In my last note about whether I should shift my fixed income allocation away from the Global Aggregate bond index fund, I got into two separate discussions regarding what I said about asset-liability matching with a bond fund.

I said that:

Make sure that the average duration of your fixed income ETF/unit trust is less than the time you need the money (your break-even point).

A Telegram group member tries to point out that a typical bond fund would reinvest a matured bond into another bond. The bond tenor and duration would more or less be maintained.

Suppose we invest in a global aggregate bond fund with an average duration of 6.5 years and an average tenor of 8 years. If I have a time horizon of 12 years to my goal, I should be able to invest in the global aggregate bond fund, as explained in the statement above.

The member’s point is that as one bond matures and reinvested into a bond with tenor close to the fund average, the fund would be subjected to the same interest rate risks again. That would mean that you don’t get close to the yield to maturity, which is the measurement of the value of the bond at the start.

Subsequently, a Johnny commented in the blog post:

For bond funds, my understanding is that you have to be able to hold for 2x the duration of the fund in the event of a rising interest rate environment, not just 1x the duration of the fund.

He also pointed me to the research paper that states this: For Constant-Duration or Constant-Maturity Bond Portfolios, Initial Yield Forecasts Return Best near Twice Duration.

The paper concludes that

- This relationship works on longer-term bond investment.

- The yield of a constant-duration bond portfolio equals the arithmetic mean return over a time horizon equivalent to twice the bond portfolio duration minus one-month.

- There were errors and they were explain by the convexity of the yield path:

- Convex: negative forecast errors.

- Concave: positive forecast errors.

- This research seem to make investment-grade bonds appear less risky to long term investors.

I got to thank both for challenging what I wrote.

To be honest, it did slip my mind hat for a bond fund, you might not get exactly the initial yield to maturity.

In my article, I did my best to explain that what we are more concern with is the worst case scenario, where the investor at least break-even on their investment if they abide to the bond fund average duration.

