I know I talk about wanting to write about Dutech part 2 in my previous post. However, CIMB released the initiation report and I thought there is no point writing about it since a lot of information can be derived from it. However, it has come to my attention that they have recently ceased coverage.

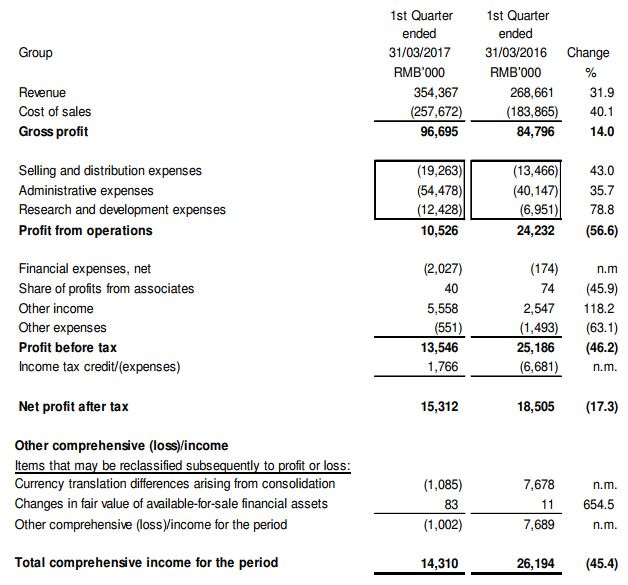

Q1 2017 Results

Net profit was down due to steel price increasing for high security segment, higher administrative and selling expense incurred by Metrics and increase in R&D expense. But I would think this is a decent set of result as increase in R&D expense is setting the sight on future revenue growth and improving on future competitive position. In the latest annual report, 22 new patents were awarded to Dutech. I look forward to more new patents in the coming years.

| Metrics | RMB – Mil |

| Revenue | 77.20 |

| COGS – Estimated to be at 70% to have a GPM of 30% | (54.04) |

| Selling and Distribution Expense | (5.30) |

| Administrative Expense | (17.30) |

| Research Expense | (1.40) |

| Loss before Tax | (0.84) |

Based on the disclosure in Q1 2017, I did a rough computation on the drag on bottomline by Metrics. I used a GPM estimate of 30% as the GPM for business solution improved from 25% to 28% due to change in product mix. As Metrics revenue is approximately half of the business solution segment, 30% should be a good estimate. Even without taking into consideration finance cost, other expense and taxes, you can see that Metrics is loss making and dragging the bottomline. That is the reason why Dutech is able to acquire companies cheap. The strategy of Dutech is outlined clearly on Droege Group website. Droege is a substantial shareholder of Dutech with 8% share. They were the company who sold Format to Dutech.

This is a table which I compute myself based on annual report disclosure. It further confirms the acquisition drag down the bottom line a lot. You can compare the margin against the acquisition timing for an idea.

What’s next?

The question to ask is really what does Dutech intends to do with all these acquisitons. A lot has been said about the death of cash but I do not agree with it. People behaviour do not change overnight and cash still has a place in society. However, the usage of cash might be reduced and hence this will impact on ATM replacement cycle. The replacement cycle might be extend to 4 or 5 years instead of 2 to 3 years due to lower usage. This will affect Dutech business. They are seeking to grow a new segment of revenue through business solution. The focus is on transport ticketing specifically. If you look at this link, there are 25 suppliers of transport ticketing and Dutech acquired 2 of them. Metrics and Krauth. These 2 acquisition immediately propel them to become the no 2 in the industry with 20% market share. The market leader is Scheidt & Bachmann GmbH. This is the same as high security segment where they are the no 2 and Gunnebo is the no1. A search reveal that the Smart Transportation Market is going to grow at a CAGR of 25% from the period of 2016 to 2021. This is definitely a high growth market.

I recently added to my position as I feel the valuation is still cheap. While the share price has gone down after i added, I am not too concerned as I feel most of the bad news has been factored in but positive has not. Hence I will be sitting on my butt for the next 2 to 3 years and watch the result. I am cutting short my post here as I am extremely lazy and would not have blog if not due to the request of one of my group chat mate. You know who you are. LOL. Thanks for reading.

Some inside info to share: A few PE funds made offers to Dutech management to privatize the company. However, they were turned off by the management asking price.

LikeLiked by 1 person

Thanks. That’s really nice to know

LikeLike