The stock market has reached a stage where the entire flow is now dependent on the Russia-Ukraine conflict. Markets are extremely volatile with news causing an immediate knee jerk reaction.

Before the third round of talks between Russia & Ukraine commenced on Monday, 7 March 2022, Russia laid down two conditions, namely:

- Ukraine must amend its constitution to enshrine neutrality, i.e. pledge to stay out of NATO

- Ukraine must recognise Crimea as part of Russia, Donetsk and Lugansk as independent states

Needless to say, the talks did not lead to much progress aside from the plan to finally introduce the humanitarian corridor while the conflict continues.

With this, we have identified 10 US listed tech stocks that are trading below IPO prices and provide a few possible reasons why this is happening and whether they deserve to trade at these prices. We have not referred to their all time high prices as these prices would very likely have been overvalued due to the overly exuberant market conditions then.

1) SentinelOne Inc (NYSE: S) (-1% from IPO)

SentinelOne listed on 30 June 2021 at very lofty valuations and even now still trade at a mindboggling price to sales (P/S) of nearly 60x. This is nearly double its closest peer, Crowdstrike which is trading at a P/S of 30x. Other competitors such as Fortinet is trading at P/S of 14x and Palo Alto Network at a P/S of 11x.

Even with a 128% revenue growth on its latest quarter, it would still take years for the valuation to be priced in.

SentinelOne has nearly $1.7b in cash after its IPO raised $1.2b in cash and burned $90m in cash in the last quarter on a revenue of $90m. At this run rate, the company is able to sustain for a few more years.

With such lofty valuations, it clearly does not seem logical to enter this stock despite its strong revenue growth and cash position.

2) Fastly (NYSE: FSLY) (-7% from IPO)

Fastly is one fallen star with growth slowing to 13% QoQ and losing ground to competitors such as Cloudflare. It has provided a 13% revenue growth forecast for 2022, which implies a forward P/S multiple of about 4.5 times. However, it expects loss margins to widen slightly as it continues to pursue growth.

Unfortunately, Fastly’s balance sheet is looking weak with $933m in debt and a debt to equity ratio of nearly 1.0 times. On a positive note, it has $527m in cash and financial assets which would last the company a couple more years as its cash burn is relatively low.

While the P/S multiple may look reasonable, as the company is still recording operating losses and coupled with a low double digit percentage revenue growth forecast, It may seem worthwhile to wait a little while longer to identify signs of market share growth before considering an investment in Fastly.

3) Monday.Com Ltd (Nasdaq: MNDY) (-14% from IPO)

Similar to SentinelOne, Monday.com is trading at a lofty valuation of nearly 60x P/S. It is also facing competition from other project management tools. Despite tough competition, It just announced a strategic alliance with KPMG, one of the world’s biggest employer with more than 200,000 employees.

KPMG will not only use Monday.com’s platform to build solutions and apps for its member firms globally but also provide real time strategic insights and solutions to KPMG’s clients to enable these companies to digitally innovate their business and help them unlock opportunities for growth to stay ahead of industry challenges.

Unfortunately, its growth forecast might be inadequate for its current valuation with a 53% growth forecast and a negative operating margin of -30%. The company does have a strong balance sheet with nearly $900m in cash with no debt and and a very low cash burn rate as it remunerates its employees via share based compensation.

This is a case where the positives may not outweigh the negatives when the stock has such lofty valuations. Hence, it clearly does not seem logical to enter this stock with a relatively weak revenue growth rate.

4) DoorDash Inc (NYSE: DASH) (-22% from IPO)

Doordash has been on an acquisition spree, first acquiring European delivery company Wolt in a major all stock transaction announced in November 2021 and significantly expanding its geographical reach, adding parts of Europe to its current North America and Australia market. The deal is slated to close in the first half of this year.

Even before the deal closes, Doordash announced yet another acquisition, acquiring hospitality technology startup Bbot. The addition of Bbot’s products and technology to the DoorDash platform offers merchants more solutions for their in-store and online channels, including in-store digital ordering and payments. Together, Bbot and DoorDash will be able to better support the evolving needs of restaurateurs and other food and beverage venue operators.