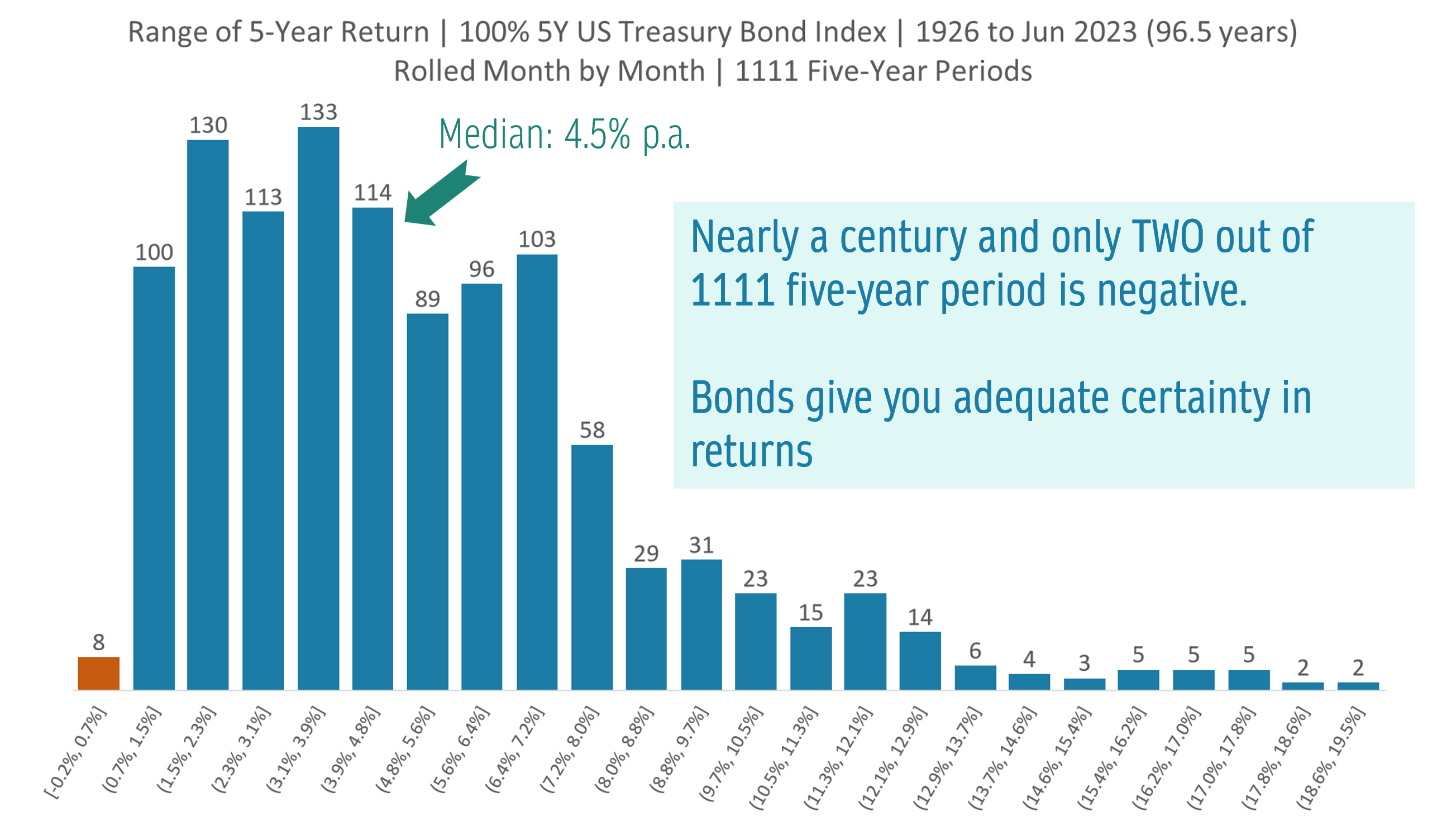

In my YouTube video about Crafting an ideal passive investment portfolio, I shared this slide regarding the range of historical returns if you invested in a five-year US Treasury note for a period of five years:

I shared this chart to show that if you have a shorter need towards some of your financial goals, having more bonds would make more sense because of the greater certainty in the event that market conditions are not in your favor. Having the bond allocation will also make your portfolio easier to stomach during the bear market periods.

In 1,111 unique five-year periods, only 2 end up slightly negative.

The role of the bonds is not to spearhead the return of your portfolio. We hope that there are some returns not to drag down the overall return of the portfolios. But the main role is to be low volatile when we most need it.

That said, I didn’t say if you reach that time horizon, you will earn that yield to maturity.

I think both got triggered by the idea that a constant-duration bond fund can be use for asset-liability matching. I think that might not be the best implementation. The iBonds that I talked about earlier with its fixed maturity would be a better implementation.

I reflected upon the whitepaper Johnny pointed me to.

That paper is applicable if hitting the initial yield to maturity is important to you but it also says that the 2 times duration is more valid if your time horizon is long.

If most of us have a long time horizon, would we want to be in equities? I think there are some investors who are more risk adverse who would prefer a close to 100% fixed income portfolio. But I would like to think if our time horizon to hold our bond allocation is like 20-30 years, we won’t know what yield to maturity we will get eventually because we will go through a few rounds of maturity.

My Telegram group member gave an example of a 3-7 year bond ETF. The average duration of the bond ETF is about 4.3-4.5 years. Had we invest slightly longer than that duration, our returns would still be negative. He did admit that he cherry picked a pretty dismal period.

I got curious about what he said so I tried my best to simulate.

