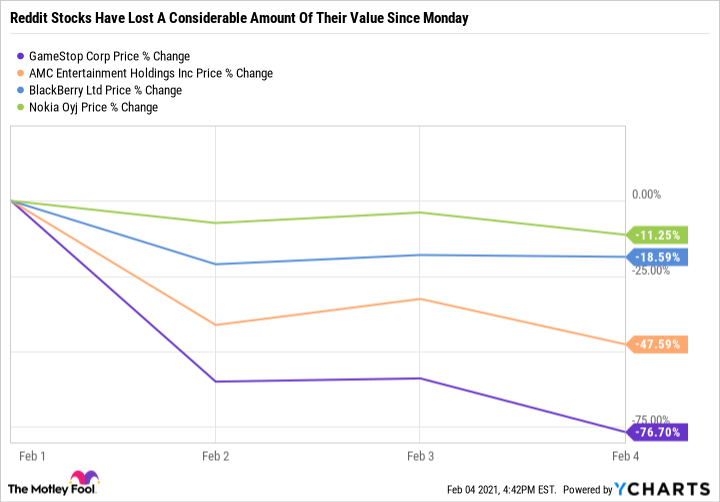

What looked like a glorious victory for the WallStreetBets subreddit all came crashing down this week as shares of GameStop, AMC, Blackberry, and Nokia all fell sharply. Shares of GameStop, in particular, are down over 75% in February.

Short squeezes are a volatile and often unpredictable game grounded in fear and frenzy rather than fundamentals. There are much better hidden gems with plenty of upside if you know where to look. We asked some of our contributors which underfollowed stocks they think are better buys now. They came up with Kirkland Lake Gold, (KL), Univar Solutions (UNVR), and TPI Composites (TPIC 8.74%).

Image source: Getty Images.

A golden opportunity flying under Reddit's radar

Scott Levine (Kirkland Lake): While GameStop and AMC are names on many investors' lips these days, Reddit's attention seems to have shifted from individual companies to a commodity: silver. In fact, the average price of the precious metal is nearly 8% higher than its average price of $25.90 in January. Gold, on the other hand, is not recognizing the same increase; the average price of the yellow metal in February has dipped about 1.3% from its average price last month. Consequently, Kirkland Lake, a leading gold mining company, looks like a sparkling option for investors at the moment.

In mid-January, the company announced that it met 2020 guidance and achieved gold production of 1.37 million ounces, representing a 41% increase over the 974,615 ounces it produced in 2019. Although investors will have to wait until Feb. 25, when the company reports Q4 2020 earnings, to gain greater insight into its financial performance -- in particular whether it met its 2020 all-in sustaining costs forecast per gold ounce of $790 to $810 -- it's worth noting that in the company's recent press release, management reported that the company ended 2020 with a strong balance sheet: $848 million in cash and no debt.

Another alluring quality of Kirkland Lake is the company's commitment to rewarding shareholders. In 2020, for example, the company raised its dividend twice to where it now stands, at $0.1875 per share, representing a 1.95% yield. Additionally, the company committed $732 million to repurchasing 19 million shares throughout 2020. And that's not all. Achieving the goal that it had announced in February 2020 of repurchasing 20 million shares over one to two years, Kirkland Lake repurchased 1.1 million shares in early January.

For investors interested in adding some sheen to their holdings, Kirkland Gold is on sale. Whereas the stock's five-year average operating cash flow multiple is 10.5, it's currently changing hands at 8.6 times cash flow. Further illustrating its discount status in terms of earnings, the stock is trading at a multiple of 13.5 -- a steep discount to its five-year average ratio of 27.

Univar is quietly restructuring for growth

Lee Samaha (Univar): The case for buying into the specialty chemicals distributor is based on a simple idea. It comes down to good old-fashioned blocking and tackling and focusing on what you do best.

Univar is refocusing its business toward concentrating on its core chemical distribution business and streamlining the company with an aim to expanding its margin in line with its peers.

Over the last few years, Univar has sold some of its noncore distribution businesses serving the plastics, environmental science, and industrial spillage industries in favor of concentrating on specialty chemicals distribution.

A key part of the plan is to generate cost synergies from its $1.8 billion acquisition of fellow chemical and ingredients distribution company Nexeo Solutions in 2019. Univar plans to generate $120 million in annual net cost synergies from the deal by the first quarter of its fiscal 2022. Meanwhile, management plans to structurally reduce costs and invest in digital capability in order to drive margin expansion.

Ultimately, Univar is aiming to increase its earnings before interest, taxation, depreciation, and amortization (EBITDA) margin from 7.6% in 2019 to 9% in 2022. It's a figure that implies an 18% increase in EBITDA at the same level of revenue.

Evidentially, Univar is on track, as its third-quarter 2020 adjusted EBITDA margin came in at 8.2%, compared to 7.7% in the same period of 2019, despite an 11.3% drop in organic sales. In addition, an analysis shows Germany's Brenntag is able to achieve a 9.9% EBITDA margin in North America, so why can't Univar improve its margin in line with its peer?

Based on analyst estimates for 2022, Univar will trade on an enterprise-value-to-EBITDA valuation of less than 7 times, a price-to-free-cash-flow multiple of less than 11 times, and a PE ratio of 12.5 times earnings. Those figures make the stock look like a great value, and investors should listen for the company's next earnings call on Feb. 25 in order to monitor progress on its plans.

A pure-play wind energy stock that no one is talking about

Daniel Foelber (TPI Composites): In the last year alone, TPI Composites quietly grew from an $800 million company to a market capitalization of over $2.5 billion. And for good reason. It's the largest independent composite wind blade manufacturer in the world and has been growing revenue at an impressive rate -- earning a record-high $474.1 million in the third quarter. The company is guiding for $445 million in fourth-quarter revenue, which would give it $1.65 billion for the year (roughly 15% above what it earned in 2019). At its current valuation, TPI would have a price-to-sales (P/S) ratio of just 1.5, which is more than reasonable for a growing pure-play wind energy stock.

After it invested heavily in new manufacturing and engineering facilities, TPI's profitability is improving, and it's paying down debt as well. The majority of TPI's business is through long-term service agreements with large original equipment manufacturers (OEMs) like General Electric, Vestas, Siemens Gamesa, Nordex, and others. Wind projects are capital intensive and incredibly complicated logistically, so these large OEMs often rely on independent blade manufacturers and other parts contractors. TPI has done an excellent job of partnering with a major OEM for every new manufacturing facility it builds. For example, the company opened a brand-new facility in Chennai, India, in 2020 (underscored by a long-term partnership with Vestas). In the third quarter, it signed a multiyear agreement with Nordex in India. It also added additional manufacturing lines in Mexico and signed new supply agreements with GE.

TPI's growth has helped it become the seventh-largest holding in the First Trust Global Wind Energy ETF (FAN -0.18%). At 3.77% it carries more influence than bigger companies like GE at 2.51% or NextEra Energy at 1.69%. Given how difficult it can be to find wind energy stocks, TPI Composites is a high-growth industry leader that's worth keeping on your radar.