DoorDash did well for its 4Q21/FY21 results, beating street expectations. Its full-year guidance suggests that it doesn’t see momentum slowing down, however. The company projected its marketplace gross order value to be in the range of $48 billion and $50 billion, which signifies a 20% growth. It also projects to nearly double its positive adjusted EBITDA.

On an as-is basis, Doordash is trading at a P/S of 5.6x with a market cap of $28b on a revenue of nearly $5b, has $4.8b in cash and nearly no debt. It also recorded positive operating cashflows.

It looks like Doordash could be one to look out for in 2022 and if it not only grows its existing business strongly but also executes its acquisitions well.

5) Affirm Holdings Inc (Nasdaq: AFRM) (-32% from IPO)

Affirm is one company that may need to work hard to regain investor’s confidence after it released a portion of its Q2 results early via Twitter by mistake. In addition, the stock crashed despite an upgraded revenue guidance for the rest of the financial year.

The upgraded guidance was due to Affirm’s tie up with Amazon which will allow Amazon’s customers to split the total costs of purchases into monthly payments using its service.

Affirm is guiding for its financial year ending June 2022 to record $1.3 billion in revenue, representing a P/S of 7.3x. With a 1H22 revenue of $630m, the guidance implies a 2H22 revenue growth of 6%. This actually looks low considering the Amazon tie up which is probably why share prices plunged.

With worries over slowing growth, while valuation has come down significantly, Affirm does look fairly priced and one may have to look for positive guidance from management before considering Affirm as an investment.

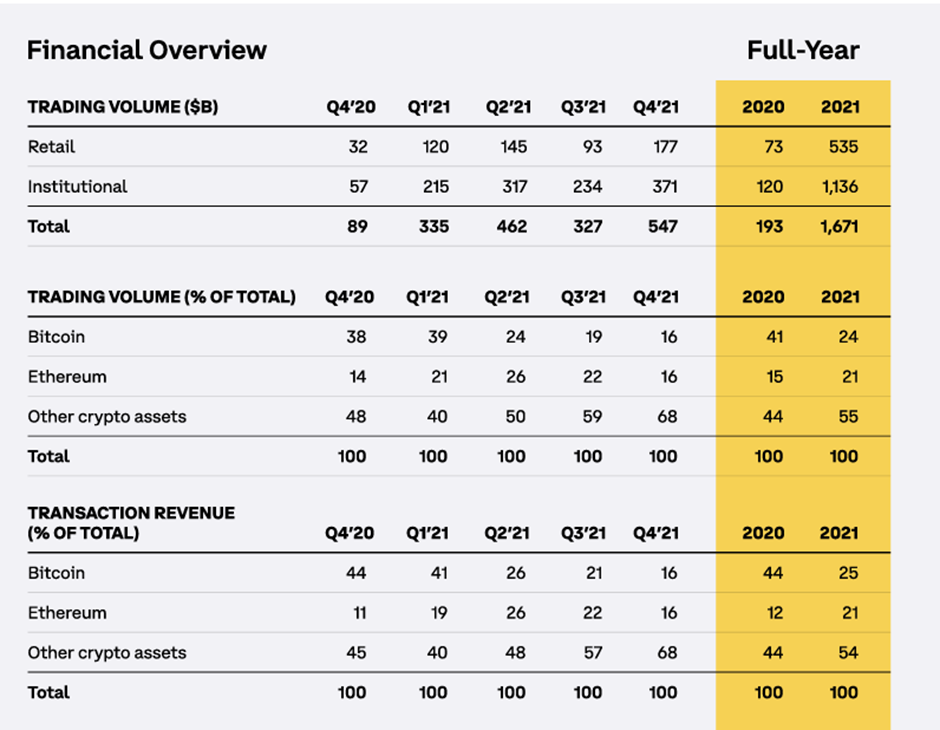

6) Coinbase Global Inc (Nasdaq: COIN) (-36% from IPO)

Coinbase was one of investor’s favourite as it is arguably one of the simplest way for newcomers to obtain an exposure to cryptocurrency. Coinbase has fallen much more significantly than the major cryptocurrencies despite a strong quarter with 4Q21’s revenue doubling from $2.5b from 3Q21’s revenue of $1.2b.