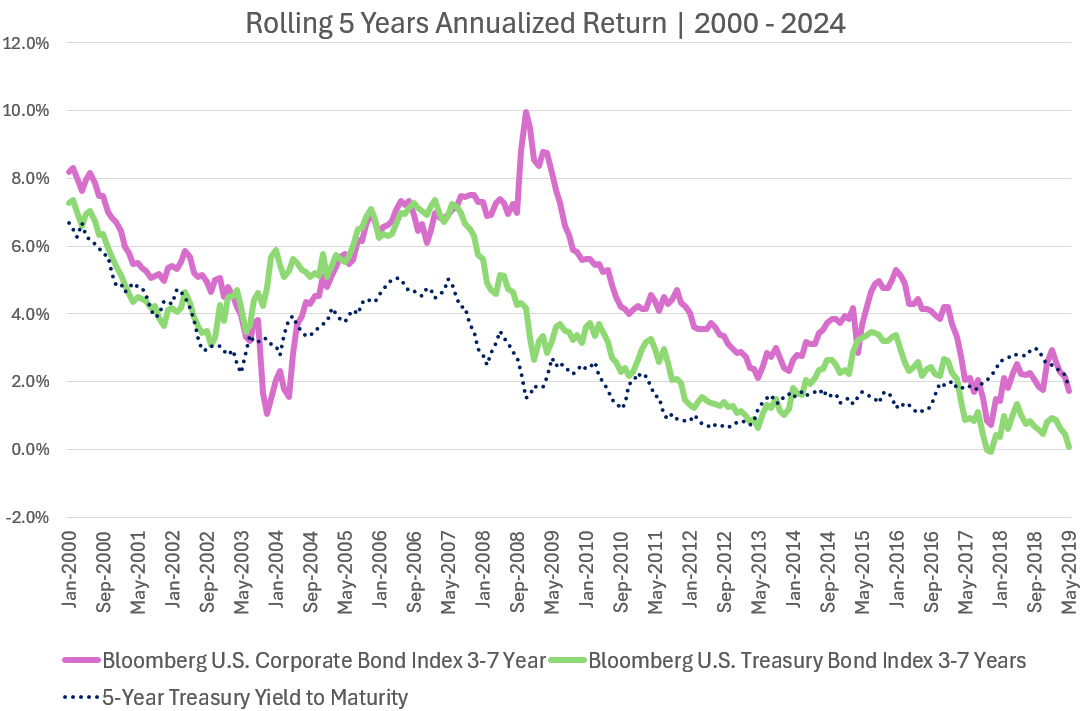

I wanted to use the iShares 3-7 Year Treasury Bond ETF but I had problem getting the NAV. So I decide to tap upon the data bank that I have and managed to find:

- Bloomberg US Corporate Bond Index 3-7 year

- Bloomberg US Treasury Bond Index 3-7 year

With these two index, I am able to plot the rolling 5-year return against the yield to maturity of the 5-Year Treasury Yield to Maturity taken from FRED.

What I want to see: If the yield to maturity of the 5-year Treasury Yield is X, then five years later, the annualized return of the bond index should be close to there.

The chart below plots the rolling 5-year annualized return of both 3-7 year index against the yield to maturity (blue dotted line):

Each purple and green dot shows the return from Jan 2000 to Dec 2004, then Feb 2000 to Jan 2005 and so on, so forth. So the return should coincide with the yield to maturity of the Five Year US Treasury note.

What we see is that the corporate bond index (purple) tend to outperform the treasury bond index (green). This is not surprising, given that the corporate bond index is more risky, and there is a credit premium attached to the typical bond pricing. But there are investment periods where the Treasury bond index outperform the corporate bond index (those five year periods starting in 2004).

What we notice is that the returns are usually higher than the 5-Year Treasury Yield to Maturity (blue dotted line) but not always. Those five year periods starting in 2018 saw the returns lower than the yield to maturity of 2% of the 5-Year Treasury Yield.

The 3-7 Years Treasury Bond Index has a shape that tracks the 5-Year Treasury Yield better.

