Following my partial sales of IFAST and Food Empire last month, both have dropped out of core holdings. However, still included them in this final quarterly report. I will probably do it differently next year since there is a slight variation in my investing approach.

A

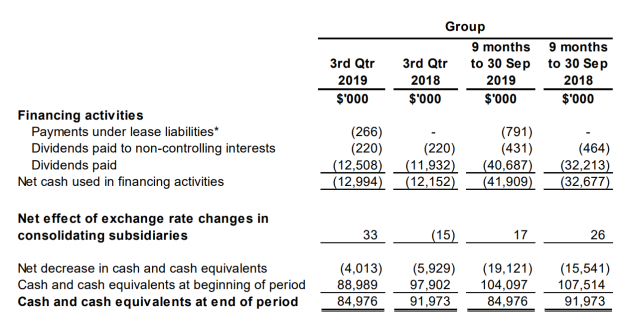

VICOM [CPF@$6.14]

VICOM continues its steady performance for the year. Revenue up 4.7% and net profit up 6.3%. Pretty similar on a 9-month basis with top and bottom lines up by 4.2% and 5.2% respectively.

Level of cash has dropped to $85 mil as compared to $92 mil for the same quarter last year. That can be attributed to the additional of $8 mil of dividend given out. While the net decrease in cash is higher this year, the difference is only about half the additional dividend.

Assuming similar performance for the final quarter, the group might be able to have cash near to $100 mil again. Which means that it is likely to give out similar amount of dividend for the full year.

Divested partially last month to reduce its position size. Unless the price correct by at least 10%, I am unlikely to add in the next few months.

Valuetronics [6.2%@$0.60]

An “A” grade for Valuetronics for being resilient despite the challenging environment it is operating in. While revenue dipped slightly compared to previous year, it is significant higher compared to Q1, reversing the trend of falling revenue from the past 2 quarters.Also its net profit margin is at a healthy 7.9%, despite a relatively higher contribution from CE segment this quarter as compared to previous quarter.

Cash per share now stands at 42 cents even as it expand its manufacturing footprint into Vietnam. The icing on the cake is the increase of its interim dividend from 5 HK cents to 6 HK cents. Looking at the mid-year report, it is likely to maintain a 20 HK cents for the final dividend, providing a 6.1% yield for its current price of 74 cents.

While I continue to think that it deserves a better valuation, I am not going to add more as it is occupying about 7.2% of my portfolio. So will just continue to hold on to my current stake to collect the dividend.

B

Raffles Medical Group [5.3%@$1.26]

Revenue continues to grow and net income continues to drop due to gestation loss of RafflesChongQing. The exact sentiment I had when I wrote in the last quarterly report. I would expect the same for the next few quarters too.

Just holding on to what I have. Will patiently wait for it to succeed in its expansion plan.

Straco [4.7%@$0.81]

Straco continues to report a lower revenue for the year due to lower visitor numbers at SOA. 9 months net profit and EPS is higher due to the closure of SF in 2018. One positive number from the report is the 20% increase in the ridership for its Lixing Cable Car. While it is not the best results, its net cash per share is at a high of 20.9 cents. So it is likely to maintain is 3.5 cents final dividend, which translates to a 4.7% yield at current price of 74 cents.

No change in my thinking of the company. So will continue to hold on to my current stake.

Food Empire [3.9%@$0.67]

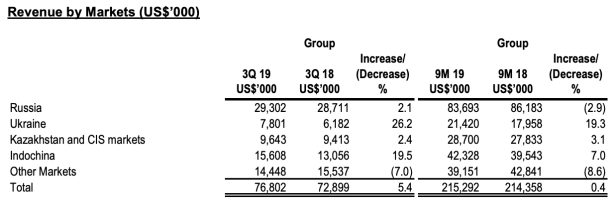

As expected its net profit continues to grow this quarter (up 34.4%) as the group continues to rationalise their underperforming businesses.

It is encouraging to see double digit revenue growth in Indochina again. The group has also guided that the second coffee plant in India is expected to commence in early part of 2020. Hoping for more dividend for this financial year and continued growth next year.

Divested some last month to raise cash for US growth counters. I am quietly confident that it will continue to do well in the next few years.

iFAST [1.9%@$0.92]

IFAST produced a better than expected Q3 results. Despite the volatility market, its AUA grew 17.3% year-to-date, to a record high of S$9.44 billion. Both revenue and net revenue grew for the quarter but net income decreased by about 6% due to additional expenditure in platform capabilities.

Possible catalysts in the coming months include being awarded the digital bank license, continued growth in HK market due to the the launch of the US stock trading capabilities since last year, and continued growth in the Malaysia market.

It will take some time for its China market to turn profitable. However, if they are successful, then the potential is enormous.

Looks like my concern for its HK market is uncalled for? Probably will wait for lower price to add more.