Coinbase not only increased trading volume but also managed to diversify its transaction revenue, with Bitcoin and Ethereum, the two core cryptocurrencies contributing to 32% of transaction revenue in 4Q21 vs 43% in 3Q21.

However, Coinbase provided a weak 1Q22 outlook expecting a decrease from 4Q21 due to lower crypto market capitalisation and volatility.

Essentially, Coinbase is the 10th biggest cryptocurrency exchange based on volume in the last 24 hours as of writing. Its future prospects are closely tied to the crypto market.

With a P/S of 5 times and P/E ratio of 11, this valuation is significantly lower than its closest comparables which are other listed stock exchanges. The valuation is also low if one takes a positive view of the growth of the cryptocurrency market, hence it does not seem logical that Coinbase is trading at this valuation and could be one stock to consider.

7) Roblox Corp (NYSE: RBLX) (-36% from IPO)

Roblox is a popular video game platform and is considered one of the hottest play on the emerging metaverse. It fell significantly following its disappointing fourth quarter results and outlook.

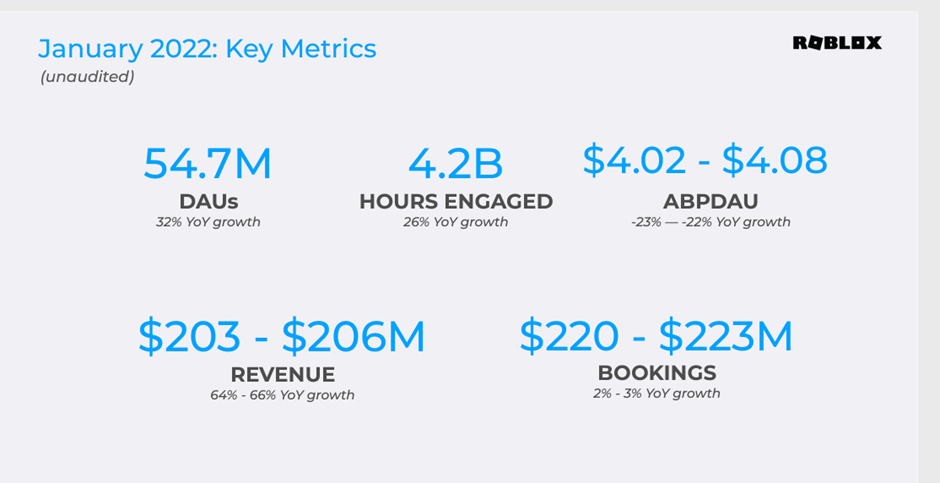

However, there is some hope for a turnaround as Roblox recorded strong January 2022 metrics with daily active users increased from 49.5 million as at Dec 21 to 54.7 million as of January. Revenue for the month was also expected to be around $203m which would represent 2022 revenue of $2.4b or a 26% YoY growth should Roblox be able to sustain bookings despite concerns over the endemic phase of the pandemic affecting user hours.

Roblox is trading at about a P/S of 12 times and is currently in an operating loss position. It has a strong balance sheet and a positive operating cashflow despite the loss position due to stock based compensation to employees and fees collected from bookings.

Hence while it may look fairly priced now, if it is able to deliver on growth expectations and reduce its loss position, Roblox may be a stock to look out for as it positions itself at the forefront of the Metaverse theme.

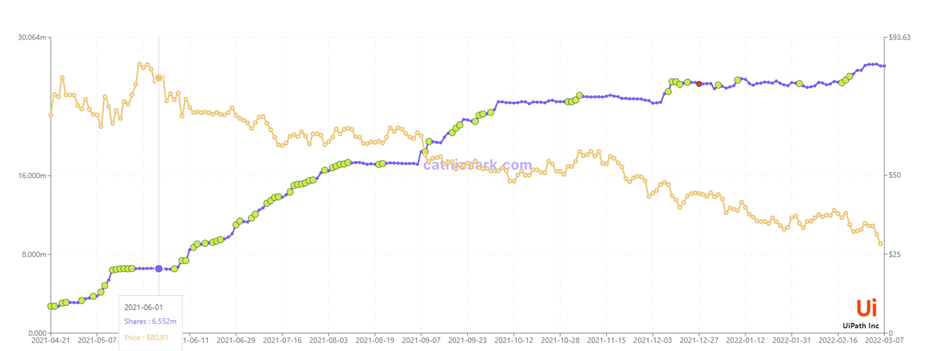

8) UiPath Inc (NYSE: Path) (-52% from IPO)