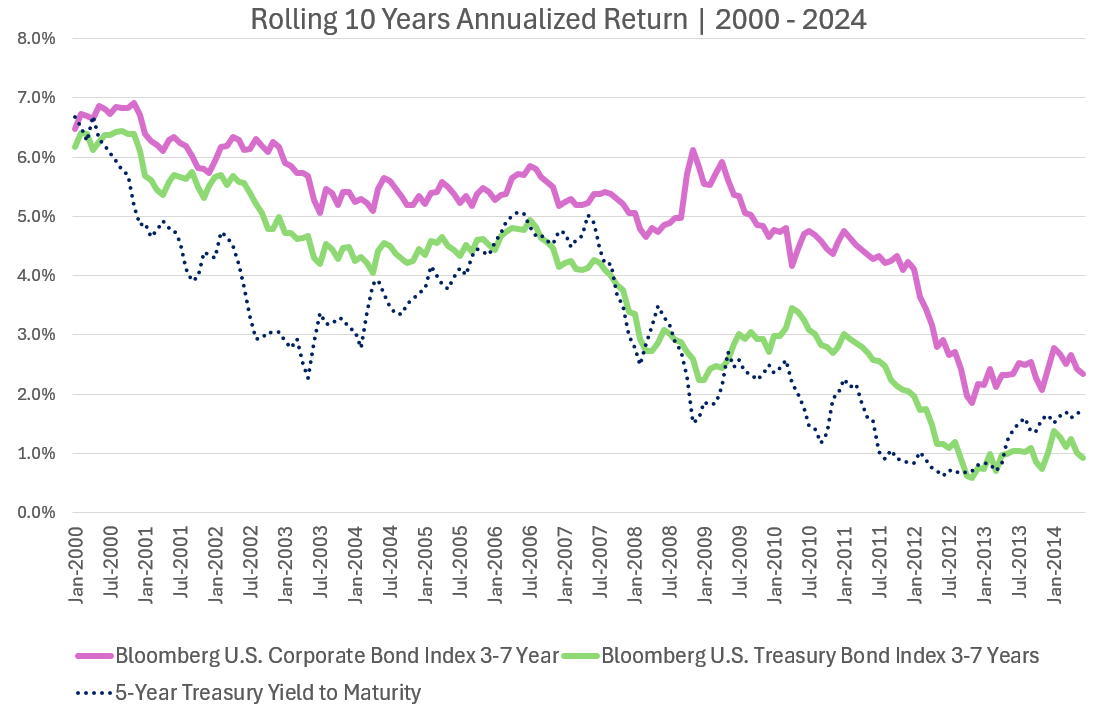

So if we double the tenor to be twice the duration or about 10 year, would the return be higher than the 5-Year Treasury Yield to Maturity like what the research says?

The chart below plots the rolling 10-year annualized return of both 3-7 year index against the yield to maturity (blue dotted line):

We can see that as we do what the research says, very often both 3-7 year Bond Index is higher than the yield to maturity. But there are some periods where the annualized return is slightly lower than the yield.

Looking at this chart I think:

- The constant-duration bond index fund future return kinda tracks the staring yield to maturity.

- But don’t expect the returns to be EXACTLY similar to the yield to maturity.

- In volatile periods such as the Great Depression in bonds and GFC, that is where we see some deviation with how the returns go.

- Risk that the bonds will underperform exist. I guess that is why there are returns.

If you wish to do asset-liability matching, especially if you have a well define date to your goal, using an iBond or some direct bonds may give you definite return but they have their downsides.

If your time horizon is 12 years, and you invest in a bond with a 8 year tenor, you have a reinvestment risk and your returns would be different isn’t it?

Hope this is useful for some of you.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Using Current Rental Income for F.I. Income Planning May be Flawed. (With 15 Years of Singapore HDB Rental Income Data.) - May 27, 2024

- PLH HDB Flats – Restrictive but May be Ideal Retirement Living for F.I.R.E People. - May 25, 2024

- Reflecting about A Stupid Income Strategy I Came Up With - May 23, 2024