The details of Keppel’s O&M arm and Sembcorp Marine‘s merger has finally been announced, providing certainty to shareholders who are unnerved by the long waiting time. The merger was communicated previously and been in the works for a while now, this morning, Keppel had finally signed the definitive agreement for the merger.

Strategic rationale

The proposed merger between Keppel Offshore & Marine (KOM) and Sembcorp Marine (SMM) expects to create a premier global player in offshore renewables, new energy and cleaner O&M solutions. There is expected to be greater synergy from the combined operational capabilities and track record from the integration of two very established industry players.

The strategic rationales are further elaborated in the following two snapshots below.

Timeline for merger

The completion is estimated to be in 4Q 2022. we think it may be effective from 1 January 2023 as the combined company start a relationship in a fresh financial year.

What Keppel shareholders need to know?

Keppel Corporation (KCL) will sell KOM to SMM.

As previously communicated, KCL will retain certain out of scope assets such as stakes in Floatel & Dyna-Mac. KCL will also retain KOM’s legacy rigs and associated receivables.

For the sale, KCL will receive S$0.5b cash and new shares in SMM representing a 56% stake in the combined entity .

KCL will carry out a distribution in specie to KCL shareholders amounting to 46% of shares in the combined entity and retain a 10% stake.

This 10% stake will be put into a segregated account for certain identified contingent liabilities for a period of up to 48 months from the completion of the merger. SMM has also done a similar exercise identifying contingent liabilities. if there is a claim made to SMM within 24 months of the merger, SMM will reimburse KCL in cash for these claims.

As previously communicated, KCL will place the retained legacy rigs and associated receivables into an Asset Co and continue monetising over the next 3-5 years, with external investors providing capital. Therefore, KCL will no longer fund this Asset Co and can focus its capital on its other business units.

Assuming the merger was completed in FY21, KCL estimates a pro-forma earnings per share increase from 56.2 cents to 72.5 cents, this is mainly by excluding KOM which was loss making to the tune of S$161 million.

The additional divestment gain of 208.8 cents (being 281.3 cents minus 72.5 cents) comes from the accounting gain from selling KOM and receiving SMM shares which have a market value based on its share price.

KCL shareholders are to note that this divestment gain is accounting in nature as the 56% stake is worth S$4.87 billion. The effective benefit is for shareholders to receive shares amounting to 46% of the combined entity as part of KCL’s distribution in specie.

What Sembmarine shareholders need to know?

SMM shareholders will have a 44% stake in the combined entity with KCL holding 56%(before a 46% distribution to shareholders). As Temasek is an existing shareholder in KCL and SMM, Temasek’s stake of the combined entity will be 33.5%.

The Combined Entity will issue approximately 39.9bn new shares to KCL and the issue Price for SMM based on the 10-Trading Day VWAP as of 26 April 2022 is S$0.122, implying an aggregate consideration of approximately S$4.87 billion for Keppel O&M.

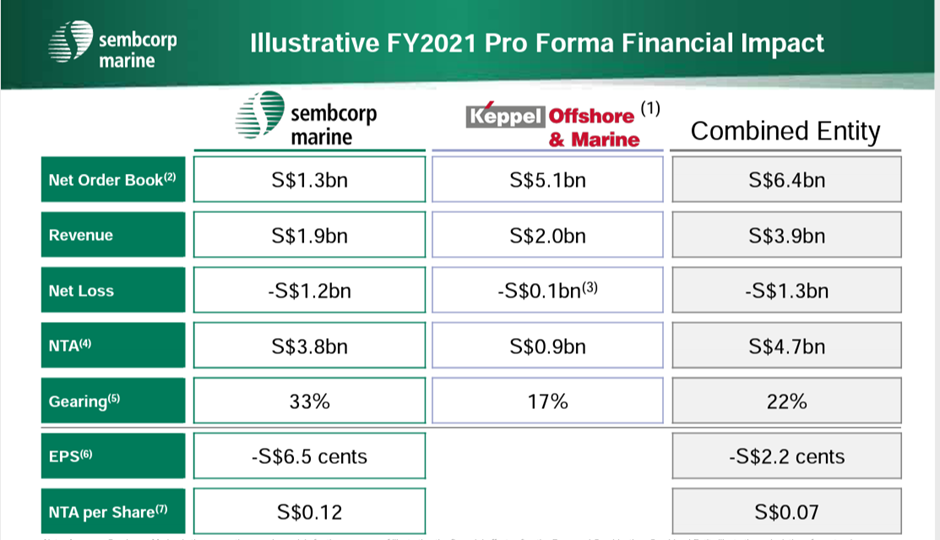

SMM provided a pro forma financial impact based on FY21 performance of each individual entity. The combined entity will obviously have a larger order book and higher revenue. However, it will have a lower net asset per share and a lower loss per share.

With a lower gearing ratio allowing for future borrowings and greater synergy from the combined operational capabilities hopefully reducing losses and potentially even turning a profit, SMM shareholders can hope that a cash call by way of a rights issue (if required) would not come so soon.

Closing statement

The merger was required for competitive reasons as both KOM & SMM have been loss making for many years and have seen their orderbook shrunk. Similar to when Sembcorp Industries had divested SMM previously, KCL shareholders will see the company’s share of Offshore & Marine assets reduce as the company focuses on its Vision 2030 plans.

SMM shareholders will roll their shares into a larger entity who would hopefully be able to see the combined entity deliver on their strategic and growth plans, turn into profitability and build value for shareholders.

With that, the only unknown now is – what will the name of the combined entity be?