.

And given how many opportunities there are in the investing space right now, I can afford to be choosy.

But hey – that’s just me.

For investors who like Mapletree Logistics Trust though, prices are back to 2020 lows, and back at 2022 lows.

If this support levels hold, it could be an interesting entry point.

For me personally, I am buying REITs at this point in the interest rate cycle, but I don’t think Mapletree Logistics Trust is going to be one of them.

You can see the full list of REITs I am buying on FH Premium (just updated the full REIT watchlist last weekend with the REITs I am buying, and price targets).

This article was written on 21 March 2024 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

WeBull Account – Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.