Similar to the other stocks mentioned here, UiPath has been on a downtrend. The stock has fallen each time the company reported financial results. The stock is currently trading at a P/S of 19x and makes an operating loss. Similarly, its operating cashflow deficit is buffeted by stock based compensation and payments receive in advance

One strong selling point for this stock is that it is a Cathie Wood favourite with the ARK ETFs holding about 27 million shares or a 5% stake in total. For investors who still believe in Cathie Wood’s keen focus on investing in innovation stocks and her declaration that “innovation is on sale”, it may seem illogical for the share price to be trading at such low prices considering that ARK has increased its stake significantly in this one.

9) StoneCo Ltd (Nasdaq: STNE) (-62% from IPO)

StoneCo is an investor favourite with investors such as Warren Buffett’s Berkshire Hathaway and investment firms such as T Rowe Price and Capital Research. At some point, Alibaba also held a position through Ant Financial. This is due to StoneCo’s position as a leading fintech solutions provider to small medium businesses, consistently strong revenue and active client base growth and also the confidence in its management.

The share price initially came down as the company faced credit losses from higher delinquencies due to difficulties in collections. The management admitted that its underwriting capabilities and collection process still had to evolve given the early stage of its credit solutions. The woes were further exacerbated by negative macroeconomic conditions surrounding Brazil as a result of its poor management of the COVID-19 pandemic.

StoneCo had acquired Linx, a retail management system software producer with a significant market share in Brazil and is in the process of integration. Linx would provide StoneCo with many new complementary business opportunities in adjacent sectors and vertical specific software solutions.

With revenue growing by 57.3% in the previous quarter (29.3% excluding Linx) to approximately US$300 million, this puts the P/S valuation at 2.3 which is its lowest valuation ever. This is one stock where it is clearly illogical for the share price to be trading at such levels.

10) Robinhood Markets Inc (Nasdaq: HOOD) (-70% from IPO)

Robinhood is the ultimate meme stock with many investors using the Robinhood brokerage app to invest in meme stocks.

Robinhood drew controversy when it locked investors out of trading in some of the hottest meme stocks such as GameStop and AMC. It also makes millions selling customers’ orders to high frequency trading firms which allows it to provide commission-free trades to retail investors.

For the first quarter of 2022, Robinhood anticipates that total net revenues will be less than $340 million, which implies a YoY revenue decline of 35% compared to 1Q21 and a QoQ decline of 6.5%. This indicates that the outsized revenue performance due to heightened trading activity, particularly relating to certain meme-stocks in 1Q21 is unlikely to be repeated.

Active users also declined from 18.9 million at September 2021 to 17.3 million at December 2021 although this was higher than the 11.7 million for December 2020.

Although the stock is trading at a relatively low P/S of 5.7x, it is not profitable and intends to invest aggressively to attract more users by building more products such as a crypto platform. While there could be significant growth upside from new products, Robinhood depends on favourable investor recognition to gain additional users and positive investing sentiment to drive revenues.

With neither present at the current point in time, it may explain why Robinhood rounds up our post as the stock that has fallen the most since its IPO.

Should you buy the dip?

Months of market weakness has led to many popular US tech stocks dipping way below its IPO prices. For some companies such as SentinelOne and Monday.com, valuations are still lofty and it may not yet be the right time to enter while stocks such as Coinbase are trading at palatable valuations and could be logical to enter.

Companies such as DoorDash have grown out of their IPO shell with multiple acquisitions and strong growth outlook while others such as UiPath has seen strong support from Cathie Wood’s ARK funds and may seem like reasonable buys.

Finally, stocks like StoneCo and Robinhood faces numerous headwinds that are not only macro in nature but also specific to the company.

As such, not all stocks that has fallen past its IPO price may be a good investment at this point in time and investors may have to dive deeper into the fundamentals and the future prospects before making an assessment.